Just curious how the second pillar works out, my new employer says I must contribute 8% and they will match the same 8%.

Do I have any choice in this?

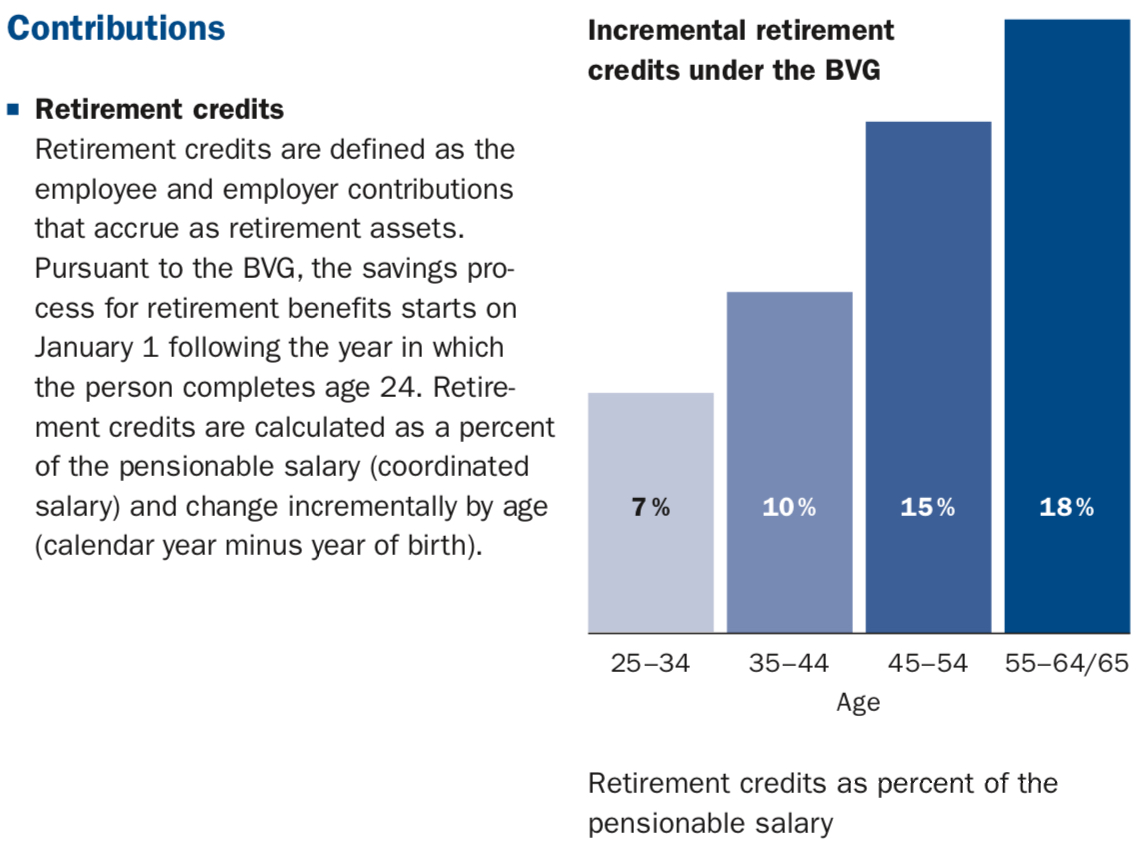

Are there laws saying how much one must contribute based on age?

Is my 8% calculated out of 100% of my monthly gross?

Any advice is appreciated.

You must ask your company’s institution rules. There is a compulsory part (legal minimum contribution and legal minimum benefits) and sometimes an over-compulsory part (extra contribution and extra benefits, but benefits compared to cost are usually lower here). You never have anything to decide before you retire.

When switching jobs/pension funds, he could try to not have his benefits transferred to his new pension fund scheme but try to keep it in a vested benefits solution (though this would only make sense when investing said benefits in equity/REIT etc., as the interest rates/return on vanilla vested benefits accounts is much lower than in pension funds)

Are you referring to a Swiss company operating a second pillar / Pensionskasse in Switzerland? What you are describing sounds more like a defined contribution plan like they have in the US (such as a 401k).

I’m talking about a swiss contract here, not US.

This is how they wrote it in the offer letter “subdivided employer’s contribution of 8% and employee’s contribution of 8%”, the pension leaflet is 48 pages and I can’t make sense of it all as it uses words and phrases I’m struggling to make sense of.

Bottom line is, any idea if I can adjust my personal contribution percent wise? Is that locked by Swiss law?

I think it’s decided by your employers (and its pension committee), from what I understand it can differ quite a bit between companies. The law only mandates that employers contributes at least half.

My bet is that you are dealing with Säule 2b, which is the überobligatorische Vorsorge. I.e., voluntary additional contribution, once you have maxed out the mandatory contribution, which tops out at a salary of 85´320.-. It seems they are matching up to 8% of your salary. I would grab that offer, given that a portion of those contributions can be withdrawn later to buy your residence (or start a business).

Biggest difference to 401k in the US is that your employer is forced to match the minimum requirement. I can set my contribution between 2.5-8%, my employer is at 6.5% no matter what I choose. So I’m at 2.5%.

Do assume that it is different with each company. For example in my company I could chose several plans of my contribution (5% - 13%) and the company matches those automatically between 9% - 15% (depending on your age).

And as well you could put more money into your 2nd pillow - so called buy-in. That was super interesting in the past, as in some cases the company did match your buy-in contribution as well. But I do assume that this is gone, unless for some high level contracts in management positions.

That’s correct. But keep in mind that it’s the total minimum, so both parties together. Your employer has to contribute at least 50% of it. Good pension funds contribute way more than they have to. Mine for example does (doesn’t matter how much I contribute):

@Cortana: Mind disclosing who your employer is?

This is a very good offer. Usually only the state and state-owned companies pay these luxury contributions. I have never seen such rates at a private company. Usually they just stick to the law, i.e. they pay exactly the 50% of the minimal amount.

The problem with 2nd pillar in CH is that you cannot choose your pension fund. You just have to take what your employer is offering. If you are lucky, your company have a strong union which fought for better rates.

But generally speaking of “good pension funds” is useless, since you probably won’t choose your employer by the pension fund. However this might become a valid point when switching jobs at a certain age - if you have a good pension fund, then you are deadlocked in your company at a certain age.

Also the minimums only matter up to 84k of salary. Which is I guess is how some employers manage to have overall contribution level below 18% regardless of age (if the salaries are higher than 84k).

It’s one of the majors banks here in Switzerland, I don’t want to be specific because I want to stay anonymous (I talked way to much on changing employers, hiding 2nd pillar money etc.).

I would definitely choose my employer by pension fund if I was close to retirement (>10 years). The last 10 years make up a huge amount in total contributions and there are differences in the conversion rate when you retire.

I think it should be a factor at all times. It’s not just about salary, work place and distance to home. If I would get a job offer with a better salary but their pension fund contributions would be half of what I get now, should I really consider working there? I would take it into account, make the calculations and then decide.

In order to get better 2nd pillar conditions/money when you are retired and let’s say my employer allows me to choose between option a) paying into the überobligatorische BV or option b) doubling the obligatorische BVG-Abzug from 10% (the standard minimum for age between 35-44) to 20%, which option would be financially better?

Now I know that with both options I can deduct obligatorische and überobligatorische from my income taxes so there is no taxes advantage but I see the difference with the Umwandlungssatz, for the obligatorische it is 6% and for the überobligatorische it is 4.4%… So logically I should go for option b) which pays more into the obligatorische, right?

But as I am no BVG expert I was wondering if I am missing something here… or what would you chose and why?

As I understand it, everything above the mandatory minimum is considered “überobligatorisch”. It doesn’t matter whether you have more than 10% monthly contributions (your option b), an insured salary above 61k (86k-25k) or do manual buy-ins. You get “überobligatorischer Umwandlungssatz” for all of these (or possibly “umhüllender Umwandlungssatz” as is becoming more common). I’m not completely sure, though, as I don’t have a pillar 2 to confirm.

If doubling to 20% means that the employer pays 10% and you pay 10%, that sounds like a better deal than a buy-in on your own, assuming this means you get 5% extra from the employer. This may depend on the details of these options, e.g., lack of flexibility may be a downside.

Please also note that the “Umwandlungssatz” that matters is the one of your final pension fund when you retire, which may not be the same as your current pension fund (and the conditions of the current fund may change as well). The mandatory minimum may also change over the years. I.e., there are various aspects that make it impossible to predict the exact impact of certain choices.

The most important aspects while still far from retirement are the maximum monthly contributions from the employer (part of your total compensation; besides the percentage also make sure the full salary is insured) and the maximum contributions of your own money (can be increased monthly contributions or buy-ins). The interest rates / returns can also make a significant difference but that may be difficult to predict and compare.

For your last employer / pension fund, the “Umwandlungssatz” will be significant but also options for (partial) lump sum withdrawal. Depending on the latter and your personal situation, the former may be less important. Especially if you aim for early retirement, the “Umwandlungssatz” may be irrelevant.

Thank you jay for your answer. So it looks like I was missing the point that the amount of money over the 61k of insured salary threshold is considered as überobligatorisch and therefore the lower umwandlungssatz will be applied anyway to that extra amount.

So re-formulating my two options more correctly based on your information would now would be option a) increasing the insured salary (versicherte Lohn) from 60k to 120k or option b) keeping the 60k insured salary but increasing the BVG-Abzug from 10% to 20%.

Something tells me that option a) sounds better because the insured salary value doubles but I can not objectively tell which one is better…

And yes in both cases the costs would be split 50/50 between employer and employee. I have already paid in all the possible buy-ins I could so that’s the reason why I am exploring other possibilities of getting better BVG conditions at retirement. Due to long studies I have only started to pay BVG at around 33 years old and since then there has always been the minimum salary (60k) insured with the minimum BVG-Abzug as defined by Swiss law. So a pretty much minimal BVG contract so to say…

For retirement purposes the two might be roughly the same, assuming the doubled retirement contribution rate will continue with 45 (i.e. 30% instead of 20% up to the age of 54 and then 36% instead of 18%)¹. If 120k is tied to your salary and thus the insured salary will increase further if/when you get raises, option (a) will be better in the future.

However, I expect the risk insurance part of the pension fund (disability and death) to only increase with option (a). This will likely also imply an increase in the monthly risk premium (typically covered half by the employer).

I’d recommend option (a), unless you’re sure you and your dependents don’t need the increased payout in case of disability or death (and the 120k is fixed, not tied to your salary).

As always, it may be necessary to read the fine print of your pension fund as there is a lot of flexibility beyond the mandatory BVG minimum.

¹ Edit: I forgot that the law imposes a maximum of 25% for total retirement contributions. I.e. as I understand it, it’s impossible to have double the mandatory retirement contributions from age 45 onwards. This means that option (a) will be significantly better in the long term.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.