Either they’re confident about their solution, or they’re trying to attract people because the solution isn’t profitable…

Will the curious take the plunge and test the solution?

Interesting to see that they waived their fees - based on the net wealth you have with them.

50k net wealth (cash and/or invested) results in a free bank account with four currencies and a physical and virtual Visa debit.

Fee structure from FX and transactions is pretty fair, tbh and compared to other banks. So, in my eyes, it is a real alternative if you want to change your bank relationship.

I personally would probably not use the Visa debit; for FX I use neon and for CHF transaction Cornercard Plat (yes, I need and want these card linked insurances).

0.75% as management fee is not good, but also not terrible. With the traditional WM banks you get in the same range, with additional businesses (e.g. mortgage, lombard etc) then 0.4-0.5% in management fees.

I would be interested in knowing more about the investments, anyone has more infos?

EDIT: just saw, that Interactive Brokers is the Depotbank. So, I can see how they make their money, with a high spread

Yes, I am still with them. And until now, I am rather pleased. I had several personal contacts with members of their team (not only online), questions I raised were answered in a detailed way. This is for me a major reason of sticking with them. Obviously, I wouldn’t put all my eggs in the same basket, but I am adding step by step (every month) money in my “Managed by Alpian” portfolio.Then, at some point, I will stop and see how it develops. I agree that it might be cheaper to manage investments by myself, as I have attempted to do it in part for two years, but I do not claim any expertise in investments and I am interested in having people taking care of it. About once a month, for customers having a “Managed by Alpian” account, a good analysis is provided about the evolution of the markets and about the choices made by Alpian.

A bit strange to cite personal growth and feeling at home in Rhode Island as the reason to leave. Leaving long before the profit zone is reached will not result in a great payout as he most likely will be asked to sell his shares. Maybe the underlying message is that not every founder is also a good CEO?

Regarding our interest rates in CHF: We are pleased to inform you that we waive all fees for the first 6 months for the account. Our interest rate is structured as follows:

1% for amounts from 0 to CHF 50’000.

For any amount above 50’000 to CHF 1 million, the interest rate is 1.5%. Do note, if you have CHF 50.1k, only the 0.1k is subject to the 1.5% rate, not the entire amount.

The interest is paid monthly on a pro rata basis. Additionally, your amount is not locked, providing flexibility in your finances.

We provide insurance coverage up to CHF 100’000.

Feel free to ask if you have any further questions!

Thank you very much for your interest, however we do not offer corporate accounts at the moment.

I invite you to subscribe to our newsletter (at the bottom of our website) on alpian.com to receive the latest news and releases concerning Alpian.

I’m about to start a alpian account. Does somebody have a referral code? I would prefer a personal one than the generic ones that are out there or the ones from the known blogs. Feel free to DM me

I participated in an account opening race. Then I never funded the account and never used the card they sent. Not sure about my account status. Probably doesn’t matter, as it has zero balance.

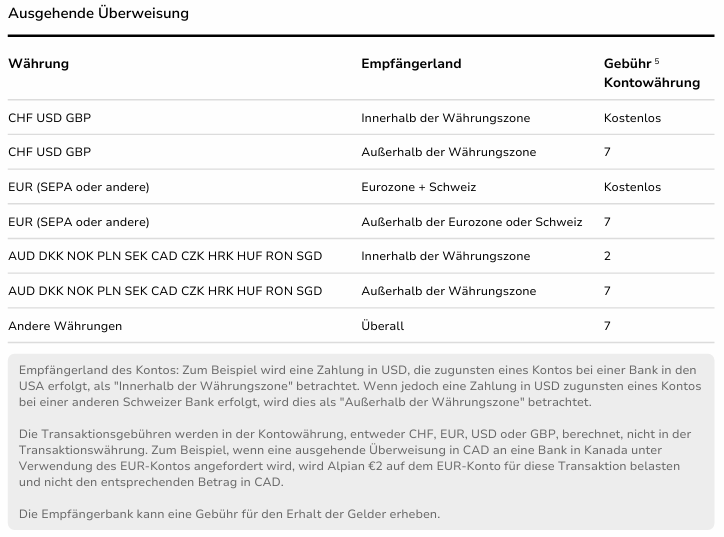

Since the UK is not part of the CHF currency union, they charge 7 CHF. But sending money from my cantonal bank to the same IBAN is completely free…

Well said. It’s basically what it is. I’m not going to pay a 0.75% management fee + ?% ETF fees + ~0.2% FX costs for a IBKR redesign. Access to financial advisors is included in the fee, but I don’t know how much that helps if you just invest in to ETFs on Alpian anyways.

We understand you are an experienced investor, so if you are looking for a brokerage solution, which we do not offer, then IBRK might be an option to consider. There is no point in convincing you to buy a solution you don’t need; we agree. This assumes, of course, that you have the time and knowledge to pick your investments, build your portfolio, and monitor it.

However, many individuals in Switzerland are looking for advice or someone to manage a portfolio on their behalf, and we believe we can be a good partner for these persons.

We offer two distinct solutions, “Managed by” and “Guided by,” at prices we believe are very competitive. Our fee of 0.75% includes:

Proprietary risk profiling

Bespoke asset allocation (unlike many banks, each portfolio is optimized; we don’t offer “standard” profiles)

Access to a curated universe of handpicked ETFs

No costly “in-house” products

Options to add constraints on certain asset classes

Monitoring and management of the portfolio by our investment team (note: we are not a robo-advisor)

Custody fees

Transaction fees, which can be significant in the case of frequent turnover

Access to advisors who are not incentivized to sell products

An intuitive interface to track decisions, performance, and exposure

This offering is much more than just an IBRK redesign; it’s more akin to the services of a private bank but at slightly more than the price of a robo-advisor. We agree on one point: for a bank that is trying to change the banking sector, we would have failed if we were merely providing a UX on top of a broker—but that’s not the case.

Many individuals have entrusted us with the management of their money, even large portfolios, and we have received positive feedback.

We appreciate your candid feedback, and if you have any suggestions on how we could improve our offerings, we’d be happy to hear them.

Yes, I’m managing all investments by myself, therefore your investment offering doesn’t suite my needs. I was only interested in the banking part. However, I agree that many people lack the time or expertise to manage their investments, and you offer a great solution for them.

You’re right, I might have been too harsh there. Since I handle everything myself, it’s sometimes hard to see things from the perspective of those who appreciate and use services like yours. And the product is probably working, otherwise you wouldn’t exist.

Whether the 0.75% fee is competitive can be debated, as it only covers the management fee, with ETF, brokerage/Courtagen, and foreign exchange fees also applying (or am I wrong?). Some cantonal banks come out cheaper, but then I guess they don’t offer any individual asset allocation.

Please implement standing orders. You are a bank and this feature shouldn’t even be debated upon. I don’t know why it doesn’t exist.

Please provide a phone number on your website. Imagine your servers going down and customers can’t contact you, because the only way to contact you is through a form on the website or in-app chat. A bank should have a public phone and email listed on their website. Or maybe I didn’t see it.

Fix this UI bug. I guess here it should say “Advices”?

Allow me to delete beneficiaries (like people I send money to). Once I add them, they will stay there forever. Mistyped something, well.. too late.

Checking out the privacy notice doesn’t work. Maybe it’s just my android phone: https://imgur.com/zi8oOk5

About the investing platform I don’t have any feedback, I never used it.

But enough with all the critique.

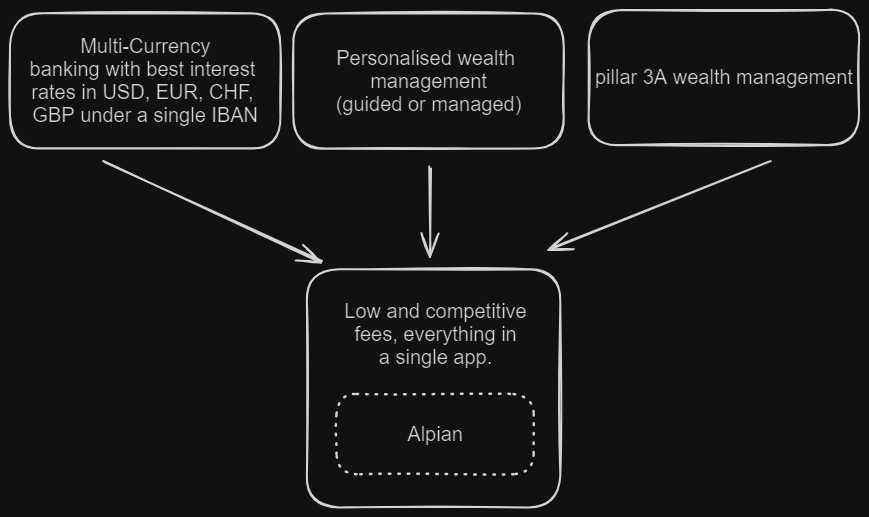

I think you are building something great and with that my idea/suggestion. In my opinion, what’s still missing in Switzerland is a “do-it-all” digital bank with competitive rates:

Great private banking: You offer four currencies under a single IBAN with highly competitive FX rates. At my cantonal bank, I would need four separate IBANs, incur over 1% in FX fees, and pay annual fees for each currency account. I even earn interest, paid monthly, on my checking account with you—something unimaginable at other banks. The things you’re still missing, I told you above. Additionally let customers put their USD, GBP, EUR balancesinto money market funds for a small fee (Something like Lightyear [1], WillBe [2] or Trading212 [3]). Zero management requirements for you and guaranteed income, since you take a small cut (e.g. 0.25%). If you have that, you will have the best interest rates and therefore the best offering in Switzerland.

Wealth management: I will take you by your word, that you have great investment offerings and your fee is competitive, so that step is also kinda complete. You also got your own advisors that can help customers for free and those don’t have to think about getting scammed. Fee is always the same.

3A wealth management: You don’t offer pillar-3a investments. I don’t know if that’s technically possible for you, because you need your own Charity/Stiftung, but you are losing out on a lot of customer funds. People care about convenience and if they can have everything in a single app, most people will not care if the fee 20bp higher or not. Additionally if your advisors can offer those things to new customers, who might not even know how the third pillar works, those customers would be delighted.

Sure, most banks offer all these things nowadays, but their fees are high and services are shuffled together and the App is… well you get it.

That’s like my dream if I were to ever build a bank, lol. You could outcompete so many others. Plus, you got the premium feel/look [4], unlike most of these neo-banks.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.