They don‘t have to. Apple Pay is not a different payment provider. It just provides authentication and tokenization (obfuscation) for your card details.

That is, an AMEX card added to Apple Pay still is and appears as an AMEX. Thus it will only be accepted by merchants that accept AMEX - which Revolut does not,

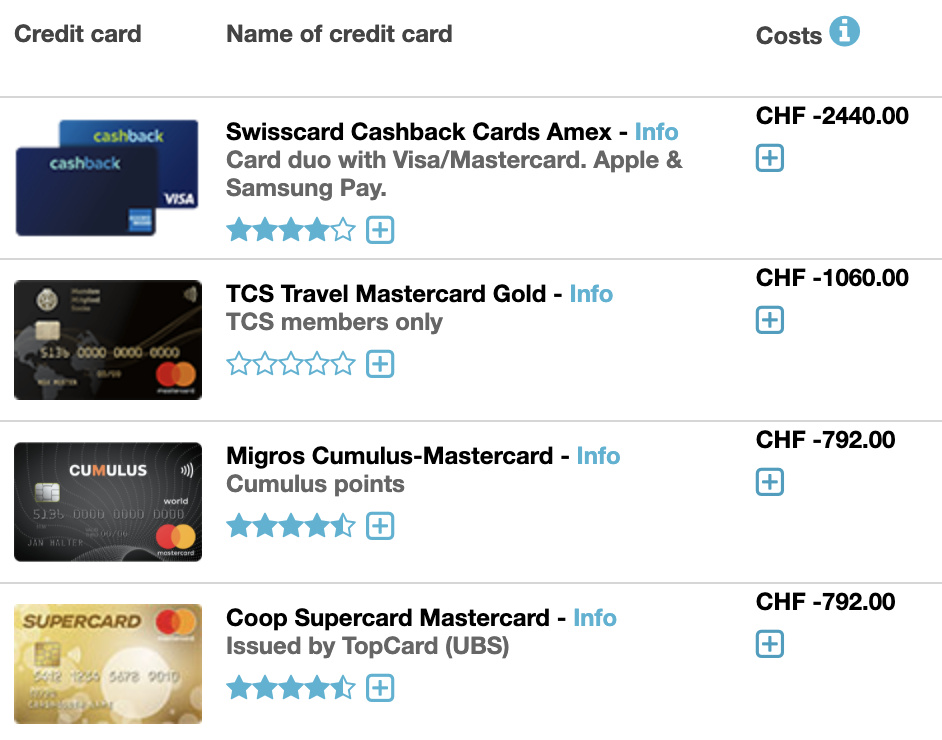

Hey guys, I have been looking into credit cards. The Swisscard Amex clearly comes on the top, thanks to the 1% cashback. Could you tell me:

How is it with acceptance of the Amex card in Swiss shops: Coop, Migros, restaurants, clothes, online? How often are you not able to pay? It’s nice that they offer a card duo, but it would be inconvenient to have to carry both cards at all times.

How does the cashback work? Is it as simple as money being credited to your account? I own the Cumulus card and have to collect these silly points, which I then can only spend in Migros.

Here is a 10 year calculation for payments of 2000 CHF per month:

If the Amex card would work, it could mean saving 240 CHF per year. This I could only achieve with the Cumulus/Supercard if I always shopped in Migros/Coop, which I don’t do, and don’t like to be limited.

Alternatively, does any of you have experience with other cards: gold, platinum? They offer some benefits which are hard to measure, like access to airport lounges, concierge service (whatever that means). The particularly interesting card is the Diners Club one. It offers:

There is a post somewhere about that. I know you can’t use it at Aldi, Lidl and Digitec.

The Amex duo pays back at the end of the year only. If you have the other offer from cashback, it will pay at the end of the month.

Amex pays 5% the first 3 months , then 1%. The second card in the duo pays 0.2%, less than cumulus CC if you buy at migros all the time. The second offer from Cashback pays 0.25%. You might use the Amex from the first offer and the Visa from the other. Have a look at their site and filter for “cashback”

I lost a flight (kind-of cancelled) for Covid and I booked with the Cumulus CC, the only card that offers (offered?) an insurance. The insurance they offer is useless if you have a Health insurance though. They offer for free only things that an Health Insurance can offer iirc.

Acceptance is pretty good, Coop & Migros isn’t a problem. Some restaurants and a few smaller shops don’t. For me, it doesn’t happen that often. Some online shops also don’t accept it.

I am having both in my iPhone’s wallet and am using them with Apple Pay. As a physical card for “backup” purposes, I would rather carry a VISA (due to the better acceptance) than an AMEX anyway.

Indeed it is.

I’ve had both but decided to cancel the standalone cashback card. Even though I liked the kind of “unbranded” design. But keeping a second card and credit account around to monitor, just for the occasional 0.05% wasn’t worth it to me.

And I may I ask, did anyone have experience with the Diners Club card? On paper, it could look quite interesting. The card costs 150 CHF per year. What it offer is 1 award mile per 1 CHF spent, 5 free airport lounge entries per year and a range of insurances:

Cancellation expenses, travel interruption and travel assistance CHF 40,000

Travel delay CHF 3,000

Baggage CHF 10,000

Treatment expenses and medical assistance CHF 1,500,000

Deductible coverage for car rentals (CDW): CHF 10,000

So how much are the miles worth? You can redeem them by for example taking a ZRH-LAX round trip for 30’000 miles (+350 CHF taxes). A flight like this usually costs around 750 CHF, so this would put 30’000 miles at the value of 400 CHF (0.013 CHF/mile)

If you opt for business class, you can have it for 112’000 miles (+650 CHF taxes). But the regular ticket costs a whopping 4300 CHF (0.032 CHF/mile)

So if you used the Diners Club as your primary card and spend 30’000 per year, you could get an intercontinental return business class flightonce every three years (the additional cost would be 3x150 CHF for the card fee + 650 for air taxes). In the same time period, the Swisscard AMEX would bring you only 1000 CHF cashback.

Is anybody using this card so that he could verify if what I say makes sense?

I started with the Visa alone and decided to keep it since both cards (actually card + card duo) uses the same system, so it’s a matter of one click to see what is happening with the other.

Do the covid test. Is this insurance paying for an interruption like the ones we saw this year? What happens if the government doesn’t let you fly but the flight is still occurring? I believe this insurance is probably reinboursing only health related issues with flights (like if you fall ill).

“taxes”. Some government should make compulsory that everything you call “tax” must go straight to the government.

I have both too: Amex + Cumulus. The other Cashback card is in a drawer somewhere. Really worth it. Also, if you pay with your Amex at Migros, then you’re effectively getting 2% cashback.

I concur with the other posts. Acceptance is quite good. Exceptions: some restaurants and bakeries, Digitec, Aldi. Doesn’t hurt to try and if you get an “unknown card” then just have a go with your Cumulus.

But you can pay Sunrise bills with your Amex. You can also pay your Mobility bills with it. Spotify works ok without commission.

I use it to buy online as well in Swiss shops that accept it, just beware of store that are actually located abroad as this will make you incur in that extra fee.

LOL, you just let me fix the misconception I had in my head the whole time. I somehow thought that I only get the Cumulus points if I PAY with the Cumulus card, but it’s only about scanning the bar code, right? I feel so silly right now

So you go to Migros, buy for 100 CHF, scan your Cumulus barcode, pay with Amex, and so you have gotten 1 CHF cashback from Cumulus and 1 CHF from Amex?

Exactly! Actually of you pay with your Cumulus MasterCard at Migros they’re not giving you more than what you would get by just scanning the barcode. The same goes for Coop and their SuperCard.

I have that diners card, which I am probably going to cancel at the end of he subscription year.

The Swiss/Lufthansa miles are only worth it for business or last minute economy flights, it‘s called Miles & Less for a reason. Their theoretical value of he diner‘s card is 1%, but in economy flights it‘s much less, in business it is more.

For regular European economy trips you need at least 17000 miles(regular is 35000 but they sometimes have discounts) plus around 70 CHF for a return flight. Those flights normally cost 100-200 chf if you book a bit in advance outside of the busy season. And in the busy season you usually cannot book a trip with miles. So the value is less than a 0.5% cashback card.

For economy trips outside of Europe the value can even be negative with the international surcharges renamed as taxes. I was testing prices for an economy return trip to New York you pay around 450 chf for surcharges, plus the miles. The same trip was less than 400 chf with normal booking.

If you really value business class the program might be worth it. I think the optimal usage is to still buy an economy trip and update with miles. Then with miles you save hundreds if not thousands. Personally I don‘t care about business, but I believe you can book those flights with around 1000 in taxes and miles cashback value combined, normal bookings are a few thousands.

But in case you value business flight I think the optimal usage is to switch every year from cornercard/diners to Swisscard and get the bonus miles. In theory they might take back the Miles if you cancel in the first year, but I‘ve read they don‘t do it, especially if you actually use the card for 10000+ per year, which you will do anyway if you care about miles.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.