Assuming I stop working before 60 and leave my current pension fund, thus transfering my 2nd pillar assets to someone like ValuePension. Gives you the opportunity to withdraw it till 70 instead of 65.

Yes, didn’t I mention it as an exception above?

No, I didn’t.

What amounts are you assuming here?

If you are employed and restricted to lower yearly (around CHF 7k) pay-in amounts of approximately 7000/year, you’ll maybe contribute a total 300k to pillar 3a over a lifetime of work (and that doesn’t account for considerably earlier retirement).

It depends on the end value of your investments. Saving multiple “10,000s” in tax seems a bit optimistic (for pillar 3a alone), cause the progression isn’t that high.

Still, as there is no drawback except a bit more paperwork, I see no good reason not to split.

Yeah, why not also turn around three times and say out loud “How much wood would a woodchuck chuck if a woodchuck could chuck wood?” everytime you want to check your balance? I’d do that for 10k in tax savings, so why didn’t they add other extra useless annoying stuff in their flow?

40.7k CHF will more than double in a 22 years horizon.

Good point Still I have problems with stupidity

Again, good point. I’m the stupid

Thanks! I didn’t know you can partially withdraw from a portfolio/account in case of buying a property (which is usually the only early withdrawal case where they ask you for a fee)

How can you have more than one Pillar 2 accounts?

Are you playing with fire and leaving money on a Vested Benefits Account while having a fill time job with Pillar 2 contributions?

"Theoretisch können auf diese Weise Gelder aus der gebundenen Selbstvorsorge sogar in elf unterschiedlichen Steuerperioden abgerufen werden (wenn die Säule 3a bis zum 69. Altersjahr bei Frauen bzw. 70. Altersjahr bei Männern bestehen bleibt).

Jeder Kanton hat seine eigene Besteuerungsregelung bezüglich der Staffelung von Kapitalleistungen aus der zweiten Säule und der Säule 3a. Das StHG sieht diesbezüglich keine Regelung vor. Es gibt beispielsweise Kantone, die gestaffelte Kapitalleistungen aus der zweiten Säule gleich wie einen einzigen Kapitalbezug im Jahr der ersten Zahlung besteuern. Andere Kantone wiederum fassen alle im Verlauf von fünf Jahren bezogenen Kapitalleistungen aus der gebundenen Selbstvorsorge zusammen, so dass der gestaffelte Bezug die Progression nicht durchbricht. Da die Möglichkeit der Staffelung nicht gesetzlich sondern in der Praxis geregelt ist, ist die zur Anwendung gelangende Regelung für die Steuerpflichtigen nicht immer sehr transparent"

If the federal tax administration acknowledges that there are limits and anti-circumvention rules/rulings on tax optimisation through staggered withdrawals, I wouldn’t discount the possibility that that will also hold up at the Bundesgericht.

Hopefully you’re at least 10 years older than me and keep us updated on this forum when the time comes.

When retiring early, you get a vested benefits account. You can completely officially tell you PK to send the money to two different vested benefit accounts (split). Just make sure they are at different foundations.

A vb account will not automatically trigger payment when you reach 65.

Viac opens 5 portfolios for you automatically, am I right?

In VIAC you have to create an account 5 times, and if I remember well, have to go through the list of questions each time, but it’s just a few clicks. Not possible to open 5 accounts in one shot. Once you create the first account, it’s quite quick to create the 4 remaining, something like 10mins.

@MrRIP I have seen that the questions have already been answered in the Forum. I just wanted to add one comment: We create a risk profile for each portfolio, as the investment horizon can vary for each portfolio (e.g. in the case of a planned advance withdrawal for home ownership). The other questions from the risk profile are related to loss management and financial knowledge and are recorded at client level. A modified answer to these questions will therefore update all existing risk profiles.

Is the split defined by the obligatorisch & über-obligatorisch parts (i.e. for most people that’ll be about 80:20 or 70:30) , or can you choose any split you’d like (typical choice would then most probably be 50:50)?

(I’m not sure if you can split between mandatory and non-mandatory part. Though I think I have reversely seen such from AXA as payment instructions for incoming transfers into some of their pension funds).

Hi! Very interesting topic, I’m definitely thinking about a switch from VIAC towards finpension…just a quick question that I look and didn’t find an answer for : does someone have an idea about the costs of the switch?

I mean, they would probably sell everything on VIAC and rebuy everything in Finpension…no?

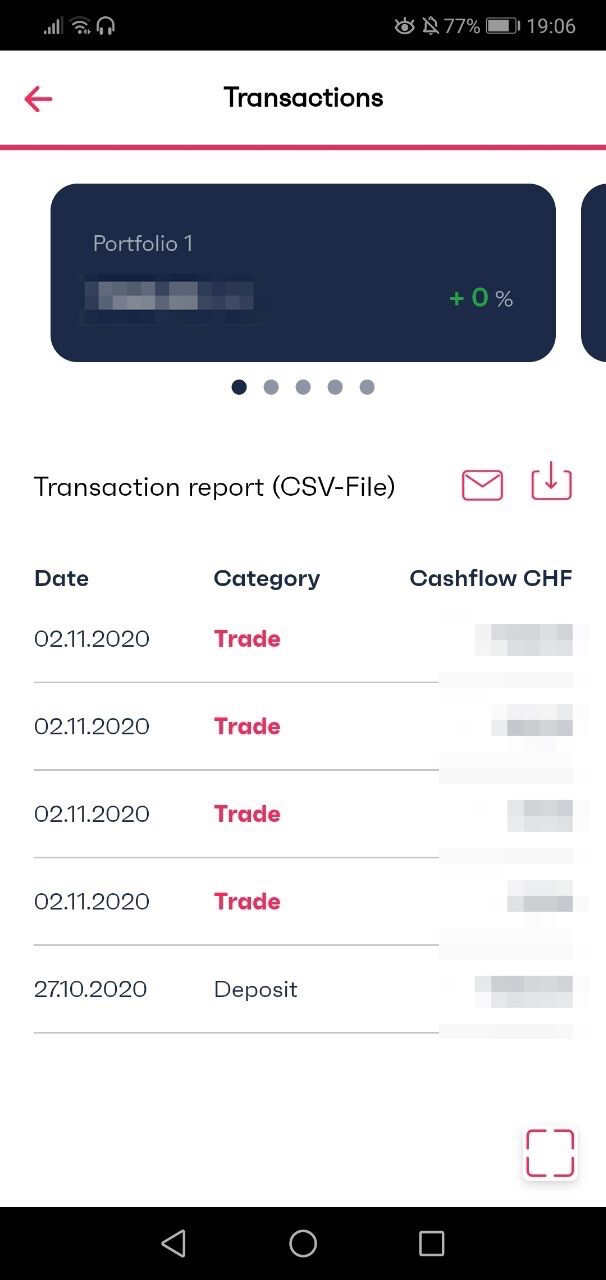

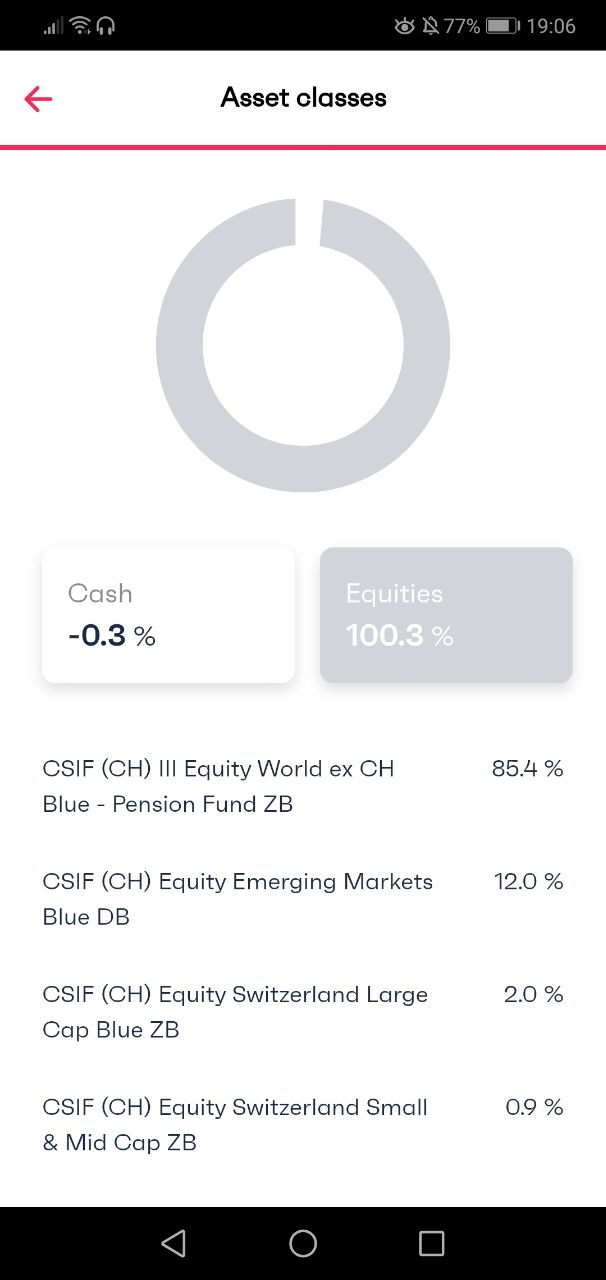

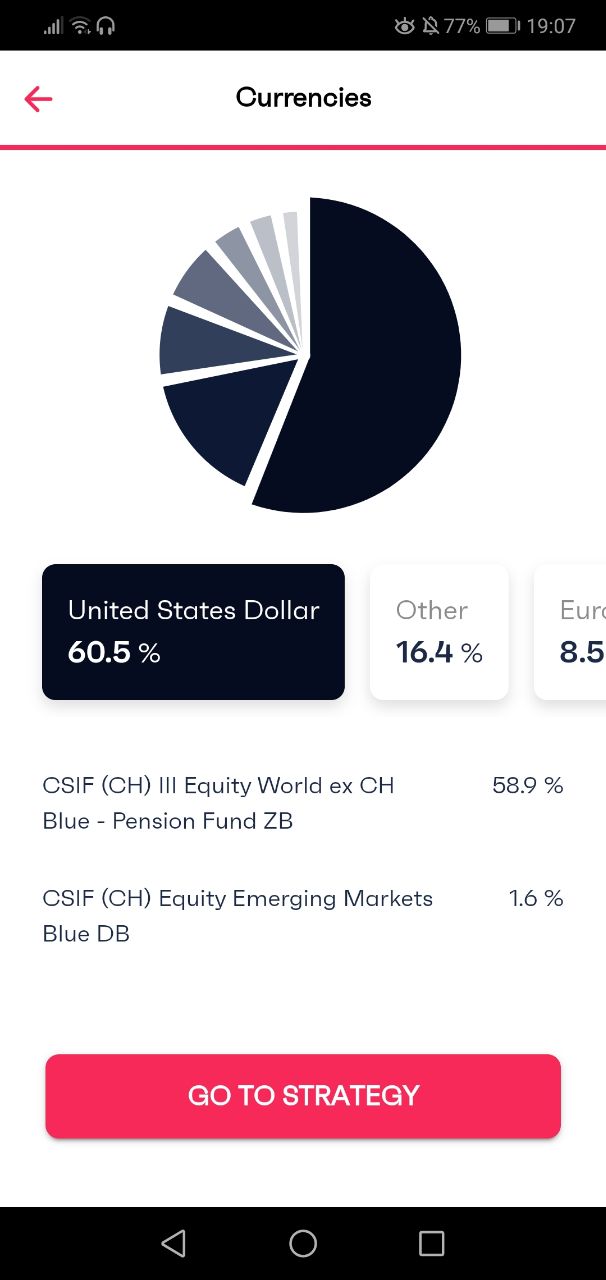

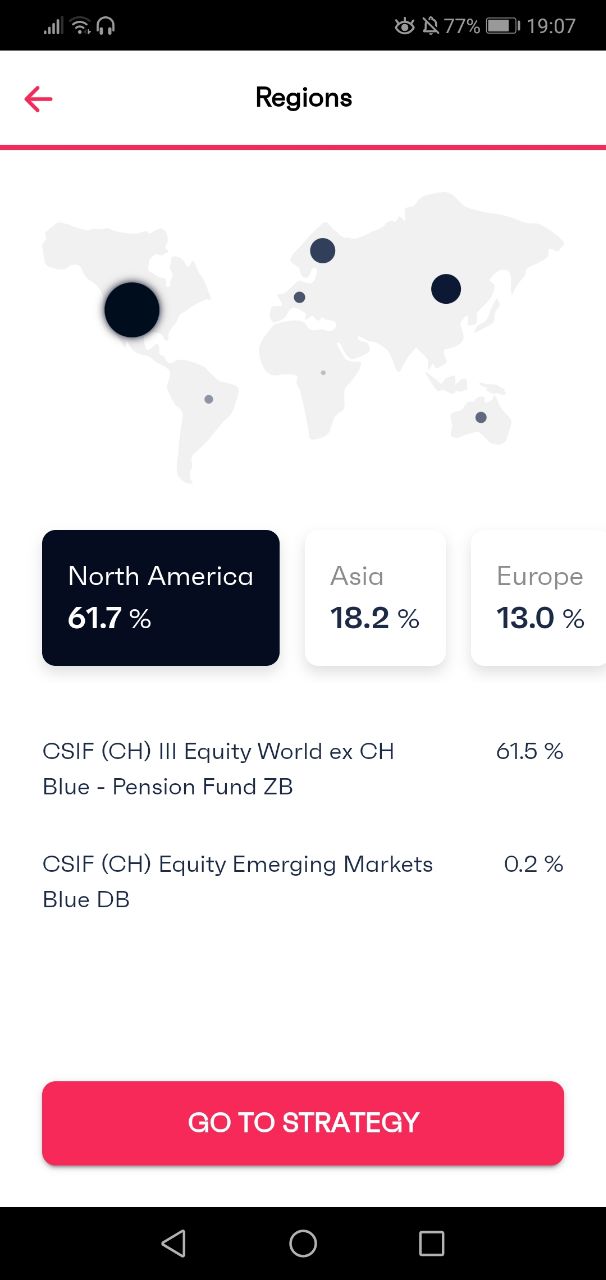

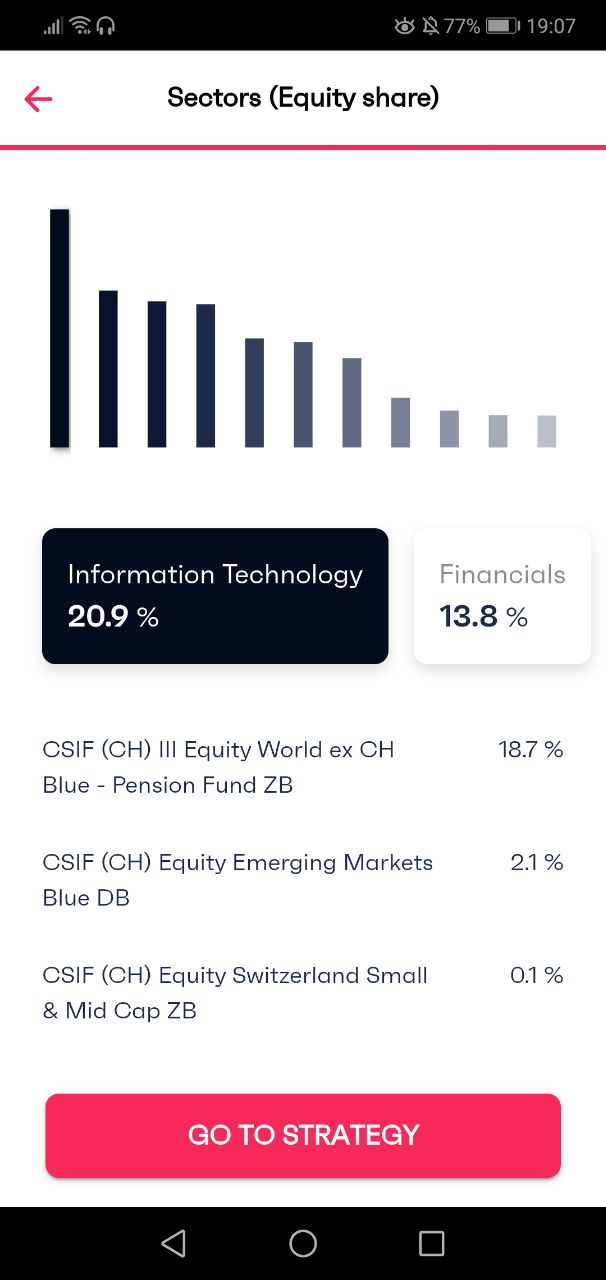

Below some screenshots from my first experience with finpension. The trades correctly occurred on 02.11.2020. Please note that it took around 3 days to update the information in the app.

Indem du dieses Forum liest und daran teilnimmsch, bestätigsch du, dass du d Forum-Richtlinie glese hesch und damit einverstande bisch, sowie mit em Haftungsausschluss, wo uf http://www.mustachianpost.com/de/ präsentiert wird.