I agree that it’s not healthy to be dogmatic. But you probably remember Buffet’s bet on index funds vs active managers, that he won. I would say, if you make your decisions based on comprehensive research and if you’re really objectively skilled, then fine. But the problem is, most people who post their market-timing “advice”, do this based solely on their intuition, and it’s something we should be bashing as much as possible. Or am I wrong?

1 Like

The documents that were posted in this thread concluded that 83-90% of the funds underperform the market. We don’t know how many outpeformed the market significantly? How many of the remaining 10-17% matched market returns?

You still didn’t answer my question: how can I know which fund will outperform for the next 10-20 years? Basing my decision on past performance will decrease my chance of outperformance dramatically.

Maybe. But compared to what? By deviating from the broad market, I do run a risk of under- or outperforming. Quite obviously.

Did Buffet take a particularly “risky” approach?

Ben Felix explains it in his videos. According to the Fama-French model, you are rewarded with higher return by taking higher risk. You can reduce the risk/return ratio if you take risks independent from each other. The factors are:

- market risk

- size risk (SMB, small minus big)

- value risk (HML, high minus low)

- profitability risk (RMW, robust minus weak)

- investment risk (CMA, conservative minus aggressive)

If you take any portfolio, then the difference in returns can be in 90% explained by this model. This means, if you take more risks, it is expected that in the long term you will deliver higher returns. But risk is a cost of course. The question is, if you’re ready to take a higher risk than the default market risk.

3 Likes

Yes, i do remember. Buffett’s bet was against a fund of hedge funds (i.e a fund that invest in other funds) , which is an abomination from a fee structure perspective: you pay 2% management fees and 20% performance fees in the inner fund, and then again 2% and 20% in the outer fund.

That is enough to transform even a 20% annual performance in a 8% annual performance. No wonder the funds lost so badly.

But again, Buffett and Greenblatt say we should index, but they never did it themselves (and their investors thank them for that).

I agree with that. I tend to run away as soon as i hear the words market-timing. What I would note however is that:

- I did not see a lot of bashing when the Corona thread evolved into a “who bought VT at the lowest point” contest (which is completely market timing and goes to the antipodes of passive investing paradigm)

- This whole discussion was started after we talked about Fundsmith, which as a company is adamant about not timing the market, but buying (hopefully for life) wonderful businesses. No market timing there

But in general I agree with you: those giving market-timing “advice” should be able to back it up with sufficient proof.

And you still did not read the article i asked you to read, otherwise you would have found the answer to your question. Had you read it you would have indeed found that you don’t judge future outperformance by past performance, but by looking at the investment tenets and philosophy. That’s the same as confusing symptoms for rootcause.

Anyway, I won’t dodge the task, so let me explain why I personally think that, let’s say, Terry Smith and Mohnish Pabrai will continue to outperform (both in distinctive styles).

Terry Smith:

-

Fundsmith only invests in good businesses, which means:

- these businesses have a high returns on capital employed (on average 27%): for every frank invested in the business, it returns every year 27 rappen.

- with sufficient runway to reinvest around half of these returns in the business at the same high rate of return (they usually grow around 15% per year thanks to reinvested earnings, not additional external capital)

- have a high pricing power (on average 65% gross margin): that means that if the business build something that cost 3.5 CHF, it will manage to sell it for 10 CHF. It shows that there is absolutely no competition able to grind their margins.

- these businesses have been there on average for more than 50 years: it shows that competing with them is not easy.

- they are extremely cash generative: the earnings are real cash flows, not accounting accrued earnings.

- they usually on small, recurring everyday tickets, which makes them strong in times of crisis: people still brush their teeth and feed their dogs during the corona lockdown.

- to sum up, those businesses are compounding machines which should continue to compound their cash flows at a high rate.

- These businesses are quite rare: out of the dozen of thousands listed companies in the whole world, Fundsmith maintains a list of only around 75 companies filling those criteria, of which it invests only in 25-30.

- which leads me to my next point: Fundsmith does not diversify, and contrary to index funds, is not willing to mix good businesses with mediocre ones.

-

Now comes the question of valuation:

- Fundsmith just states that it tries not to overpay for a business (stating that they usually buy around 4% free cash flow yield), but this is where i did most of my research to understand why it works

- the first thought that usually comes to mind is that since those businesses are so good, everybody should know that, and thus investors should have bid up the price so much that these businesses do not offer any excess returns compared to other investment opportunities, right?

- however, this is simply not the case. There are countless examples of good and famous businesses that everybody knows and that continued to outperform. For instance, Pepsi was already a famous, outstanding and predictable business in the nineties, and still it managed to outperform the market during the following 30 years. Everybody knew about it, and yet it was still mispriced for 30 years. How come?

- my personal explanation is following:

- recall that the fair value of any asset is the present value of its future cash flows discounted at your opportunity cost

- if the price is too low compared to fair value it is either that the market uses a discount rate that is too high, or that the cash flows are under-estimated

- high discounting rate does not make sense: this would be equivalent to saying “the better the business, the higher the margin of safety i am asking and the worse the value of future cash flows”

- the likely reason is that as human being we under-evaluate the effect of compounding at a high rate, and so the human brain just underestimate the value of future cash flows.

- an example of this: would you rather have : a) 700’000 CHF now, or b) 1 rappen doubled every day for 30 days? The answer is b) because 0.01 *2^30 equals roughly 10’000’000 CHF. But the way the question is presented, our brain is not even able to grasp that proposition b) is worth more than ten times more proposition a)

-

Finally, once a business is bought, Terry Smith does nothing: he just rides the compounding machine as long as possible. It is not market timing, but time in the market. I would not be surprised if his turnover is even lower than passive ETFs.

Doing this allowed Fundsmith to compound investor’s money at around 15% per year, while enduring less volatility (i.e the risk as usually defined by volatility was much lower). On a risk-adjusted basis, the performance is phenomenal, and both Sharpe and Sortino ratio are there to testify it.

Mohnish Pabrai:

Although Pabrai also likes to buy outstanding businesses for life (Moody’s, Mastercard…), he invests more in what I’d call “high uncertainty, low risk” situations:

- high uncertainty = you have no idea what’s going to happen

- low risk: whatever happens, you won’t lose much money

- markets usually detest uncertainty, and punish companies who suffer from uncertainty, which means that often you can find quite interesting situations:

- For instance, he invested in Ipsco in the following situation (the number are from my memory, so they might not be absolutely exact, but you get the general idea):

- Ipsco was a steel maker, earning around 30$/share a year

- it had around 45$ of net cash on the balance sheet (that is, after paying debt)

- but it had absolutely no visibility on how the few next years were going to be. No visibility at all. As a result, the market had punished the stock to 45$ a year (brrrrrrr… uncertainty!)

- whatever happens, buying at 45$ was low risk because of the ample cash available in the balance sheet (limited downside)

- Pabrai said “you know what? why don’t i buy the stock and see what happens in the following few years?” He did that. After a year, Ipsco posted yet another 30$ returns (Pabrai had bought in fact at a P/E = 1.5), and went on to do the same afterward. Once the market understood that after more than 6 months, the stock went back past 150$ and Pabrai sold.

- This should not be confused with gambling. In gambling, you usually have fairly equivalent downsides and upsides. here, it is more like “Tail I win, Heads i don’t lose much”. That’s why this guy has been compounding at 26% since 1995 and why i think he will continue.

That was my thesis why those two managers (among my list) will continue to outperform for years ahead.

But since reading an article seems so difficult in your case, i reckon that doing the analysis above is many orders of magnitudes more difficult. Therefore i confirm : Cortana you should stick to indexing.

7 Likes

Yeah, that’s what I would have thought, too. Or at least now when everybody knows Fundsmith and their strategy, everybody should be like “ok, we have undervalued these stocks” and bump the price.

Your theory as to why this happens, while tempting, doesn’t fully convince me. People do not grasp compound interest, but their excel sheets do. So does their simulation software.

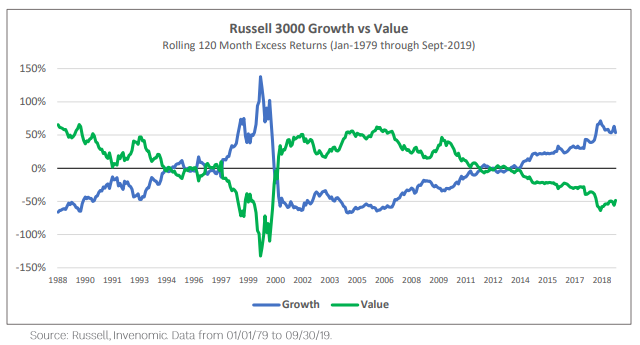

Judging by what you wrote, Smith is big on investing in value stock (low price, big earnings), but interestingly, value has been lagging behind growth for the last 15 years. I don’t know what to think about it… What Smith is doing just seems to good and easy to be true.

On comment on that part. While I would say that Terry Smith is a value investor, he is not in the sense of deep value, which is what I think your graph is comparing. He is a value investor in the sense of really looking at the value of the business. Most of his stocks have a PE ratio above 20 and are several time above book value. For example, he was owning Neslé for some time and owns Microsoft. I would really suggested to read his owners manual and his letters to shareholders or watch his annual shareholder meetings. Even if this does not convince you, I do think their content is insightful for every investor.

What I do like about is approach is that he really does not try to do anything fancy and once he owns a stock, he is very passive.

3 Likes

By the way, how do you guys invest in Fundsmith? Directly with them or via ETF?

If by “value stocks” you mean “low multiples” (i.e the value factor in Fama/French model), then you could not be further from the truth. Fundsmith’s holdings have actually quite big multiples (see below some of their current holdings). But that’s the point: even at these high-looking prices, my interpretation is that it is still not enough given how these businesses will compound.

And don’t switch band and say “then it’s growth stock!”. Smith has been operating since 2003 and in the meantime, both growth and value have had their ups and downs. (*)

| Company Name | Symbol | Market Cap | Currency | Sector | Price | P/E |

|---|---|---|---|---|---|---|

| Microsoft | NASDAQ:MSFT | 1,350,719,907,560.00 | USD | 177.58 | 31.03 | |

| Paypal | NASDAQ:PYPL | 129,733,474,225.00 | USD | 110.62 | 53.74 | |

| Philip Morris | NYSE:PM | 120,504,432,389.00 | USD | 77.32 | 16.82 | |

| Estée Lauder | NYSE:EL | 60,708,364,964.00 | USD | 168.85 | 33.56 | |

| Stryker | NYSE:SYK | 68,023,783,838.00 | USD | 181.48 | 33.52 | |

| Idexx | NASDAQ:IDXX | 22,624,995,558.00 | USD | 265.47 | 54.05 | |

| NASDAQ:FB | 507,311,093,984.00 | USD | 177.95 | 27.86 | ||

| Intuit | NASDAQ:INTU | 67,966,793,377.00 | USD | 260.92 | 42.31 | |

| Novo Nordisk | NYSE:NVO | 116,269,087,484.00 | USD | 62.34 | 26.24 | |

| McCormick | NYSE:MKC | 20,792,142,381.00 | USD | 156.26 | 30.05 | |

| Sage | LON:SGE | 6,844,329,691.00 | GBX | 628.00 | 26.20 | |

| L’Oreal | EPA:OR | 133,730,483,133.00 | EUR | 249.80 | 37.37 |

Smith’s strategy is not really new… Buffett has been saying the same for at least 40 years “it is far better to buy a wonderful business at a fair price than a fair business at a wonderful price.”

Now the real question is: how many funds do really apply this?

- buying very good business and only good ones

- do nothing

- do not diversify with mediocre ones

This seems simple, but in my experience it is actually quite hard to find these funds. If you find some tell me, i am interested.

I have my own theory (which is in fact more an hypothesis than a theory): the asset management industry is about charging a fee on AUM, rather than absolute performance. Viewed under this lense, the average manager would think:

- you should not depart too far from the index, otherwise you risk to have a seriously different performance than the crowd. It is better to be wrong with the crowd, than right on my own, i could lose my job

- if i follow a “index closet” strategy by investing in a hundred stocks, no stock will harm me, but none will contribute significantly. I may underperform after fees, but hey, my client are not so sophisticated and as long as i get my fees and the clients won’t go away, why do something else?

In summary, for an average manager, carreer risk (losing your job) is more important than portfolio risk. Otherwise managers would stick to what works.

(*) growth and value are two terms defined by modern finance theory, and are not the same as what most investors define by value investing, which is buying something for less than it is worth…

7 Likes

On my side, for now only in Smithson, which follows the same principle but in smaller cap companies. So I cannot answer yet. But if I would, I would most likely do it directly with them.

This thread is a GEM, and we should all thank @Julianek for his free lessons on investing here!

I was one of those who 5 years ago thought “I’ll never be an active investor because it’s baaaaaad and they always lose!”

But then I realized that it’s not black/white. It’s not a 100% passive vs 100% active game.

I myself am picking an “asset allocation”, which inevitably makes you an active investor of some sort. How much stocks? How much bonds? Which stocks? Which index? What the hell is “the market”? Buying VT is the market? S&P 500? The Dow? Does one who invest only in NASDAQ is beating the market? What is the market? Am I “passive”? No! I’m both choosing among indexes, and trying to deploy my money into the market with some discretionality in timing (i.e. I’m moderately timing the market)

On the other hand, an “active investor” who picks 10 stocks and stick with them for the next 50 years, never logging in into their brokerage account forever… looks pretty passive to me!

The more I read, the more I understand that YES, the market (however you define it) is beatable, even in the long term. It’s a tough job, it has costs (your effort and time), it has high chances of failure, but it’s beatable. I clap to those who succeed in that. It requires a lot of skills (mostly psychological), and it’s the reasons why it pays much more than being Cristiano Ronaldo.

Does it mean I’ll change my mind and become a true active investor? No, for now. Maybe one day I’ll be more active. I’m ok with considering myself 80% passive, 20% active at the moment. Maybe in future I’d like to try that “job” of understanding businesses and investing in the good ones.

But at the moment I’m not putting in my time, and I shouldn’t even be as active as I am right now. I should be more 90/10, and my irrationality might cost me money. Just sheer luck that I sold at high in November and purchased (maybe) discounted stocks during Feb and March.

The point is: making it a “religions fight” is childish and plainly false. Active investing is a thing, and it works under some circumstances. The vast majority of people should not try that at home, but that doesn’t falsify the statement.

7 Likes

Are you not afraid that the fund is getting to big and will lose it’s edge?

Out of curiosity:

Given that they are pretty open about the holdings (but perhaps not their proportions) - and that there are indeed very few of them - why not just replicate them yourself instead? (and do e.g. equal weight)

One could argue “it’s too late to buy because the price is high now vs. when he bought”, but that’s not the right viewpoint - he wouldn’t be holding them if he didn’t believe in their long term gains, no?

Time, effort, taxation.

You could but as you mentionned, you would have to equal weight, which they do not do. For exemple, if you read their 2013 annual shareholders letter, you will see that they sold five of their holdings during the year and he explains why. Here, I will just quote the first paragraph which is a more general explanation, afterwards, he gives individual reason for each stocks.

Although our turnover was once again very low in 2013, we sold five holdings: McDonald’s, Schindler, Serco, Sigma-Aldrich and Waters Corporation. There may seem to be an inherent contradiction between the fact that we sold five holdings yet our turnover was low. Part of the explanation is that some of these holdings had already become an insignificant proportion of our portfolio because we had been struggling to add to them as their valuations had become too high to represent good value in our view. Once this point is reached it begs the obvious question of whether we should in fact sell our holding to make way for an investment which offers better value, either within our existing portfolio stocks or from within our wider Investable Universe of stocks on which we maintain research.

So if you would do an equaly weighted portfolio, you would have reinforced those five stocks while they were, according to them, overvaluated. So if you want to do that, you start to need a valuation model similar to theirs. I guess that this can be done to some extend since they explain which characteristic that look at.

2 Likes

If they are buying and selling that often, then the comments above of “passivity” and “buying for the long run” fail. ![]()

What taxation? You are not doing day/month trades with this, you are holding them longer I suppose.

Time and effort - not much really (again not trading daily or monthly as per their strategy).

1 Like

Two additional points on this:

-

Just to confirm that our brain is absolutely horrible at handling compound interest (an exponential process), here is an interesting link on the topic. Quick summary: you may think that the brains thinks at least linearly, but it is even worse: most often the brain behaves logarithmically. For instance, when we handle millions, billions or trillions, we do not have a grasp of the scale change, we just add zeros in our minds. Juggling with an exponential process is then absolutely impossible.

-

To answer your exact point about spreadsheets, i thought the same. I have an hypothesis about it, but so far i am not sure yet if i developed it fully (beware, it is a bit technical)

- as said before, most analysts will do a discounted cash flows valuation to value a business (i am not fan of this, but this is what is taught in most business schools)

- the discounting rate is usually around 10%, and for exceptional businesses like the ones held by Fundsmith, there is no reason to think that it should be higher

- Now look at our businesses: they are compounding at 15+%. When you do discount cash flows growing at 15% with a discount rate of 10%, it does not converge, the value is infinite…

- Therefore, in most spreadsheet models, the analysts say that the business is going to grow at 15% for let’s say 10 years, after which the growth will be more modest due to increased competition (usually the 4% GDP growth). With this adjustment, the model converges to a value.

- Now it happens that your valuation is very sensible to the limit you set for the number of years of good growth: many analysts use 5 years for normal businesses, 10 years for businesses with good visibility, etc. But what happens if the business actually continue to grow for 20+ years at a good rate? Your valuation will be wrong by a 100% margin… This could explain why analysts are so off the mark when valuing businesses, but as said before it is just an hypothesis, i need to dig it further…

For Fundsmith, investors outside the UK need to subscribe to their Luxembourg SICAV (a kind of mutual fund). You send them directly the money, it is not listed on an exchange. Smithson on the other hand is a closed end fund listed on the London Stock exchange, and thus available on IBKR.

Fundsmith is currently $20 billion AUM. It has around 30 holdings, all of which have a market cap of more than 70 billion. 20b/30 = 700 million to allocate in each position, which is still quite liquid. Using the same principles, Buffett grew BRK to $500 billion so I am not too worried.

Yet San_Francisco is spot on: if I’d do it myself, even if i do not trade, I have still 30 businesses to manage, which implies:

- reading all financial reports, making sure that the businesses are still impeccable, looking for financial shenanigans/management mislead. You could say that since they are in FEF portfolio it should be OK, but Fundsmith communicate on buys/sells only once a year, and i could learn about an issue way too late

- This is an awful lot of time, given that it is not my full time job. I am much more at ease with 8-9 positions to manage. This way i know these 8-9 companies from the inside out, rather than 30 + businesses that i know vaguely. To give you an example, @ecthe spends quite some time calling directly CEOs/management of companies he is investigating. Imagine doing that for 30 companies every quarter…

- Others might be more comfortable with less diligence; I know it is not for me though, as I tried something similar in the past.

- And finally, although it is not a decisive factor, i can assure you that it is not a pleasant moment to fill your tax declaration (especially the Wertschriftenverzeichnis), when you have so many holdings that you need two additional sheets… 10 holdings is much better

So in a nutshell, i am more comfortable outsourcing it to Fundsmith/Smithson, having one big line in my portfolio that will provide good returns with low volatility, and which acts as the opportunity cost for my other 8-ish lines.

But i concede that you are right, Fundsmith is quite open about their holdings, and in theory you could approximate their portfolio once every year…

Well thanks a lot MrRIP! Happy that it did provide some food for thoughts…

6 Likes

When holding individual stocks: Are you going to reclaim withholding taxes on (applicable) dividend payments from a multitude of foreign tax authorities? Is it even worth to get the required documents issued from your broker?

Granted, if you don’t, the (potential) loss in unreclaimed withholding taxes on individual stock holdings will be less than the costs and charges in Fundsmith - but it does narrow the gap.

1 Like

Interesting observation, and intuitively it seems correct.

Why are you not a fan? What other way would there be to calculate present value of future cashflows?

Your theory certainly gave me food for thought. It is indeed tricky to calculate. Still, I think that people who really influence the price with their trades have a good understanding of how it works. I can’t imagine that someone like you or me, even if there are millions of us, can keep the market constantly out of balance?

Discounted cash flow (as well as discounted dividends) doesn’t really measure value generated. A company can have a negative cashflow (e.g. because of big investments) and has still generated a profit. Investments generate cash flow, but investments often cost cash at a much earlier time. Stephen Penman says

we preferred to call free cash flow a liquidation concept rather than a value-added concept and, in doing so, called into question the idea of forecasting free cash flows to value firms’. We recognized, of course, that forecasting free cash flows for the long run captures value. But that goes against our ctiterion of working with relatively short forecast horizons and avoiding speculative valuations with large continuing values.

Now, you can try to predict value added, but that has the chance of not materializing in cash when it’s necessary. I’m not sure (yet?) what the right way to go about this is, but @Julianek probably can say much more about this.

1 Like