I woud advice another feature that is really important for some people: joint account.

I would be very interested to try the investment solution from Alpian and to use it as my (our; with my girlfriend/partner) main Bank account but only if a joint account could exist.

And I think that a lot of people are waiting for that since more woman are getting interested in personal finance and more married people tend to share their incomes together to build their future.

Also flexible to switch banks - but not as main bank relationship, yet, I will stick to a bank with state guarantee.

But as replacement for neon for example… Yeah, I can imagine that. But as of today, neon is lightyears away, there are many things to do for Alpian to get on the same level.

Definitely wish them all the best and very cool, that they have a representant (@Dino_Alpian ) here in this forum, this gives a good feeling and it is a good sign!

Alpian markets itself as a online private bank for affluent clients (between 100’000 to 1 mil CHF) with advisory or discretionnary mandates. The business model debate is irrelevant here.

A multi-currency account and payment service is an additional service, but not the core model of a private bank.

Valid point, comparing Alpian with neon as overall comparison makes probably not sense.

When comparing Alpian with Volt by Vontobel (which also does not seem to work out, same as Marcus by Goldman Sachs) from the investment perspective, the costs seem to be lower, indeed. But since this mass affluent business model seems not working out (Alpian recently had a disount program, where they give you CHF 250.- if you are transferring a higher amount of assets to them an other banks discontinued their mass affluent program), they have to offer further services, for example daily banking or payments with low FX fees - if they want to keep existing.

But when basics of the daily banking are not availabe (e.g. standing order, TWINT through pre-paid (wtf), no credit card, fees for transferring CHF to another CHF account, which is not located in CH) or regarding FX there are high ATM withdrawal fees (neon has a capped fee of 1.5% and allows free withdrawals in CH), then the whole concept will not work out.

There are too many topics at the same time under construction - they offer a lot of things, but not even one topic is covered and set-up properly, in my personal opinion. BUT, Alpian launched only two years ago, so I can understand, that some revenue has to be generated and they had to offer the services despite the full function may not be available, yet.

I am very curious, how their business model works out, maybe and I hope they are doing things a bit different than Vontobel or other banks. But I have also very high expectations in general and if someone is offering unfinished (basic) services, then I am not willing to take into account their services.

Business model seems a bit like Neon’s - just upside down. Where Neon started with a free, no-frills current account and card and then progressed into offering/selling additional or supplementary services later, Alpian sounds like taking a reverse approach. I kind of get that/why they don’t want to prioritise on the current account features when they want to generate revenue.

But when you go to their website, the first and most prominent claim you come across is this:

# Premium banking, now at your reach Manage your daily finances and invest for the future, all from a single app

Premium banking, managing daily finances - and failing to offer (according to what I’m told here) standing orders? That doesn’t compute.

Valid point. And if you’re marketing to affluent individuals, you don’t necessarily have to compete with the most low-cost options on the market (such as ATM cash withdrawals).

But maybe they shouldn’t advertise “daily finances” so prominently then - when they lack essential payment functionality to get one’s “daily finances” done?

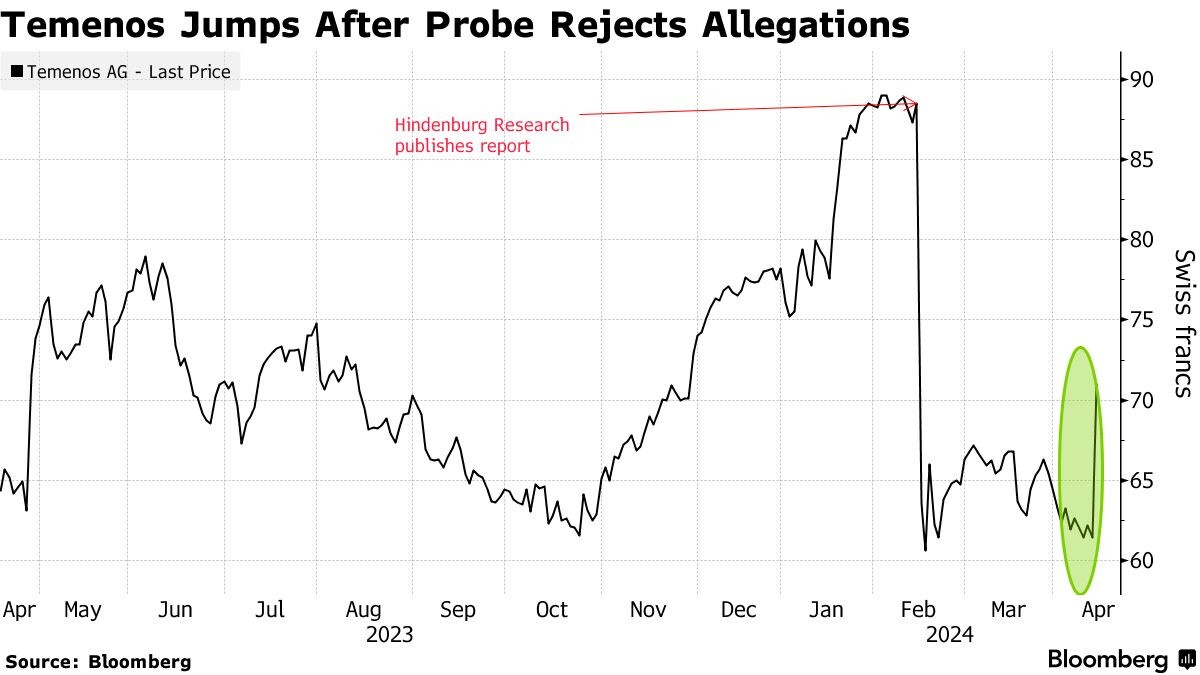

They haven’t reinvented the wheel AFAIK, they are using Temenos Banking Cloud [1]. And that product surely has standing orders as a feature. But then again Temenos seems to have some problems on it’s own [2].

Or maybe they also switched? The article says that they host on Azure, but their website is hosted on AWS (Amazon Web Services) and their API+Monitoring on Google Cloud.

Then they shouldn’t promote their bank as “Manage your daily finances and invest for the future, all from a single app.” as @San_Francisco correctly pointed out. And even if you are a private bank, your “additional service” should be up to par with all others. Otherwise yes, focus on your main business, being a wealth manager - that’s where the money is anyways.

Alpian seems to advertise as well as on bargain websites as Preispirat:

(Unfortunately in German, but you can translate the website - the comments are pretty critical).

Couple of days ago - out of curiosity - I started the application process at alpian but it somehow got stuck during the online identification, therefore, I never got the chance to sign any documents. Nevertheless, today came the card, lol.

Honestly, meanwhile I do not know what to think about the whole situation:

neon/Revolut/Zak/… are already further and provide a solid service - if you are looking for an FX payment servicer.

I invest in tax and cost efficient ETFs like VTI. I thought about having a fun portfolio with alpian, but somehow this would not be wise, because the opportunity costs are too damn high and I am pretty confident to beat their actively managed portfolio.

Moreover, the clients for digital (private) banking should be IT affin - with high probability, they manage their finances by themselves.

Too much advertising on „wrong“ channels, where the „wrong“ target clients are. Gives me a strange feeling as potential customer.

Only real USP: paying out interest monthly. WillBe has it quarterly, so pretty good, as well with 30% higher interest rates (as of today).

Nor sure about their wealth management; Goldman Sachs takes a minimum of CHF 10m, other private banks start with CHF 5m or even CHF 1m. How many possibilies are there with an investment of CHF 30k? Who gives me the guarantee, that they are not just throwing the assets in an automated robo-advisor? In that case, I could continue with True Wealth or - soon - finpension.

When checking the fianncial statement 2022, the cash burn rate is enormous and nearly swallowed seed round B. Competitors like Clear Minds Investment AG (liquidated) or UBS WM commented once, that the Swiss market is too small for mass affluent clients (Note: UBS has an digital plattform for wealthy clients in the US, but not in CH).

I always liked when new competitors disrupted the market - but in this case I have no clue how this will continue, or end. There are too many questions for an initial 30min online meeting with once of their advisors, so I will probably just close it or keep it running, since I did not sign docs.

What are you experiences so far? The ones who invested: how confident are you with the gains so far, when compared to your own portfolio, which consists e.g. of VT?

I think you are looking at it from a different perspective versus what this platform is designed for.

You are of firm believer in index investing using VT. Based on historical data , we know that passive investing works very well at least for large and mid cap stocks. So for you VT works fine.

But there are many people who fall into following categories

They want index investing but not sure about asset allocation (stocks, fixed income, gold, crypto, commodities, real estate etc)

They want index investing but don’t feel confident about going for global market cap driven ETF and want different regional allocation. However they don’t know how to decide.

They simply don’t believe in index investing

I believe Alpian is trying to serve the needs of people in three segments mentioned above. And if you think about it, the fees is lower versus traditional wealth management options.

You might think people should simply research themselves and decide regional allocation and asset allocation strategies. But it is not a skill that everyone possess.

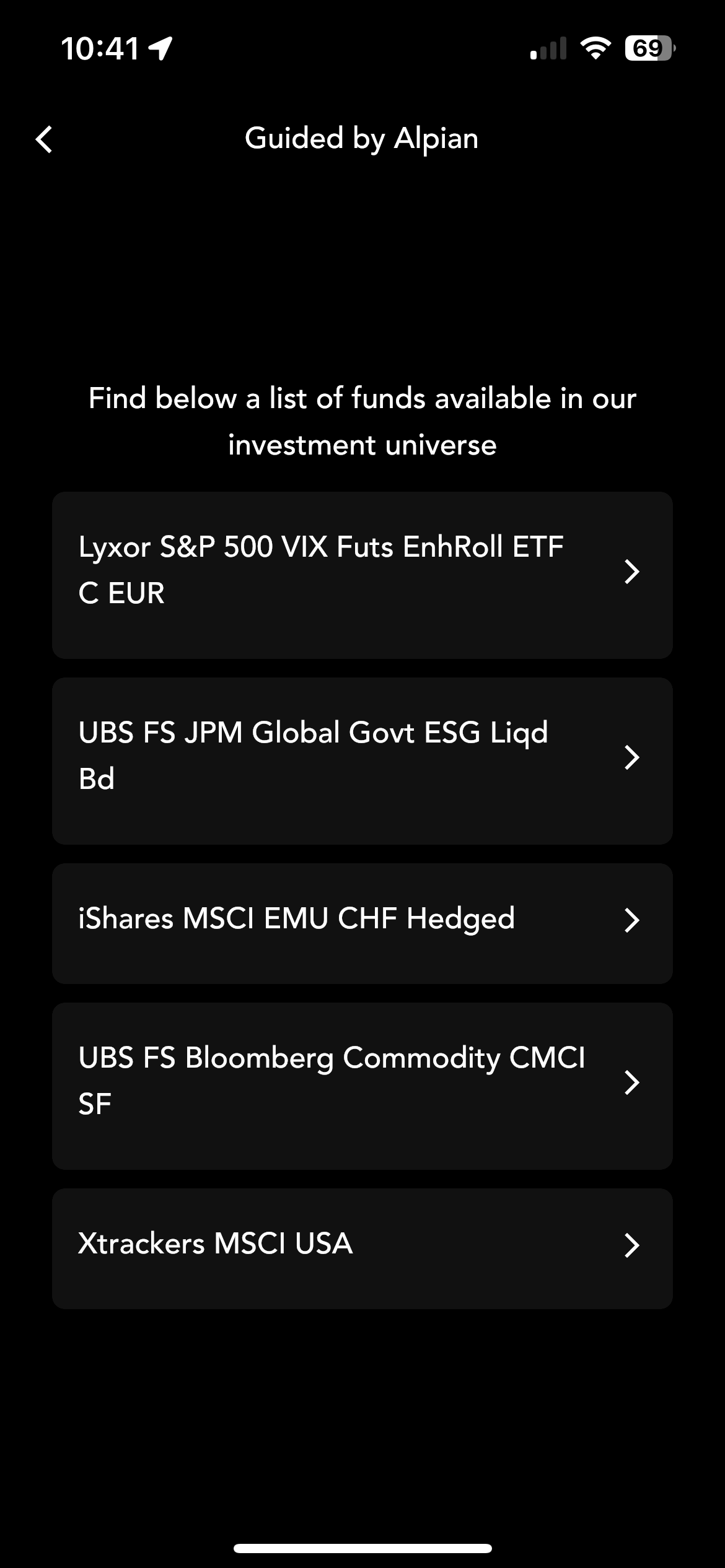

The only interesting one is the Xtrackers MSCI USA in this list. Not sure, if this is based on my questionaire (very aggressive), or all available assets.

Anyways, would be interesting to see how the products look like when choosing „Managed by Alpian“.

Makes UBS‘s Platinum cards (CHF 38/month including banking package) look cheap in comparison.

Bonus: And UBS’s are real credit cards (and a VISA/Mastercard two-card set, if I’m not mistaken).

Someone is optimistic: Alpian has raised 76mio CHF as a result of their Series-C funding round. Alpian AUM is nearing 100 mio CHF, quite some valuation that!

According to my calculations applying such a valuation to UBS (with 5 trillion AUM), I receive a valuation of 4 trillion. Ok folks, off to pitch my investment case to SoftBank

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.