To be honest, I also always thought that one should mimic VT in finpension and that’s it.

But I think, their default Global strategies are based on strategic asset allocation and they overweight Switzerland intentionally to create home bias. I have seen such behaviour in almost all pension funds and maybe all funds in CH in general.

Having home bias might look like lack of diversification but I also think there is a reason why so many investors in so many countries have home bias. Investing is not only about returns but also about risk, investor protection, familiarity, tax treatment etc.

I know most people tend to not like traditional fund managers or houses because of their higher costs. But they do a lot of research and have high level understanding of asset strategies. Maybe worth considering default strategies at FP since it is a retirement account.

Home bias has many scientific reasons behind why it‘s a good idead. Most research comes to the conclusion of around 30% being optimal.

Couple of those reasons:

behavioral factors do play a huge part, for example when your home market does well, you want to be in it. If it is bad, at least you‘re in same boat as your environment.

taxes are a big one! With home bias you most of the time have tax benefits. For example for most of the world there are unrecoverable witholding taxes on dividends (US stocks and Japanese stocks for retirement funds being an exemption in the case of finpension). Those are zero for swiss stocks. You for example lose 10-15% of your dividends from emerging markets. There‘s also the "giving back of capital reserves“ that swiss funds do tax free (not that applicable in the case of 3a)

local inflation, currency and meeting consumption targets in retirement. Your local companies are likely to be more closely related here.

protection. What happens in case of crisis in other markets? For example what happened with russian stocks, cant happen to your homes bias. Of course super small risk, nontheless it‘s there.

Very true. As we discussed on Indian funds topic… Indian investors or even Non Resident indians have significant tax advantages over foreign investors. This aspect is often overlooked.

Conversely, you’re investing where you’re making a living. So when disaster strikes, say UBS goes belly up or an earthquake devastates Basel, you may not only suffer a loss in your investment portfolio - but also lose your job and regular income.

Should is a strong word! If it fits your strategy is “as broad as possible” and “as passive as possible” then simulating VT in Finpension could make sense. However the third leg of that strategy is usually “for as cheap as possible”, in which case you can already get VT in many other places for a lot less costs.

Personally I went with Finpension (and not VIAC) after a lot of consideration, after losing 40% to insurance 3A, and decided that given the capped annual contribution allowance AND locking of the money for a long time AND higher costs compared with investing in any retail broker AND the fact they are the only ones who offer tracking of the Quality index to go 100% Quality.

Has anybody also received dividends last weeks? I have a VT-like strategy with e.g. “CSIF III Equity World ex CH Blue - Pension Fund Plus ZB”. I thought (and the factsheet says that) the funds are accumulating.

I am wondering, there was a dividend payment on the 14th Apr, but hasn’t been allocated to equity (have 99% equities, now it’s been skewed a little bit towards cash), given I am only with Finpension since January I don’t have much experience, but would have imagined the dividends would have been allocated to equities on the weekly rebalancing.

Another note, paging the Quality Qrew, I have ~15000 in Finpension in the Quality fund, the dividend was 78CHF meaning the (internal) yield is ~2%, right?

The rebalancing takes place if the current allocation deviates from the target one by at least 1%. Not sure how they round things up. Pretty difficult to reach even +0.5% of cash above the target with just one distribution.

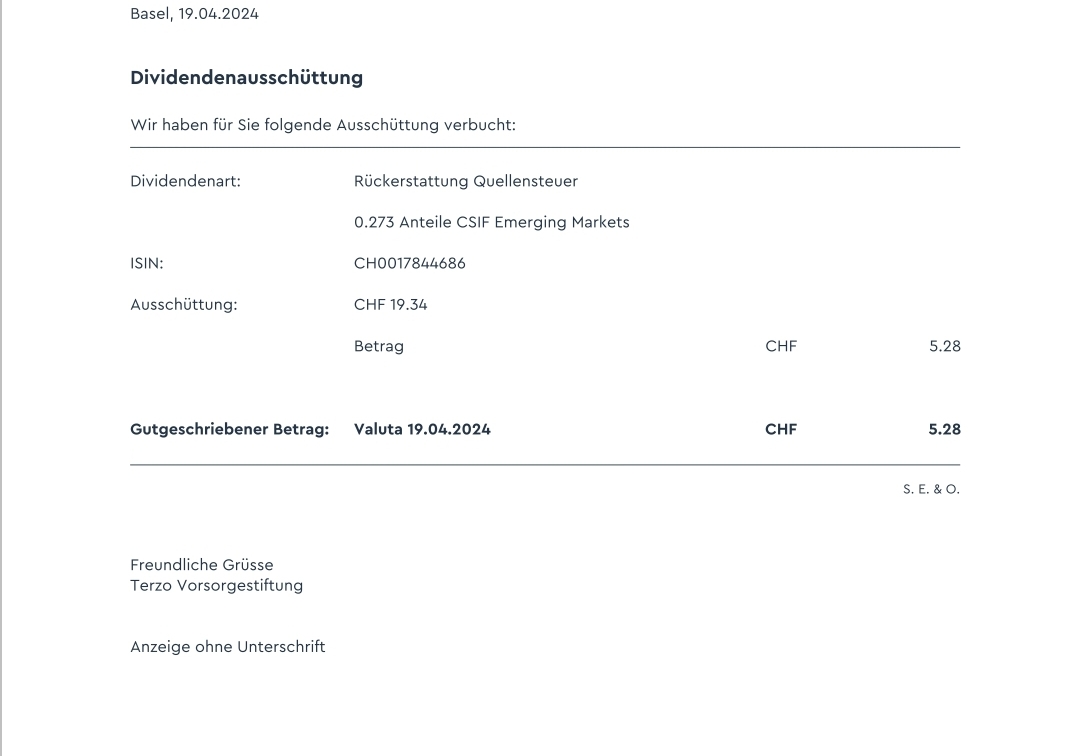

These are reimbursements of Swiss withholding tax on dividends, 35%. So I came to 1.63% original dividend yield, which is low . No idea which units are eligible to receiving this refund, there might be some cut-off date or something.

„Since 2019, Credit Suisse Index Funds (CSIF) have been accumulating. This means that interest and dividends are generally retained in the fund and reinvested.

And yet there is a distribution, which we have credited to you as follows: …“

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.