Good thing that there are (at least) 6 years in total to cash out 2nd and 3rd pillar. ![]()

1 Like

I’m not saying it’s a bad thing to pay into five different 3a accounts monthly. I’m just saying you could simply switch your deposits to a different account every few years and the outcome would be the same.

1 Like

I mentioned 5 because normally people need to cash out full 2a in one year. So 5 accounts were recommended in various forums.

In the end , the final optimisation depends on one’s individual situation, needs for money at time of retirement etc.

With easy and cheap process to open accounts, one can have 30 accounts as well with every new year a new account ![]()

But as you said 3a is smaller already compared to 2a. And then if you already split it in 4-5 accounts then it’s even further reduced in size. It’s not something to worry about too much.

That’s highly dependent on your salary and pension fund.

Let’s look at a realistic example:

Time horizon: 35 years

Annual payments 3a: 7’000

Annual payments 2a: 20’000 (that’s already a high amount and I’d say most people have way less on average)

Annual interest 3a: 5% (fully invested)

Annual interest 2a: 1.5% (above min, many people only get the minimum)

Final value after 35 years:

3a: ~632k

2a: ~912k

While the 2a amount is higher, the 3a amount is still significantly high to optimize.

4 Likes

I don’t know if I am the only one who finds this worrying, though. I like to think nothing is free when it comes to services, having been burnt badly by “free” advice (3A with insurance…). There must be some cost, somewhere, or a limit. As it stands one could rebalance in Finpension 52 times per year…isn’t this a bit weird to be free IF we assume that the securities we hold there are in fact in our names? Or are they in silico and are/will be settled once someone withdraws - and I said above I expect most people to be far from it wth Finpension given they are quite new.

Looks like there is some confusion. First of all, assets held in a 3A account are NEVER held in your name. They are held in the name of the foundation, which is a separate legal entity than the operating entity. Meaning that even if FP go bust, the foundation was not affected and your assets are hence secure.

With regard to trading. FinPension incurs a ticket fee whenever they place orders with the fund banks. These ticket fees are highly likely flat and they don’t care whether they now purchase 10 or 1’000 fund units. So FP doesn’t incur any variable cost as such when you trade. The Index Fund itself trades like a fund does (aka trading cost are materially different from anything you and me have ever seen before). They recover these trading cost with the purchase/redemption uplifts applied at a fund level (that you still pay).

FP tries to reduce purchase/redemption uplifts using netting and pooling. This is actually good for the IndexFund too, as it leads to reduced trading (or at least the magnitude thereof) so its a win-win.

In conclusion: Your trade does not lead to any variable cost neither to FP nor the Fund, other than trading fees you still pay with the purchase/redemption uplift that are netted away to a certain extent. Why should FP charge you any transaction fees? They cover their fixed cost with your recurring fees already.

5 Likes

I was just trying to find a reason, why it might be complicated.

But the other thing you mention: You mean, when you have to adjust the value in the foreign currency until you hit the right value in CHF?

It’s not free. But it’s optimised

-

People can change strategy 52 times a year but they don’t change it because most people invest and hold.

-

Remember there is also lot of AUM under 1E plans and Vested benefits account. So most likely when a trade is placed at fund level there are many trades which get combined.

-

You are also paying 0.39% annually. So I believe overall it works out well for FP.

@TeaGhost has explained the mechanism in detail.

- of course, 52 times/year is an absurd exaggeration, but it is possible. It’d cost money to do that with other brokers, even with golden goose IBKR.

- true, it’s this point which I find somewhat worrying though, the worry that it’d be a mess to untangle, but that’s just me being overly conservative. I am not a fan of fractional shares either

- that’s fine, I hope it goes well for them because it works for me too

1 Like

I mean that the withholding tax reimbursement statements can’t be imported into Portfolio Performance, because the FX rate is missing on the statement.

1 Like

It’s a bit long story, but it’s also not free because there is a spread “fee” added upon subscription and redemption of fund units.

I have analyzed the price at which funds are traded inside finpension. They are not traded at NAV but at NAV plus OR minus the spread. Sometimes I had the same fund bought and sold in different portfolios, the price was the same.

My conclusion was that finpension books transactions at the price that they paid to the fund management for subscribing or redempting. Because of the netting, only a part of gross order is actually traded with the management and incurs “fees”. The rest of the spread fee is exchanged between users buying or selling the fund units. If you are at the same side of the trade as finpension, you pay your part of the fee, if you are on the opposite side, you receive some of that fee.

To their honor, it looks like finpension is not taking their cut when their users are trading funds.

10 Likes

Absolutely insightful comment. Thanks for further clarification

I don’t understand. I tried the upload function in Portfolio performance with the report from IB, but it didn’t work.

So what document do you exactly download every month on viac? Then you upload it in portfolio performance and it will automatically fill all the information so that you exactly see the performance from viac in that specific month?

What do you want IB or VIAC?

I detailed how to setup and update VIAC with Portfolio Performance in my blog → Portfolio Performance - VIAC Setup

And for IB as well → Portfolio Performance - Interactive Brokers

Wow thanks a lot, I will try this out

Hope that never happens “active funds out of business “ …

But great to see competitors

1 Like

@Burningstone

So I followed your instructions for importing from VIAC to Portfolio Performance.

I compared the amounts, do you happen to know why the Saldo in VIAC isn’t the same amount as the one in depot in Portfolio Performance? Isn’t it supposed to be the same amount?

Do you happen to have the identical amounts in VIAC and Portfolio Perfomance?

First of all, great that you got it going with my guide ![]()

For me the amounts match almost down to the Rappen, once a year I do a reconciliation and need to adjust 1-2 Rappen manually (not needed, but I’m a perfectionist xD).

There could be a few reasons why it doesn’t match on your side:

- The cash in Portfolio Performance is missing in your screenshot

- The prices in VIAC could be from a different date than in Portfolio Performance. I’d suggest to check for each security whether the number of shares match. If they do, you should be fine.

- VIAC uses way more digits after the comma in their internal systems than shown on the transaction statements, this can lead to small rounding differences.

- If the cash doesn’t match, you probably forgot to manually book the reclaims of withholding taxes (around mid april normally) in Portfolio Performance, unfortunately these can’t be imported automatically as VIAC doesn’t provide the exchange rate on their statements. It’s a pain in the a**, but at least only once a year. It took me about an hour for all 4 portfolios.

1 Like

@Burningstone

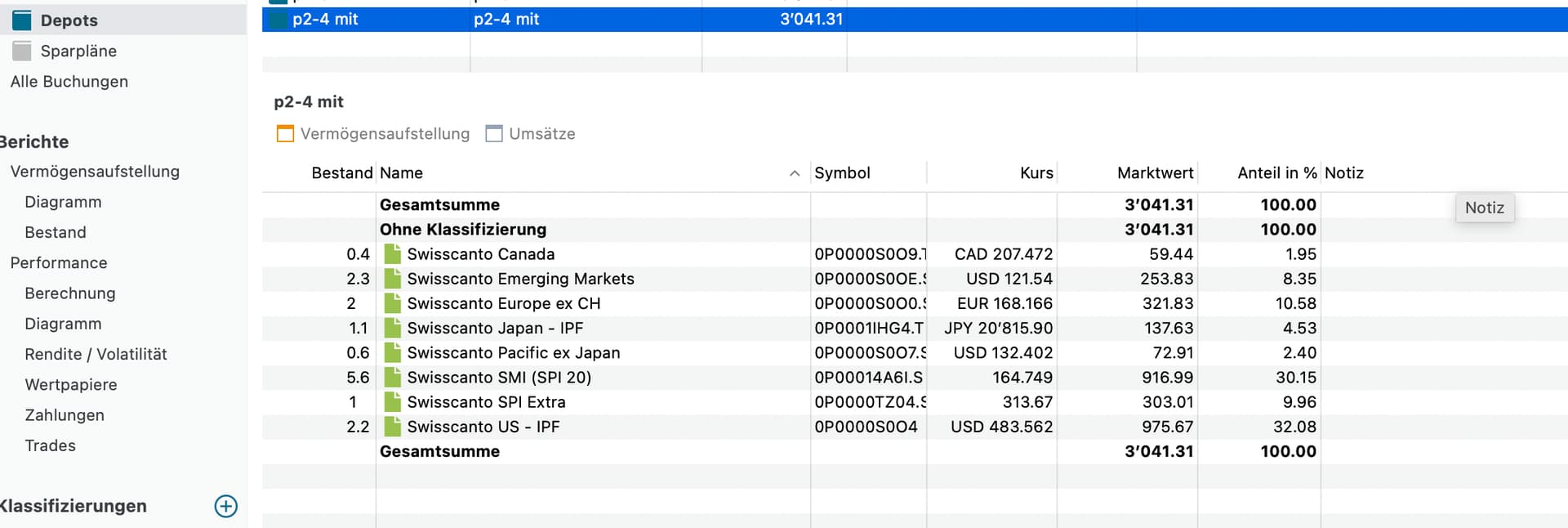

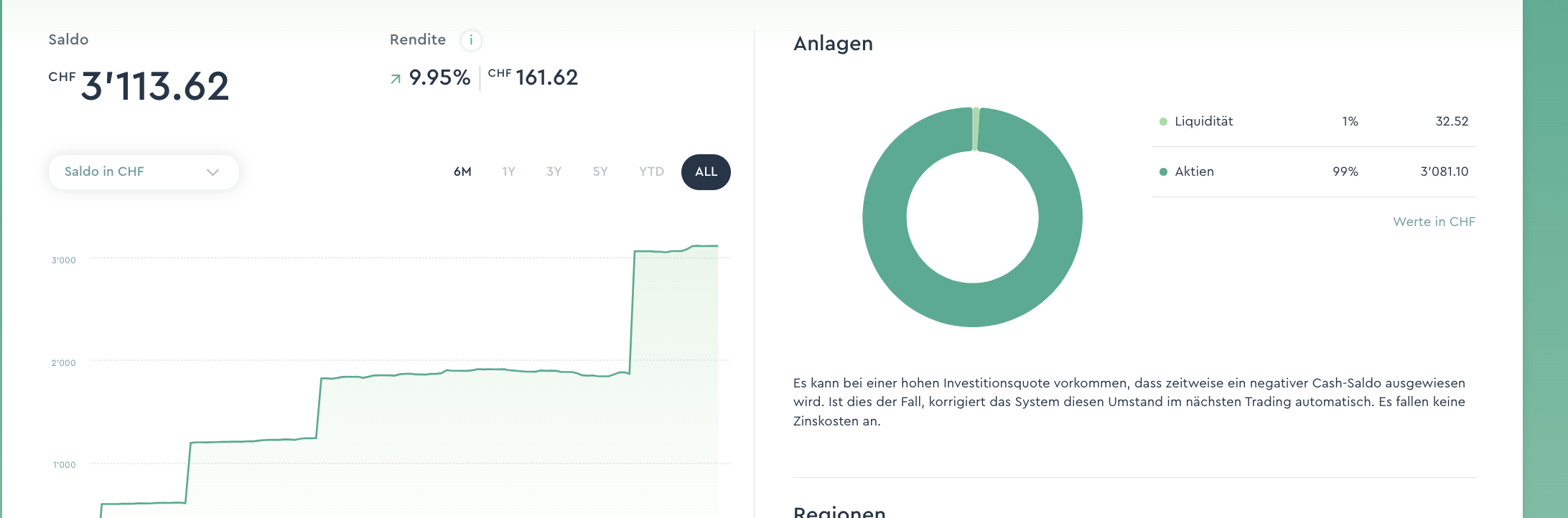

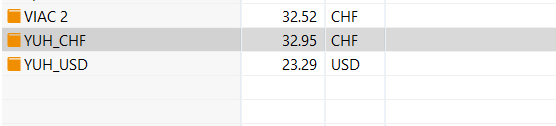

So the cash is correct:

The amount 32.52 CHF is the same the on in the screenshot in VIAC.

I also compared the amount of the securities. It is the same amount, and as you said correctly, VIAC uses much more digits after comma.

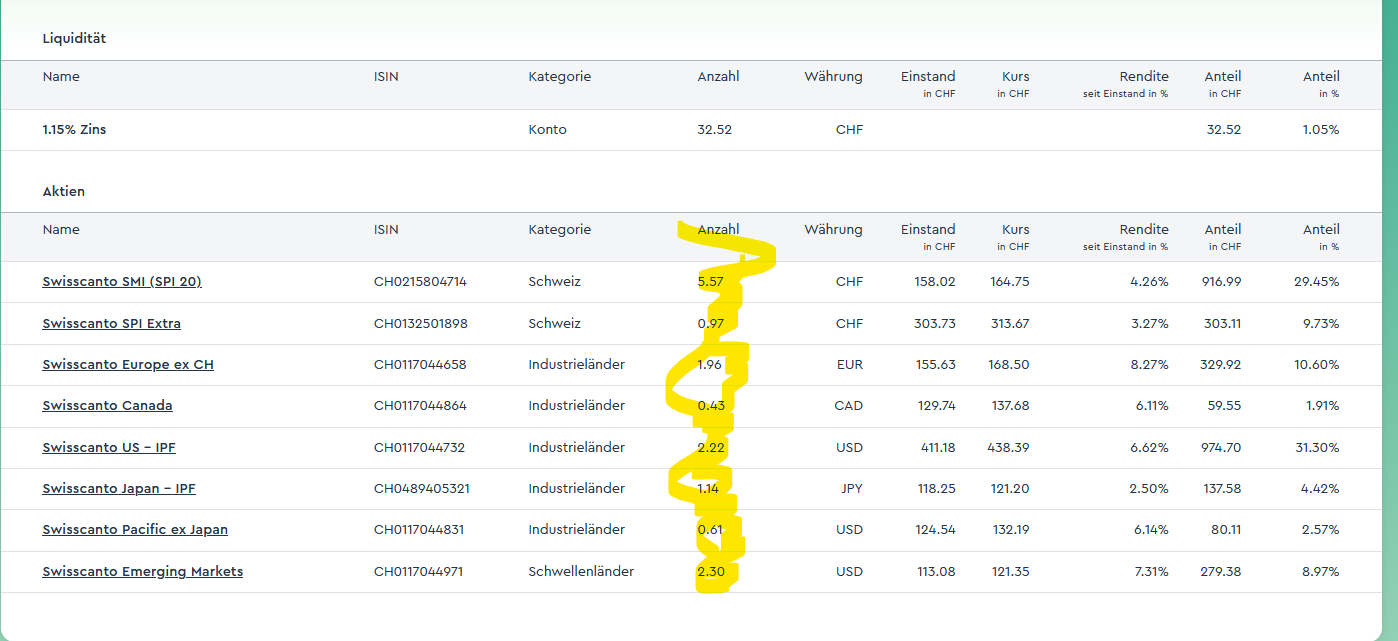

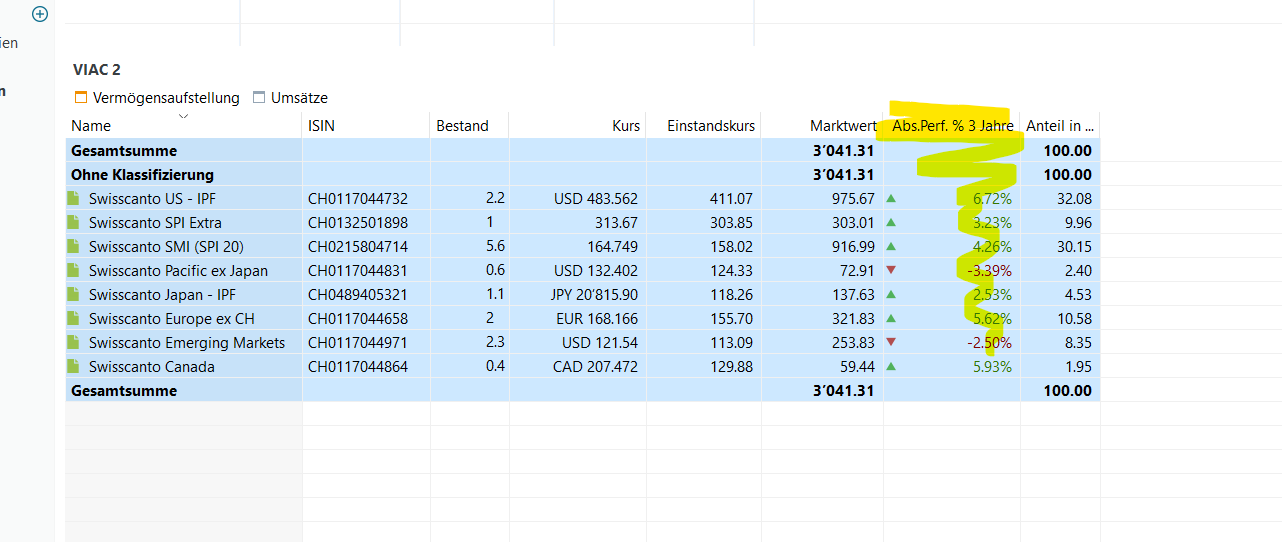

So the Depotvolumen in Portfolio Performance is Marktwert. Now i am trying to find out, how viac calclates to get the Saldo 3113.62CHF.

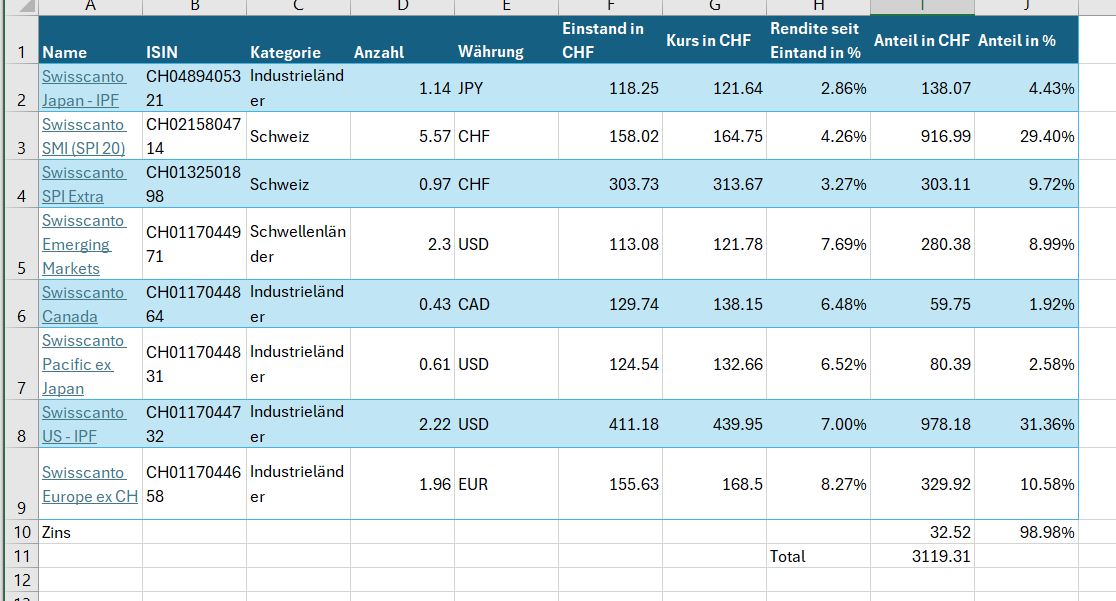

So I copied the data from viac to excel for better analysis.

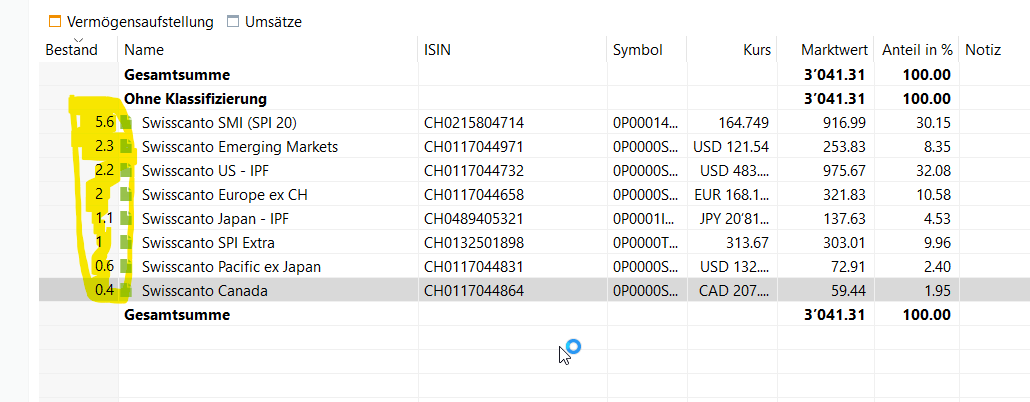

So Einstandkurs in Portfolio Perfomance = Einstand in CHF from Viac see Screenshot below

Anteil in %: When I add the Anteil together in VIAC / Excel it is 98.98%

In Portfolio Perfomance it is 100%. Dop you know why?

I tried to add the colum Anteil in CHF from viac, and the result is 3119.31. How does viac caculcate to get 3113.62CHF? Is it even possible to have the identical amount in porftolio perofmanc and viac?

Portfolio perfomance = 3104.31CHF

And VIAC 3113.62

Do you happen to know how I can get the same amount of rendite seit einstand in chf from viac in portfolio perfomance?

There is a column abs perf. % 3 Jahre… i didn’t find anouther one that displays the same amount as in viac rendite.

Thank you very much for your help!

That’s absolutely correct. But the spread fees are taken by the fund manager. For example, the often discussed “CS Quality fund” takes a subscription spread of 0.09%, and a redemption spread of 0.04% (see their prospectus).

So when you trade with Finpension on Tuesdays, you will get the Fund’s NAV of Wednesday ± those spreads.

Now, I don’t know if Finpension will net out redemptions/subscriptions internally to avoid these costs, but I don’t think so. I have always noticed these spreads.