Thanks, I’d seen that previously but wasn’t making sense of the numbers given the MSCI doc. And frankly still don’t make sense of it but it’s fine, it’s been a tough month at work with several late nights.

Those who put 99% World Quality: how is the performance until now? Any numbers? I am thinking if I should open another viac account global 100 or finpension with 99% Quality. I hope you guys can help me decide

While I would let others comment on actual realized gains, I am sharing a report which might be useful to understand how Quality factor has performed over the period 1999-2023

Important - this is history, doesn’t always mean future will be same / similar.

I think it’s important for investors to understand factor investing (quality is one of the factors). Factors should be used to tilt your portfolio to generate higher than market returns, but I think people tend to just invest in one of the factors seeking higher returns just because history said so. This is not always the best strategy. One needs to understand the underlying dynamics of each factor, set right expectations and then construct a portfolio.

3 Likes

That’s me since starting late last year

My main portfolio of SSAC, CSSPX and VWRL have all done better, but let’s see long-term.

Past performance is not indicative for future results.

Nevertheless here’s my gains since I started mid last year:

1 Like

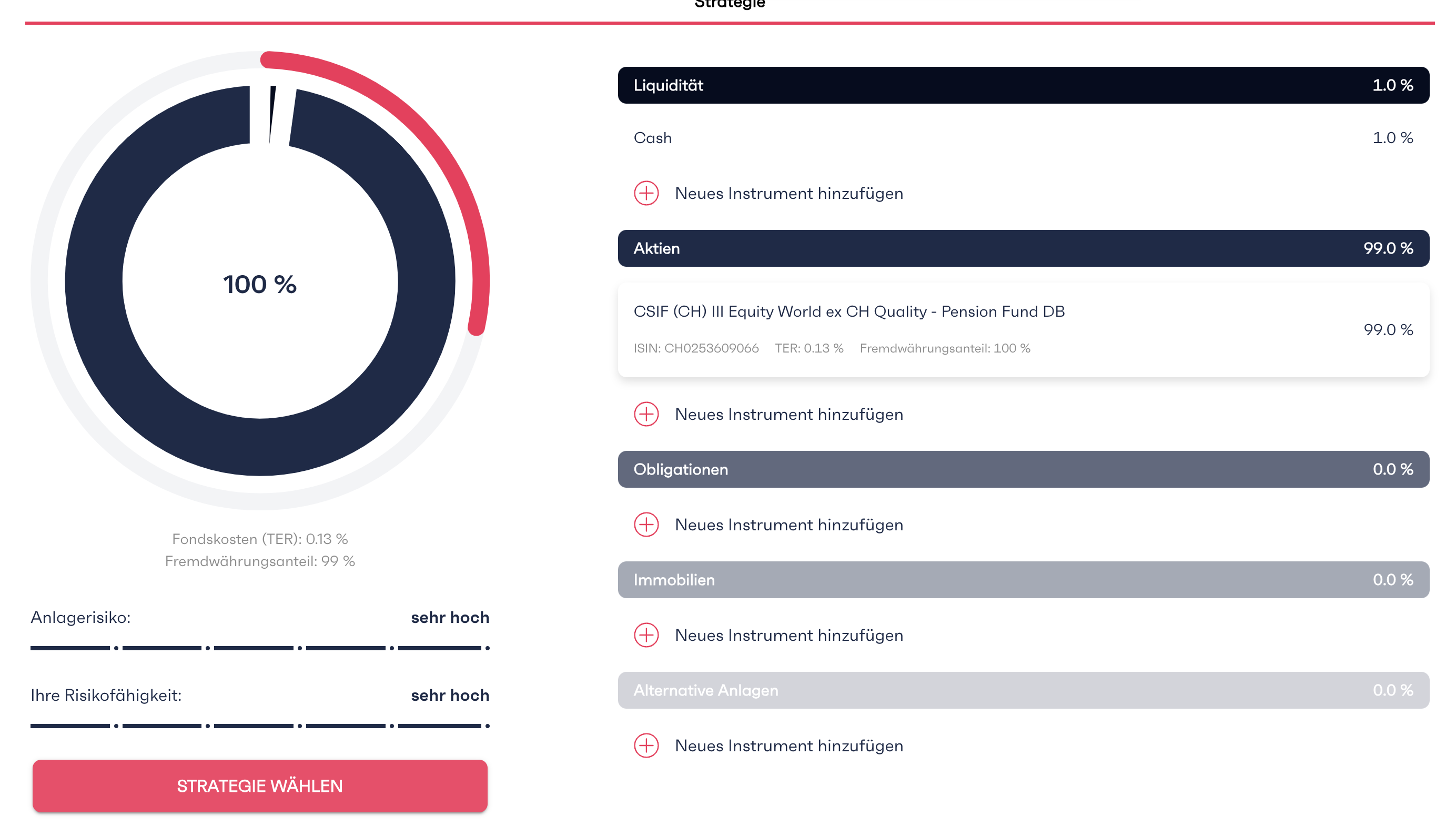

But that’s not 99% CSIF III Equity World ex CH Quality - Pension Fund DB

Because that one massively outperformed VWRL CHF for the period you show.

You’re right actually, I’d made an approximation of VT, I think I joined the Quality Qrew on February.

Just get it from the CS fundgate → location change | Credit Suisse Asset Management

1 Like

Maybe about my situation:

I have 2 Viac Accounts, 1 Frankly.

Viac 1: About 35k, Global 80, performance 18%, so far very satisfied

Viac 2: About 3k, Global 100, performance 9%, decent for the fact, that I just started in Januar 24.

Frankly: 96CHF, change to extreme 95 several months ago, hope to get to 100CHF and then transfer the money to VIAC.

I will open a 3rd pillar: finpension CSIF (CH) III Equity World ex CH Quality - Pension Fund DB

Is it recommend that i transfer all my 3rd pillar to finpension, so that I will have 4-5 3rd Pillars at finpension, and all of them are CSIF (CH) III Equity World ex CH Quality - Pension Fund DB?

What do you guys think? @assemblyrequired @Mirager @Abs_max

I’m guessing you meant to say 96k, not 96?

Yes, create a portfolio for each account you want to transfer. Don’t transfer the various accounts to 1 portfolio, as you can’t split them up again. Having 5 separate accounts/portfolios is advantageous from a tax perspective when you withdraw the money when retiring.

It’s not a problem to have multiple portfolios all with the same strategy. I have the same, one has only about 3k in it.

1 Like

You should not look at recent performance to make any judgments about investment decisions.

Else you should go 100% Nvidia or similar.

Past performance falls victim to recency bias. You need to understand why you do an investment and what are the expected returns of that. But those cant be judged by recent/past performance.

3 Likes

No it is really only 96CHF, just for the Test ^^"

So you have 99% CSIF (CH) III Equity World ex CH Quality - Pension Fund DB and 1% Cash, is this correct? Just wanna make sure that I don’t forget anything

1 Like

If I were you, I will not worry much and also do not overthink. You can have 2 accounts at Finpension, 2 at Viac and one in Frankly. Total 5.

In other words - I wouldn’t recommend to close or transfer anything. I know finpension might be cheapest. But difference between 0.39% and 0.44% is not that huge in my opinion. For perspective if you have 100,000 CHF in the portfolio, 0.05% would mean 50 CHF on annual basis.

If for some reason you don’t like Frankly (for example because of lack of choice of funds), then you can have 2 accounts at VIAC and 3 accounts at Finpension.

Going forward over a 10 year period, try to have similar amount in all of them. This way you would be able to have some flexibility at time of retirement.

Regarding which strategy to choose within each of the accounts, it’s more of a financial decision based on risk tolerance and overall portfolio allocation strategy (total across -: 3a, bank accounts and also other brokerages)

Last point -: I think you are focussing a lot on past returns. It is not going to be a good criteria for future returns. The future returns are based on when you invest and what strategy you choose.

And believe me -: few years back, Viac was cheapest, then Frankly arrived, then Finpension, in coming years there would be more. So any decision you make today will only be valid for few years ![]()

3 Likes

Yes, that’s correct.

Transactions are free with finpension, so you can always adjust your portfolio.

Common wisdom is to stop depositing into an account as soon as it reaches 50k and open another 3a account, but as stocks will increase the money in an account over time, I would distribute deposits much earlier, say after an account reaches 10-15k. Some deposit CHF 117.60 (7056/12/5) into five accounts each month, although I think that’s overkill. Each year into a different account/portfolio is fine IMO.

May I ask why you would consider that to be an overkill? After once setting up the 5 automated payments from your bank account to Finpension you don’t have to think about it anymore, no? Of course changing the amount if the limit has changed for the next year might be considered more work, but that’s it.

1 Like

If your tracking with Portfolio Performance, you have upload a lot of PDFs ![]()

1 Like

I do that, what’s the issue? You can upload all PDFs for one portfolio at once, so 5 uploads a month.

The painful part is once a year to manually enter all the reimbursements of withholding taxes, because VIAC doesn’t provide the FX rate in these statements ![]()

Having similar amounts in 5 3rd pillar accounts at retirement age is not really desirable unless you plan to take the annuity from your 2nd pillar after retiring.

If you intend to cash out your second pillar and do so over 2 years (obligatory and extra-obligatory in different years), the optimal scenario may be to split 3rd pillar cash out over 3 4 other years. Hard to do so in equal-ish amounts with 5 similar 3A accounts.

Anyways, I’m not sure optimizations at this level really matter that much: 3A is usually small compared to 2A, amounts can be cashed out at different times for real estate or self-employment for example, rules may also change in the meantime…

The main point for me is that IMHO there’s no need to over-complicate things, especially if the result is not even an optimal one.

edit: thanks @Luk_nuts for pointing out the mistake!

3 Likes

Plus 1 vs 5 documents for tax filing.