I need your help in understanding how my 3rd pillar works.

As a newby I’ve already signed it and have been paying the maximum for 2 years, before realizing I don’t fully understand how it works.

I guess it’s never to late to start going in the right direction…

In any case, here is the question:

Currently I pay a premium with Swisslife of 3283 CHF / year since 2019, if I do the calculation over the 35 years I should have a total of: 114’905 CHF, in contract I signed it is written guaranteed savings 94’226 CHF, a difference of 20’679 CHF.

Thanks for all your replies, the good thing (I guess) is that I started just 2 year ago) so the losses won’t be too bad…

If I understand correctly the smarter move to do now is to resign my contracts and move to VIAC.

Apparently once I sign up to VIAC they’ll take care of everything, I just have to embrace the losses. Am I right?

Hi @Tmask welcome to the club! I was in the same situation as you last year, except at Axa. I switched everything to VIAC and never looked back, and couldnt be happier. Apparently there might now be “better” offerings than VIAC (search in this forum).

However from my experience opening the account with VIAC was very easy, and once you have your account you can select “transfer from another 3a pilar account” , you fill out the form, send it, just wait a couple weeks, and it is done. Plus the VIAC team are very helpful and responsive

Let me know if you need any help or have questions

Thanks for your feedback.

I have two 3a pillars, half of the maximum amount at Axa and the other half at Swisslife.

May I ask you how much you have lost?

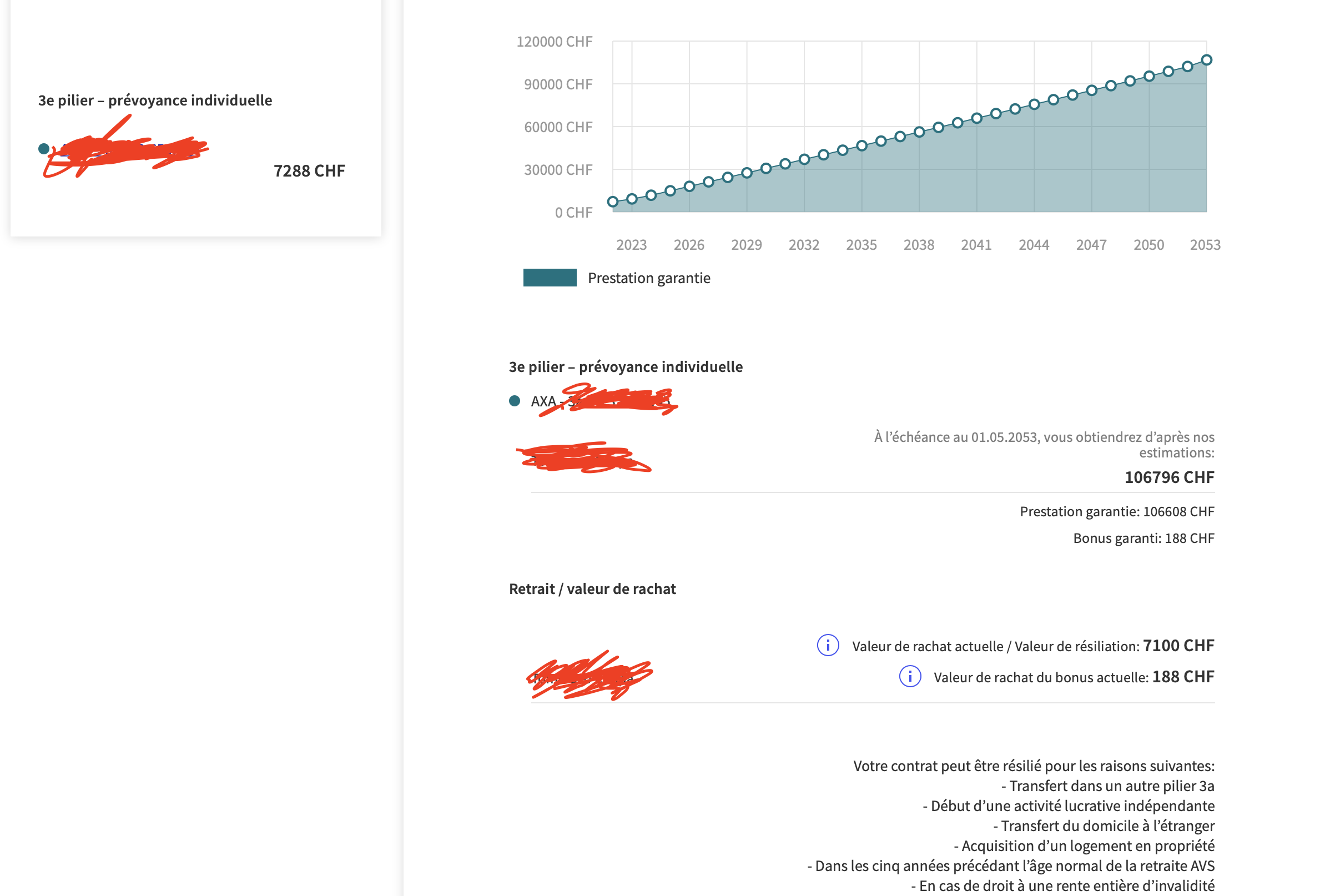

I currently have 7 288 CHF at AXA and 6800 at Swisslife.

Should I imagine that I would loose half of that?

What would you suggest that is better then VIAC?

Thanks

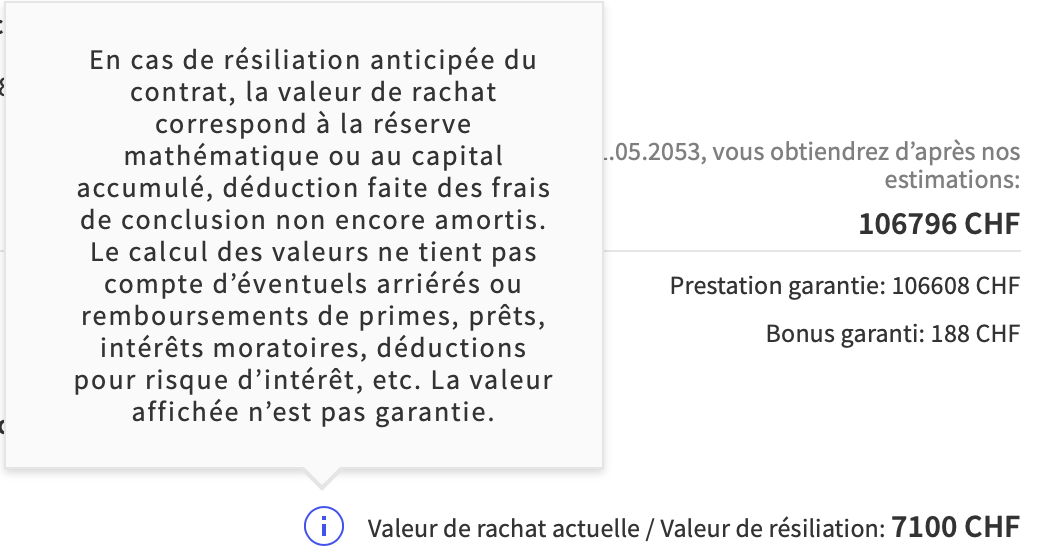

You can check your contract details for buyback amounts. It might be possible that you don’t get any money back, depending on the contract. I still remember a proposal from Generali where you didn’t get any money back before year 4 was over and paid. First 3.5 years was provisions only.

You can check for finpension. There’s another thread in this forum.

Interesting, this is what is sais on the contrat for AXA: 1. Assurances susceptibles de rachat Toutes les assurances sont en principe susceptiblesde rachat, à l’exception des assurances suivantes:

– assurances en cas d’incapacité de gain,*

– assurances au décès et*

– rentes temporaires au décès avant le décès de la personne assurée.Un rachat est toujours possible pour les assurances constitutives d’un capital, si les primes ont été payées pour au moins 3 années. Lorsque les primes ont été payées pour moins de 3 années, un rachat est possible si la valeur de rachat calculée selon le chiffre 7.4 est positive. Quand une assurance de risque est susceptible de rachat, un rachat est possible si la valeur de rachat calculée selon le chiffre 7.4 est posi- tive. Les assurances financées par une prime unique peuvent être rachetées immédiatement. L’une des conditions de résiliation mentionnées aux chiffres 6 ou 9 doit en outre être remplie*

So if I understand correctly I should be able to re-buy given that it has been 3 years.

Still not sure how I calculate the amount.

If you want to be 100% invested, finpension is a bit better (unlimited non-CHF investments, no currency exchange cost, slightly lower management fees).

As I see it, the main advantage of Viac is that you can keep e.g. 20% in cash where you still earn a bit of interest (0.1%) and you don’t pay any management fee on that part.

At finpension you’re forced to invest into bonds if you want to reduce the risk/volatility of your portfolio (compared to 100% stocks/real estate). CHF and CHF-hedged bonds are currently considered worse than cash with 0.1% interest.

Another advantage of Viac is that a ‘free’ life or invalidity insurance is included, however, this is likely not that significant.

I would definitely recommend that you check your terms of insurance to see in which year you can claim back at least some of your money. Many permanent life insurances begin to have a reclaimable cash value from year 3. If you can reclaim more money from the cash value than you would pay in total premiums until you are able to cash out, then it’s generally worth waiting.

You should generally assume that you will lose at least half. Cash value (including returns on investments) generally doesn’t begin to match total premiums paid until year 10-20 at least.

Of course there is also the option of keeping them until the cash value at least breaks even. If you would lose say, 7000+ francs by terminating them early, that may equal or surpass the opportunity cost compared to Viac, etc. over the investment term. You have to do the math based on how long you expect to invest the returns your life insurance investments have delivered so far in relation to the stock market.

7.4 Valeur de rachatLa valeur de rachat est égale à la réserve mathéma- tique diminuée d’un montant égal à 5% de la valeur actuelle des primes non encore échues. Pour une assurance à terme fixe libérée du paiement des primes suite au décès de la personne assurée, la va- leur de rachat est égale au montant du capital assuré escompté du taux d’intérêt technique. Pour une rente temporaire au décès, la valeur de rachat après le décès de la personne assurée est égale à la somme de toutes les futures rentes temporaires escomptée du taux d’intérêt technique.Selon l’évolution des taux, une déduction pour risque d’intérêt peut avoir lieu lors d’un rachat. Les cinq pre- miers points de pourcentage de la déduction de la valeur de rachat sont dans tous les cas supportés par AXA Vie SA. Aucune déduction pour risque d’intérêt n’a lieu au cours des cinq dernières années contrac- tuelles.Une éventuelle déduction pour risque d’intérêt est cal- culée sur la base de la durée résiduelle déterminante au moment du rachat multipliée par la différence entre le taux d’intérêt moyen et le taux de swap à sept ans en cas de rachat. La durée résiduelle déterminante de l’assurance est limitée à la moitié de la durée contrac- tuelle totale.

Le taux d’intérêt moyen correspond, durant la pre- mière moitié de la durée contractuelle, à la valeur moyenne du taux de swap à sept ans depuis le début du contrat. Durant la deuxième moitié de la durée contractuelle, le taux d’intérêt moyen correspond à la valeur moyenne du taux de swap à sept ans sur les n dernières années précédant le rachat, n étant égal à la moitié de la durée contractuelle totale.

La valeur de rachat correspond à au moins deux tiers de la réserve mathématique, pour autant que les primes ont été payées pour au moins trois années, plus la valeur de rachat du bonus accumulé jusqu’à cette date.

Hello Daniel,

Well for me the idea is to invest for the long term,

I’m 33 and I have at least 30 years of investing before I retire.

That said, given the really bad returns I get from AXA ans Swisslife I guess I would recover quickly from the loss.

Honestly I don’t know how I signed for something like this…

I think everyone who has permanent life insurance eventually ends up wondering how they allowed themselves to be conned into it. If you’re planning long-term, I’d say take the loss and quit. But do check what the difference in cash value will be if you wait a year or so to cash out. For example, if you would get nothing back now, but would get 4k back next year after paying the last 3k premium, that 1000-franc difference would make it worth the wait and cost.

Get out as soon as possible of this scam and forget it forever. It will be the only mistake you made and you will recover your loss in the following year with a better product

So, for Swisslife seems more complex.

I’ve managed to find the full contract → WeTransfer - Send Large Files & Share Photos Online - Up to 2GB Free

I currently have 6’347.70 CHF with them.

I really don’t understand how I can calculate the loss for resigning.

Eternal gratitude for whoever can help me out

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.