Never heard Terry Smith speak until now. Strikes me as a very reasonable and humble man. And he basically uttered a threnody for Jack Bogle there, +1 for that.

Ugh… if only I had the courage to invest with him…

@Julianek: so did I understand right, you figured out recently that your net nets strategy is too time-consuming and that’s why you will invest a bigger portion of your portfolio with Fundsmith? May I ask what is your current overall allocation?

It is mainly that lately the market had gotten so high that the number of available net nets is absolutely tiny. As these are usually mediocre companies, you could not find enough to diversify (net-nets work well as a basket, but are way riskier individually). They are usually less time consuming though: you know already that they are mediocre companies, so you don’t have to check again and again that they are good businesses (quality checking is more time consuming).

So i have currently the below allocation.

The cash is high but comes from a recent bonus.

As you see i am mainly invested in Smithson (the small/midcap version of Fundsmith, available on IB), which provides the base line of my portfolio for good returns/low volatility.

It is also the basis for my opportunity cost. Anything I add to the portfolio should improve my opportunity cost.

I am also considering opening an account at their SICAV for Fundsmith (as it is a mutual fund, non-UK investors have to go through the SICAV in Luxembourg).

Finally, i guess most people on the forum should discard the last line(individual stocks) and replace it by the fund of their choice as I guess they won’t go into individual businesses.

If you don’t do point 2, but take e.g. VT - would you bother with / care about balancing out the small-mid-large cap “misalignment” which comes with overweighting small/mid with SSON?

If you don’t know accounting, you will have to learn it, one way or another. Accounting is the language of business, and you need to know how profitable a business is, how much capital it needs, and how much of its profitability you can expect to benefit you.

Any book will do, but as the topic is quite dry, for newbies i would recommend chapters 4 to 8 of The five rules for successful stock investing, by Pat Dorsey.

What makes a good business

Berkshire Hathaway, letters to shareholders, 1965-2019. Buffett’s letters are famous for a reason, and i learned a lot about what makes a good business in them. The topics are a bit random every year, so if you want them more organized, Lawrence Cunningham ranked them by topic in his book The essays of Warren Buffett : Lessons for Corporate America

The blog and lectures of Sanjay Bakshi. Sanjay is an indian professor and successful practitioner of value investing. Over the years he has amassed a lot of wisdom that he shares freely on his lectures (they can be a bit messy, but full of treasures, especially the company analyses), as well as on his blog. In particular, this article is a masterpiece.

Quality Investing by Lawrence Cunningham will give you the building blocks of what are excellent businesses

You will need to be able to evaluate management. This might look like a vague and daunting task, but your priority is to know if they are good capital allocators. No better book has been written on the subject than The Outsiders, by William Thorndike

Valuation:

Financial Statement Analysis and Security Valuation, by Stephen Penman, so you can get an idea of how the characteristics of a business make it worth more or less. You can also have a look at Accounting for value, by the same author.

Various good books

You can be a stock market genius, by Joel Greenblatt. Worst book title ever, but best book on special situations. Additionaly, the author has compounded at 40% per year for 20 years in case you needed credentials.

One up on wall street by Peter Lynch will teach you how to think about growth.

The joys of compounding by Gautam Baid: a nice recent surprise. I was pleased to see the number of important topics this book covers. I’d recommend it as soon as you have a broad idea about how business and investing work in general

100 baggers , by Chris Mayer: the author spent his life studying businesses that made a x100 in the stock market. While he admits he can never be sure how well he avoided survivorship/hindsight bias, he draws interesting conclusions always worth keeping in mind.

Everybody quotes The intelligent Investor by Benjamin Graham, but the book is really, really dry. I would advise reading chapter8 (the Mr Market Allegory) and chapter 20 (on the margin of safety).

Qualitative thinking

Poor Charlie’s Almanack, by Charlie Munger: in this book you will learn more about how to think , as well as about your cognitive biases, than anywhere else.

Seeking Wisdom and All I want to know is where i am going to die so i’ll never go there by Peter Bevelin: builds up on Poor Charlie’s Almanack.

More importantly:

Read financial reports. Reading books is good, but applying lessons and figure out stuffs for yourself will make you learn 10 times more. Pick a company you are curious about and download its annual reports for the last 5 years, and see how it evolved over the period. Did it get better at allocating capital? Did it grow earnings BUT reduced profitability, making it less valuable? Is management candid and telling things the way they are, or are they putting lipstick on a pig (you’d be surprised how often companies managements talk about “adjusted EBITDA” to try not to look bad…)

Well, there are so many books to read, but with those you should have an idea about where you want to go next…

Oh, and one more thing: don’t neglect the Sanjay Bakshi resources: they are really that good. Don’t be rebuffed by the Indian units he’s using, it is worth learning to understand his articles (1 lakh = 100’000, and 1 crore = 10’000’000).

If all the fund manager die in an accident, i would expect the company to liquidate the fund and return capital to shareholders. The value of the holdings would not move : the value of Microsoft does not change because a fund manager holding Microsoft passed away. Any other outcome would be an arbitrage opportunity.

I don’t know, I don’t think in terms of market exposure, but in term of opportunity cost. If my portfolio is expected to return 10% over the long term, then my opportunity cost is 10%. Every time i consider a new investment opportunity, i compare it to my portfolio opportunity cost. If I can reasonably think that I should expect 8%, then i don’t add it. If i have no clue (happens a lot), then i don’t do anything.

But the rules of the game is to try to increase the opportunity cost of my portfolio with sufficient margin of safety…

So to answer your question, with SSON i’d expect around 14-15% over the long term, same for FEF… VT would not make sense in this case.

Hey, just wanted to thank you for giving these resources, which are valuable as a primer on the topic.

Also, I wholeheartedly agree one should some (at least sometimes) try to think outside of the box and look not limit one’s horizon to US and, maybe, British sources, literature and research.It’s easy to become biased towards them for the simple fact that the biggest exchanges and financial firms are located are in these countries - and the language, obviously.

E.g., not discount resources because they originate from a supposedly “less developed” region or market in the world.Be that in more broader terms of “human development”, or in a narrower sense of less developed equity markets.

I assume the majority on this forum has a “buy and hold” strategy. But has anyone tried to sell out of the money, short maturity, call options on their underlying holdings?

Say one has a long 1000 shares position on company/fund XYZ at an average price of 4.00 $/share (i.e. total amount invested to date $4k). Let’s assume current price is maybe lower, say around 3.50 $/share, and a 4.00$/share call option with maturity 20th of May will be 0.05-0.25 bid-offer. What if you can sell 1 call option for say 0.15 $/share, then you can receive 15$ in premium. If the option will expire worthless (say price will be <=4.00 $/share at maturity) then you cash 15$ and your long position remains unchanged. If on the other hand the option expires in the money (i.e. price at maturity is >4$/share) then you’ll have to sell 100 shares of XYZ to the option buyer at 4 $/share. You still realized the 15$ profit but you lose the opportunity to gain more by selling the 100 shares at higher market price. In this case, the adjusted portfolio will be 900 long shares @ same average price of 4$/share + 415$ in cash. This of course works if you have a view that on 20th of May the price for this share won’t settle higher than 4 $/share.

Any thoughts?

It’s obviously a legitimate strategy and since Switzerland has no capital gain taxes, it costs you almost nothing to sell and buy again, unless of course you have to buy again at a higher price. This is a good strategy for a market moving mostly sideways. The taxman may find it questionable though.

As an alternative for buy and hold investors, a better idea may be to sell puts. I mean, you know when and what amount you want to buy. You can cash in the option premium as you go. Either your option expires but you keep the premium, or you get the shares you wanted to buy anyway, at a price you wanted to pay.

I am not an expert in options at all, but don’t you loose 85 CHF if the price goes to 5 for example, or 35 CHF if the price goes to 4.5 ? I understand you are earning the money your are loosing, but that is still a loss.

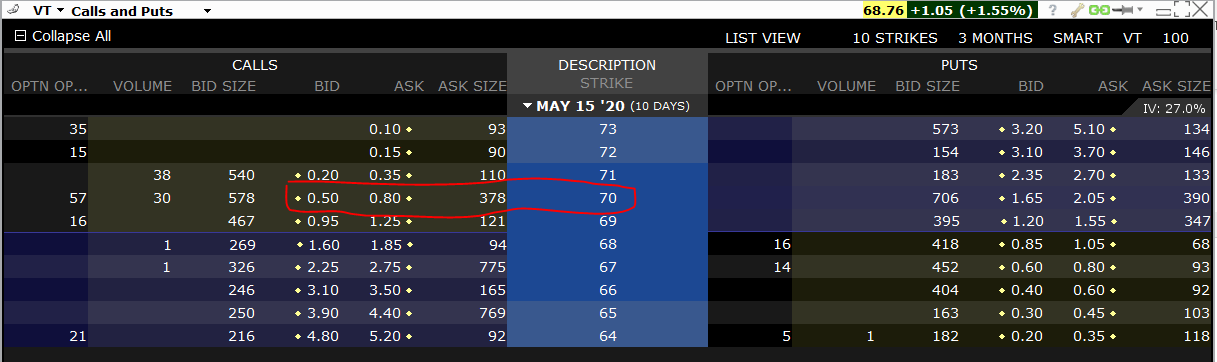

Let’s take my example with VT and assume you’re already long 1000 VT shares bought at an weighted average price of say 65 $/share (assuming you started investing more than 3 years ago). Here’s today’s options schedule:

So, you can sell 1 VT May 15’20 70 CALL @ say 0.60 premium meaning that you’ll cash in 0.60 x 100 shares = $60.

At maturity there are two outcomes:

if VT settlement price is <=70$/share, then the option expires worthless for the buyer and you get to keep your $60 premium and your VT portfolio stays unchanged (you still own 1000 VT shares, but the MTM value of this portfolio would have dropped depending what the price will be; however, this MTM loss you would have suffered anyway had you done nothing - i.e. didn’t sell any options - but it doesn’t matter as you are a buy and hold for long term investor)

if VT settlement price is >70$/share, then the option will have value for the buyer, who will exercise it’s right to buy 100 VT shares from you @ 70$/share. You’ll still get to keep your premium of 60$ plus you’ll receive 70*100=$7k from the sale of your 100 VT shares to the call option buyer. So in total your portfolio will now be comprising 900 VT shares (1000 your initial position less 100 that you just sold) and 7'060 that you can freely use for whatever purposes.Of course, if you haven't sold the option you could have sold now the 100 shares at a price >70 and would have made a higher profit, so this is an opportunity cost for you.

But, as I mentioned before, this makes sense in case you have a market view that the prices for VT may go down in the near future (say there are some really bad news coming up after economies are slowly restarting, maybe 2nd wave of infections etc.). Again, it involves taking a market view, it’s not passive investing (so that’s why I’m discussing about it in this thread).

Well, the 0.60 is a price in between the 0.50-0.80 bid-ask spread highlighted in the screenshot, skewed towards the bid price (one wouldn’t want to pay exactly the quoted bid, at least I wouldn’t - I almost always use limit orders). But you can use the 0.50 bid price if you just want to trade at market price…

And as I said before, this strategy is mainly used for generating some extra cash from your portfolio that takes a beating during a downturn.

Nonetheless, I do agree that selling puts makes more sense for “buy and hold” long term investors. This just dawned on me, but I think it’s actually even a better strategy than the DCA or, especially, VCA if you have a big amount that you don’t want to invest it all in one go (which, btw, might be the best thing to do as it was intensively argued and discussed on this forum).

I don’t like active funds either, but I like to actively invest myself a part of my net worth in companies I like believe have big upside.

The advantage of an individual investor is agility. You can buy 10k in a company and the price won’t move. Funds have more trouble to outperform in part because they buy/sell large amounts and move considerably the price by doing so.

Anyone knows a good online forum like this one, that is more focused on stock picking?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.