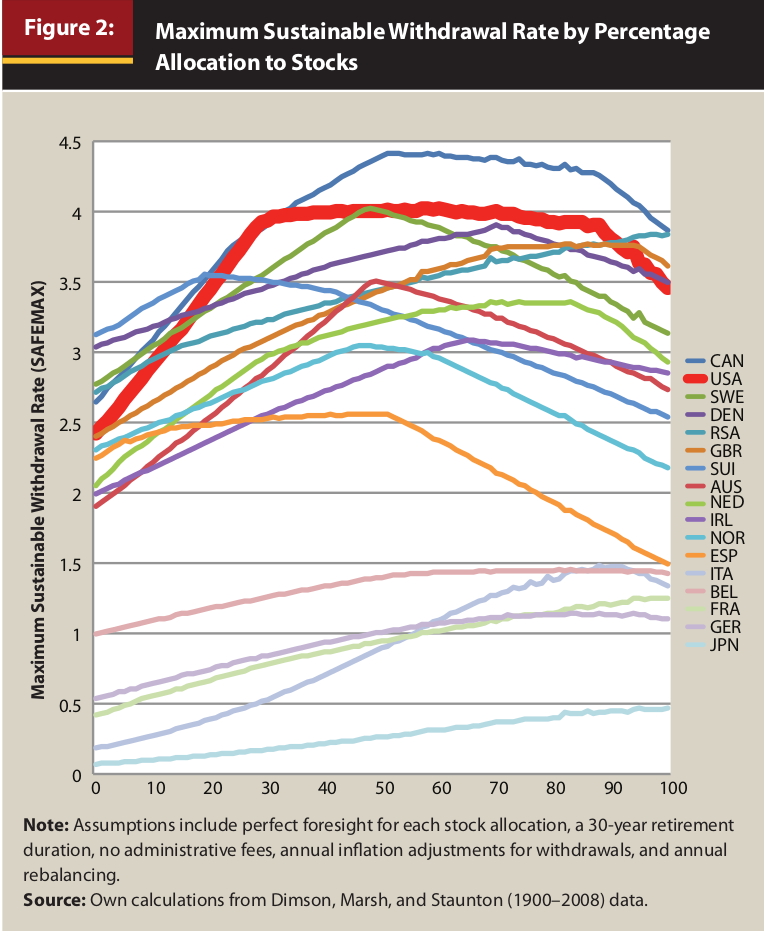

Today I was wondering that most of the studies like the Trinity one is using US or World indexes, or at least that’s what I’ve read/thought.

I wonder if there is a study or at least a nice graph that show that even european or world ex US market behave the same way.

I’ve seen a vanguard ETF (world ex us something) that for the last 10 years made less than 1% gains.

Are we basing all our strategies by studying the us market?

Trinity study is limited (flawed) in various ways. There were a number of other studies that attempted to fill in some gaps. But nobody should be concluding from the Trinity study that we can invest a pot and assume that 4% will give us a safe early retirement. Unfortunately, many seem to do so because:

they haven’t read the study

they didn’t understand the assumptions/limitations/parameters

they didn’t look at the differences between their situation and the scenarios envisaged by the study

VT has currently around 60% US. US exposure grew over time, too, I believe it was around 53% 1-2 years ago, can’t find the exact data on it. US performed very well in past x-years, far better than Europe, Asia and emerging markets. VXUS/VEU, which I assume you mention in OP, did perform very poorly vs VT and esp vs VOO/VTI. They typically have a higher divident yield ~1.6-2% on VT/VOO vs ~3% on VXUS in the past. Is past performance indicative of future performance?

No that‘s just the Japan scenario. Something like 66.6% VT 33.3% domestic bonds should give you a SWR of 3-3.5%. I can‘t find the specific study right now.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.