Hi Everyone!

I am looking for some advice on how to fix my 3rd pillar mess up. When I moved to CH, 15 years ago, I fell pray to an unscrupulous insurance salesperson and signed up for a 3rd pillar life insurance account with Genralli. I have contributed the maximum allowed 15 years ago for all these years. Now, as I am getting older (48 yo) I have started looking a bit closer into my retirement funds, and came to learn what a costly mistake I’ve made.

I would like to stop contributing to Generalli and use another 3rd pillar solution. To date I have contributed about 98k. Options are:

a. I stop the contract and leave 85k, which is the current value of my 3rd pillar until I am allowed to withdraw it.

b. I break the contract, with the surrender value of 65k, and move these money to VIAC/Finpension for the remaining 15 years.

c. Or of course there is also the option to do nothing and continue the policy ( however I have no dependents, so no need for a life insurance per se, and the only useful thing would be the disability insurance 2500/mo).

I am not very knowledgeable in finance matters, and a couple of times I’ve tried to get advice, it ended up with people trying to sell me things. So I would be grateful for your insights on what should one do in such a situation. Many thanks

Just to be sure , if you have contributed 98K so far, how come the surrender value is 65K and current value of 85K? Was the money not invested anywhere?

Option C

Perhaps it’s also important to also determine what is the end value for option C.

how long is the contract

Is there any guaranteed some at the end of contract

Option A

And in option A , what would be the final value by end of the contract?

Thanks Abs_max and Markus ! Option C, the contract all together is 30 years, started in 2009 and it is supposed to finish in 2040. The guaranteed amount is 176 k, which is 20k less if I would just saved the monthly contribution. They showed me at the time some fancy calculations with a 3%, 5%, 7% but based on today’s value it is all BS. I do not have dependents, so I do not need a life insurance, as for the disability insurance is anyone’s guess. I have a good income, and I am paying the mandatory 1st and 2nd pillars.

For option A, I’ve asked if that amount would accumulate any interest and I was told no, the money will just sit in the account until I turn 60 and I can access it.

Nothing comes free in this world, but all this looks like a quite bad deal for the customer and a sweet one for Generalli. Thanks!

First of all this is indeed quite complicated scenario. In each case you lose money from pure investment perspective. Of course there is life insurance element but seems that’s not the key requirement anyways for you.

So I think all scenarios need to be calculated to get the overall picture and estimate the final value

Scenario A -: 85K + all future contributions invested in Finpension/ Viac

Scenario B -: 65K + all future contributions invested in FP/Viac

Scenario C -: 176 K guaranteed + some fancy value which we don’t know (assuming all future contributions are continued)

From purely final value perspective, scenario B beats scenario A because 65K invested with 3.5% expected return would lead to 108K in 15 years while the 85K remains 85K. At 1.8% return, scenario A and B would be equal.

Do you happen to know what’s the final taxation? Are insurance schemes also taxed at lumpsum tax or they are tax free at end of contract?

I would still suggest to ensure that options recommended to you are really the only real options. I feel this contract is very one sided.

Seems like getting out everything and taking the surrender value is the best option, if you otherwise see no value in the insurance part. And if it really will generate 0 return otherwise.

You will just lose money to inflation over the next 15 years.

At a moderate 5% return you‘ll have almost 140K after 15 years.

Go to Finpension or Viac with the money.

100% stocks for now would still be ok. Start shifting more to bonds in about 5 (if the market is not down at that moment). And then gradually increase bonds till retirement, towards 50/50.

Or do a classic 60/40 portfolio right from the start and never worry about it. It‘s the classic risk adjusted return optimized portfolio, that will work in most market environments and will likely yield a solid return with moderate drawdowns over the investment period.

The qestionaires of the providers should give you some guidance here.

E:

Here a quick backtest through one of the worst decades of investing (dotcom bubble 2000 and GFC 2008) for the 60/40. This really is close to a worst case scenario for your situation.

In USD and with an US only bond fund. It’s just to give you a rough overview on what it can look like.

Option A is to not pay any more premium and get 85k at age 60 (in 12 years).

Option B is to not pay any more premium and get 65k right now.

If so, option A means a guaranteed 2.26% compounded annual rate of returns (CAGR) on the 65k. That’s probably more than you could get in CHF denominated bonds (the 10 years yield for bonds of the Confederacy is at 0.46%).

I would think about it in terms of asset allocation. If you want more bonds, then that policy seems like an attractive way to get somewhat of an equivalent to them. If you don’t care for bonds and want more stocks instead, then transfering the surrender value to another 3a solution might be an attractive solution.

The most important question here is how the 176K final guaranteed insurance benefit compares to the sum total of the premiums paid up until the policy matures. Once you determine the return (insurance benefit minus the total cost), you can then compare the opportunity cost vs. other pillar 3a solutions.

If you would otherwise buy disability insurance and life insurance (pure insurance, without cash-value), you can deduct the total premiums for identical stand-alone insurance offers from the total cost. But from what you wrote, that isn’t the case.

It is important to be 100% sure that the 85K when the policy matures is actually guaranteed if you put it on hold and stopped paying premium. My hunch is that only the 65K cash value is guaranteed.

You should also check whether the life and disability insurance would be cancelled or put on hold as well, or if you would have to keep paying for that.

From a tax perspective, there is no difference between a pillar 3a life insurance and any other pillar 3a solution. You always get the pillar 3a tax deduction, and the assets/cash value are exempt from wealth tax. You pay the retirement capital withdrawal tax when you withdraw (or withholding tax, if you leave Switzerland/EU).

An important question is whether you are willing to invest in the stock market and other unpredictible assets as opposed to having a guaranteed return (assuming there is even a return, as per the calculation above). There is no guarantee that the stock market or commodities will perform well over the next 15 years, although it is likely if history is anything to go by. If you prefer to stick with investments that give you a guaranteed return (at least in Swiss franc face value terms), then you may come out better with the insurance than with pillar 3a savings accounts (again, that depends on the return as per the calculation above).

If you believe that the stock market or commodities will gain enough value to compensate for both the cost of surrendering your policy and the guaranteed return, then stocks would be the way to go. Based on historical performance, you would likely end up with more. But no guarantees.

Many thanks Daniel! The 85k are guaranteed when I turn 60. The insurance would be cancelled, I will only have a document saying that they have my money. I am planning to call to see what is the minimum I can pay, as if it is a reasonable amount, that could be a solution to. As to what I would do with the money, I would put them in VIAC/Finpension.

If the 85K are guaranteed without any further payments, then my personal advice would be to just put the policy on hold until you turn 60, and count it towards the cash portion of your portfolio. I know many here would disagree, but 15 years isn’t a huge amount of time in stock market terms, and you would start off your investment with a 20K loss to recover.

Of course, you should ideally have enough other capital to balance the portfolio with stock investments.

Personally, I would strongly advise against making even minimum payments to the insurance. As it stands, you’ve essentially spent 13,000 francs on life insurance and disability insurance, which is probably more than it would have cost you to get those insurances on their own. If you don’t need those insurances, why waste any more money?

I recommend checking your pension fund plan (pillar 2) to see if it includes additional disability insurance. If it does, you probably do not need additional pillar 3a disability insurance in any case.

What is very weird is that your current value of portfolio is 85K while the contributions are 98K.

With stock markets and real estate at all time high, Generali should explain to you why the current value is 13% below contribution value.

Anyhow- if such performance continues, then adding more money would mostly add more agony.

This brings us to only two options

A- freeze and withdraw at end of contract

B- withdraw and reinvest

Option B comes at a 20K loss which is too high to ignore. I think it might be wise to take a bit of pause.

So perhaps what could be the game plan is following

freeze the 3a insurance

Start Finpension or VIAC or truewealth for future contributions as of 2025

take sometime to define your overall asset allocation (including rest of the investments). This would help you decide if it’s worth withdrawing funds or just leave them there.

generali can be viewed as bonds with 15 year term generating 1.8% CAGR

Let’s say your total assets are worth X (across 3a , taxable accounts everything)

X = G(3a insurance) + C(Cash)+ S(Stocks/Etfs) + B( bonds / bond etf)

Unless B = 0, it would not be wise to withdraw G at loss.

It’s because insurance providers’ ETFs are DOGSHIT, my supposed global market cap weight bullshit ESG portfolio with Swisslife did 1.3% in 2023 while VWRL did nearly 11% in CHF.

It’s basically a gift to the insurance agencies, free float. You pay close to 1200/year for a life insurance that’d be pay (my family) 150k, while a 500/year life insurance with eg Baloise would pay 400k. Plus the contributions (to their shit products) if you become unable to work. I’m ferociously against insurance 3A, but in OP’s case, considering both age and size of lost contributions, I’d probably freeze it and go with a proper provider like VIAC/Finpension.

I have to confess, I’d read the insurance 3A horror stories here but I’d have probably stayed if it was making anywhere close to market gains. That 10x difference in performance was my wake up call, thankfully only cost me 5500 as I’d only contributed for 2 years. With Finpension since early Jan 2024 and happy about it.

But also the simple explanation is that the 13k (98k-85k) is basically the insurance premium you would have paid for a simple life insurance with similar benefits? (Plus or minus)

The amazing thing is that they wrap this “selling life insurance” into a “3a investment product” that makes you believe you’re saving for the future. However, after removing all the fancy wrapping it’s still just a life insurance that you bought and paid for.

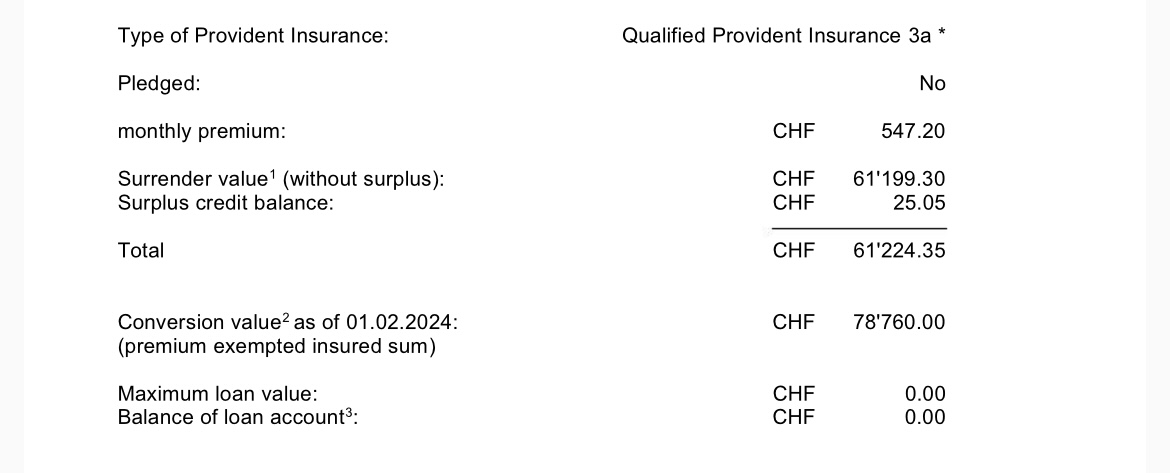

Thanks everyone for your kind thoughts. This is the statement from January, somehow I cannot find the latest, but since then I contributed another 5000 fr roughly. I checked their investment fund, is 98% Swiss bonds.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.