I know, and I am even a subscriber.

And I occasionally use it for The Market articles, too.

I feel us openly discussing this loophole here will lead to it being closed soon(er). ![]()

I know, and I am even a subscriber.

And I occasionally use it for The Market articles, too.

I feel us openly discussing this loophole here will lead to it being closed soon(er). ![]()

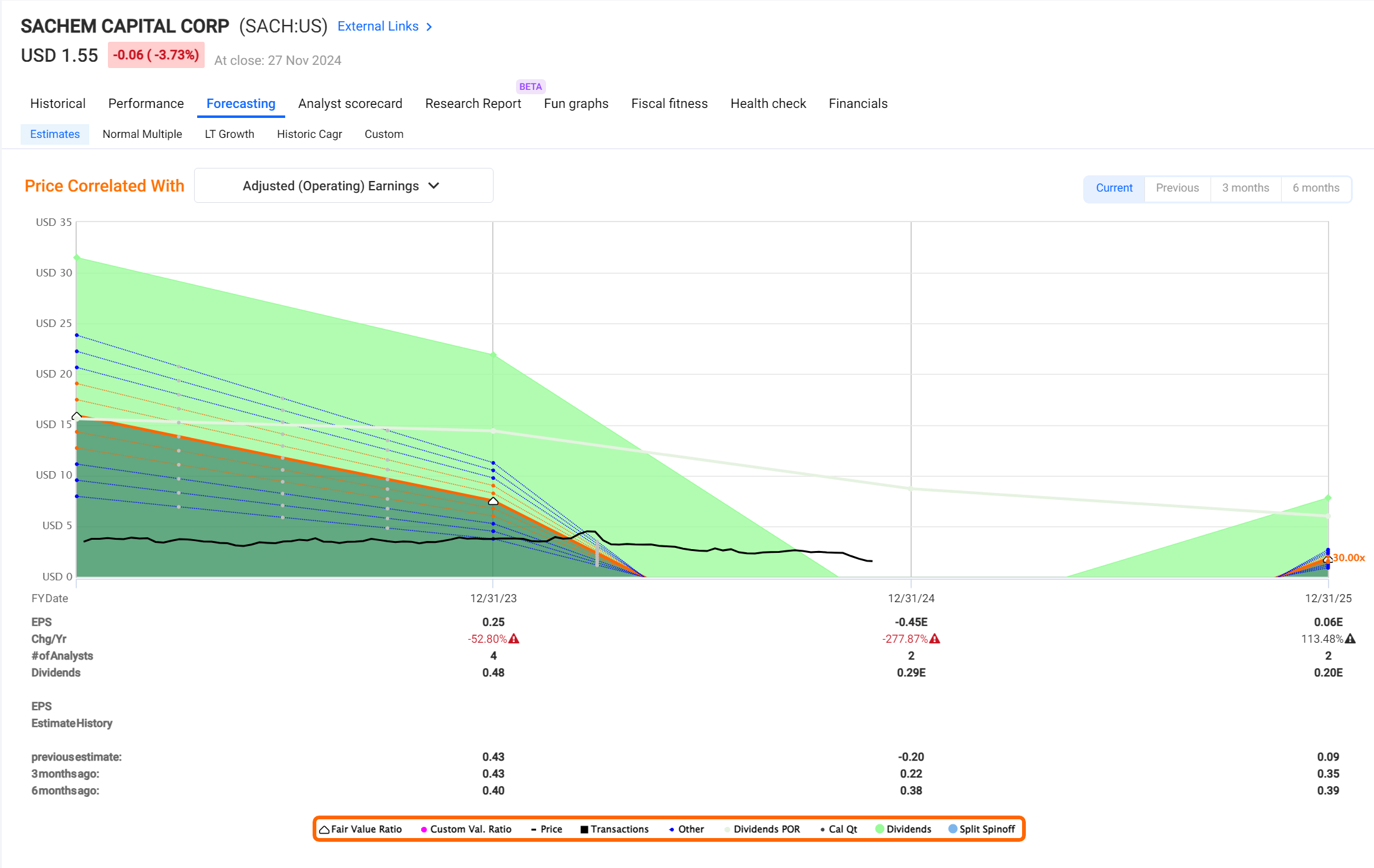

I just found this company Sachem Corp. that is -62% this year, they have been missing the revenues but it doesn’'t look like a bad company… maybe undervaluated right now. What do you think?

TL;DR: I would pass.

Tiny (USD 72M market cap) mortgage REIT, yielding close to 13%, about 50% debt.

Historical graph:

Forcasting estimates:

Even though I like dividends, this one wouldn’t be for me.

They expect negative earnings this year and the two analysts covering the company expect tiny earnings next year that they’ve been lowering from 39 cents six months ago to 35 cents three months ago to 9 cents in the previous estimate to 6 cents now.

With no earnings the company will likely have to cut their dividend.

According to their latest 10-Q they’re a bit concentrated in risk exposure, both geographically (over half in New England) as well as in the distribution of borrowers (e.g. the company has one borrower of $54M representing 11.3% of the outstanding mortgage loan portfolio – if that borrower has an issue, the stock price will likely take a massive hit).

Their debt and maturity schedule won’t leave a lot of flexibility with cash flows, as they’ll have to pay down about $34M till the end of 2024 (with negative earnings …) and $56M next year (with tiny earnings expected). And a bunch more debt is maturing in 2026 and 2027.

Given the still relatively high interest rate environment, I don’t think they’ll be able to re-finance the soon maturing debt at lower rates.

At September 30, 2024, the Company had an aggregate of $260.5 million of unsecured, unsubordinated notes payable outstanding, net of $4.3 million of deferred financing costs (collectively, the “Notes”). During the nine months ended September 30, 2024, the company redeemed its 7.125% unsecured, unsubordinated Notes due June 30, 2024 in the aggregate principal amount of $23.7 million plus the accrued interest thereon. At September 30, 2024, the Company had six series of Notes outstanding:

(i) Notes having an aggregate principal amount of $34.5 million bearing interest at 6.875% per annum and maturing December 30, 2024 (the “December 2024 Notes”);

(ii) Notes having an aggregate principal amount of $56.4 million bearing interest at 7.75% per annum and maturing September 30, 2025 (the “September 2025 Notes”);

(iii) Notes having an aggregate principal amount of $51.8 million bearing interest at 6.0% per annum and maturing December 30, 2026 (the “December 2026 Notes”);

(iv) Notes having an aggregate principal amount of $51.9 million bearing interest at 6.0% per annum and maturing March 30, 2027 (the “March 2027 Notes”);

(v) Notes having an aggregate principal amount of $30.0 million bearing interest at 7.125% per annum and maturing June 30, 2027 (the “June 2027 Notes”); and

(vi) Notes having an aggregate principal amount of $40.3 million bearing interest at 8.00% per annum and maturing September 30, 2027 (the “September 2027 Notes”).

Things I also came across in the 10-Q (highlighting mine):

In December 2021, the Company hired the daughter of the Company’s chief executive officer to perform certain credit and compliance services. For the three-month periods ended September 30, 2024 and 2023, she received compensation of $0.04 million for each period. For the nine-month periods ended September 30, 2024 and 2023, she received compensation of $0.1 million for each period.

IMO, if you’re a public company, just don’t hire the CEOs daughter to do stuff for the company …

Looking at their latest investor presentation from November 14, it doesn’t look like a bad company, just one that I personally wouldn’t pick over other options out there – as one of my mentors likes to say: there’s many other potential brides out there and you don’t have drink yourself into finding this one to be the most beautiful one. ![]()

Just saw this post and was wondering why you did not go for GLDM instead of GLD? It’s basically the same but a fraction of GLD and with lower TER if I understand correctly.

I guess it is the power of marketing. I heard of GLD and didn’t think about GLDM - I assumed it was just for people who wanted to buy smaller amounts.

I wonder if there is a trade off though:

For the remaining shareholders of Idorsia – they continue to make headlines: Idorsia: Der Überlebenskampf der Biotechfirma spitzt sich zu (paywalled in German)

English summary:*

The Swiss biotech company Idorsia is facing severe financial difficulties and urgently needs new funds to avoid insolvency. Key points include:

Declining Stock Value: Idorsia’s market capitalization has dropped sharply, with its stock now valued at less than one Swiss franc, compared to nearly 30 francs five years ago.

Missed Licensing Deal: The company had hoped to finalize a licensing deal for its hypertension drug, Aprocitentan, by the end of 2024. While negotiations continue, there is no guarantee of a deal, leaving the company’s financial future uncertain.

Liquidity Issues: Despite a recent $35 million exclusivity payment, Idorsia’s cash reserves are estimated to be around CHF 70 million at year-end, far short of the CHF 200 million convertible bond repayment due in January 2025.

Strategic Options Open: The management is exploring all strategic options, including a potential sale of the company, a move previously resisted by major shareholder Jean-Paul Clozel. The Clozels, who control a significant stake, might also consider taking the company private.

Management Criticism: Analysts criticize Idorsia’s leadership for poor cost management and inaction, which they claim have jeopardized the company’s value and future.

The company’s immediate priority is securing funds or reaching an agreement with bondholders to delay repayment. Without these measures, Idorsia’s survival is at serious risk.

* Courtesy of VCs, MicroSoft and other investors setting their money on fire by investing in OpenAI.

Comes to show how hard it is to invest in pharma, I probably wouldn’t do it even if I was allowed to.

https://www.fiercebiotech.com/biotech/fierce-biotechs-rotten-tomatoes-2024

Pity for Idorsia, has some good people…

Great day today: my Walgreens Boots Alliance (WBA) position is up 25% after they announced they increased their losses in Q4.

(Nope, not gonna look at my other positions today … ![]() )

)

What happened? I didn’t even buy anything today!

What’s going on with WBA? Is it at risk of bankruptcy?

WSJ says that hope for rate cuts have further dimmed as the jobs report today came out way better than expected.

I like Chat-GPT’s explanation better, though:

The markets are down today because it seems like every investor collectively woke up on the wrong side of their portfolio. Fear clouds have gathered over Wall Street, casting shadows of uncertainty so thick that even the bulls are lost in a maze of pessimism. Central banks’ policies have rattled the financial tectonic plates, causing tremors that shook the courage right out of the market’s heart. Somewhere, a butterfly flapped its wings in a far-off economy, causing a hurricane of doubt to blow through trading floors. In short, it’s a perfect storm of sentiment where every little worry has grown into a financial monster, and the sky is raining red arrows. Tomorrow? Hopefully, the sun of optimism rises again!

During and post-COVID they made massive losses on their convenience store part of their business as people literally looted the places … they then cut their dividend after a couple of decades of raising it and no plan was in sight to turn things around.

A new CEO arrived recently and decided to cut off the dying limbs which led to more losses but now an end seems in sight and investors hope the pharmacy part of their business will do fine, hence the jump in price.

Or something like that. ![]()

And there I was reading Good to Great (2001) admiring what a fantastic company it is/was. ![]()

I guess I need to read fresher books.

How will the pharmacy business do well if they had to close a ton of their stores and can’t open them again due to looting?

I believe they’ve (mostly) given up on their non-pharmacy business (situated mostly in cities, like San Francisco, where stores got looted).

Their mostly pharmacy only business (situated in strip malls outside cities) aren’t looted because … ahem, you need a car [to get there] in the land of milk and honey* which is less suitable for casual looting if you … don’t have a car …?

Anywho, who am I to judge whether this is a good business – they don’t plan to re-open those vulnerable stores (and have sold them or are selling them), and the market seems to think this is a viable plan.

As we’ve been told by Nobel laureates: the market is always right.

No?

![]()

* As I looked up the lyrics and the video for this line, I realized for the first time in probably about 35 years that I have apparently misheard their line – you’ve got to have a con in this land of milk and honey – mistakenly as you’ve got to have a car in this land of milk and honey.

The latter makes sense to me, the former still doesn’t.

For reference: The Message by Grandmaster Flash and the Furious Five, for those graybeards who were around at the time, listening to one of the first Hip Hop tracks at the time.

Lyrics: Grandmaster Flash and the Furious Five The Message - Google Search

Video: https://youtu.be/PobrSpMwKk4?si=AGEvuiI3YZh4M4SB&t=182

I understand it as the only way up in society (or to keep sitting in a good position) is to deceit and profit from others, which fits the theme of the song that things are terrible in their neighborhood and they can’t afford to move.

You’re right – I guess I’m more upset about my decades of having misheard/misunderstood that line.

I suppose, at least back then, both car and con would have worked, and at least today, I would say that the car line might be even more true … and I’m not really sure what I want to say about the con line/interpretation …

I thought they had a petrol station kind of model: you go there because you need to buy paracetamol and end up buying a lot of other over-priced stuff. Plus it is also combined with a convenience store, so you go buy your milk and while you’re there get a bulk pack of anti-depressants. ![]()

on my “top top” playlist.

You’ll admire all the number-book takers

Thugs, pimps and pushers and the big money-makers

Drivin’ big cars, spendin’ twenties and tens

And you’ll wanna grow up to be just like them, huh

could be a Leitmotiv for some of us here…