I just saw the “forced to resign” thing and didn’t really get the fuss. If any employer wants to end any contract in a peaceful way he offers the employee the option of resigning.

That’s odd. Why? Why not fire them? I mean, you can let people go. In ch if you resign, you won’t get part of the unemployment salary, so no one should accept that kind of forced resign.

1 Like

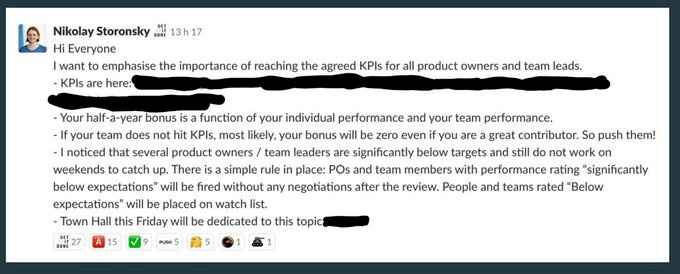

Revolut staff claim they’ve been told to quit their jobs or be fired

…and then being ineligible to receive unemployment benefits?

Not as easily in every country.

1 Like

Many people think it’s easier to find a new job if you resigned and invent a story why you did than if you were fired.

I think the problem is, if true, that they were forced to resign being told that otherwise they would be fired for underperformance.

Threatening employees with untruthful termination grounds would be pretty bad behavior.

3 Likes

Yes I agree theses methods are unfair. I moved to n26 2 months ago because they allow 5 cash withdrawal in euro per month which is what i am looking for my vacations in Portugal. Many small shops does not accept cards where I go.

The main drawback is that n26 only accept euro inbound… Not CHF.

I have to find the cheapest way to convert chf to eur before sending them to n26. Revolut or transferwise ?

Most certainly Revolut, when converting on trading days and staying below their monthly free conversion limit (5000£) on non-premium plans.

1 Like

5 Likes

Looks like revolut just became a bit less interesting, they’re changing their fee structure

https://www.reddit.com/r/Revolut/comments/h0ct5n/new_fees_starting_from_august_12_2020/

The new fees will be from 12th of August

https://www.revolut.com/legal/fees

The big change I see is that standard (free) accounts can only do 1000 CHF of free currency exchange per month.

2 Likes

Thanks for the information about the new 1000 CHF exchange limit… ![]()

![]()

Bait 'n switch

What’s next best thing? How’s n26 or neon?

It’s a simply change of conditions. The old conditions had been in force for months.

Bait & switch is when you aren’t getting what you signed up for - that doesn’t mean however, that the service have to continue providing these same conditions forever.

The biggest issues is maybe the exchange rate during weekends. If you spend more than 1k per month maybe it’s ok to buy the revolut metal imho.

Edit: reading that reddit post makes me happier about my english knowledge. it seems that people can’t really read.

I just got an email from them - in fact it will be 1250 CHF. Be aware also about the fee for exchanges during the weekend - going up from 0.5 to 1%.

4 Likes

The FX conversion limits have really been slashed…this was my reason for getting Revolut in the first place ![]()

I have thought of a work around and thought i’d share it with you: Neon gives you the Mastercard (& Revolut) FX Rate when you purchase in foreign currency. Top up in the foreign currency of your choice directly from the Neon Card (Credit Card Top-up) and you’ll get to keep the actual FX rate without any fees or limits, as the conversion is being handled by Neon and not Revolut. To my knowledge, there is no conversion limit for Neon.

If desired, I can also provide a referral for a Neon account, they’ll give you 10 CHF as a starterbonus.

If so… why don’t pay directly with Neon card? Unless you want to split money into 2 accounts…

Yeah? Neon doesn’t charge 1% on weekends. Why not just use Neon?

the point for me is the conversion of money, not spending it. i want to hold euros and spent the money at a later time. so do the other people affected by the 1250 chf limit. reasons for this can be multiple. suppose you want to reimburse a mortgage in euro for instance - you’d want this to be as cheap as possible, but neon charges 1.5% FX Spread on the conversion for SEPA transfers. by virtue of applying the top up method, you save that fee.

if not applicable to you, don’t use that method.

Why not use IBRK for FX trades?

1 Like

Complicated to open.

Relatively complicated to grasp and handle (currency pairs, buying and selling).

Minimum activity fee.

Expensive transfers beyond the first withdrawal each month.

If you have an IBKR account anyways (as I do), it’s a good option.

Opening up one just to do occasional FX exchange? Hardly worth it.

PS: Also, wouldn’t IBKR be slower, due to settlement delays before withdrawal is possible?

1 Like