Last year presented a real test of one’s chosen asset allocation. Looking back to see what you actually did during the the March-June 2020 period in particular is probably a much better way than a questionnaire to evaluate your actual risk tolerance.

I am curious how people reacted.

Let’s say your real risk tolerance is on a scale of 0-5… what did you do?

(edit: now in poll form…)

How did you react during the March-June 2020 period?

0: You had trouble sleeping and ended up completely losing your shit and selling it all.

1: You sold some of your equity holdings and held off buying for a few months.

2: You held off investing for a few months

3: You continued to make (monthly) purchases as before.

4: You bought more aggressively than before

5: You called literally every bank and person you knew to get them to lend you money to buy more stock.

0voters

I thought I was in the 3-4 range and it turns out my risk tolerance is a 4 on my made-up scale…

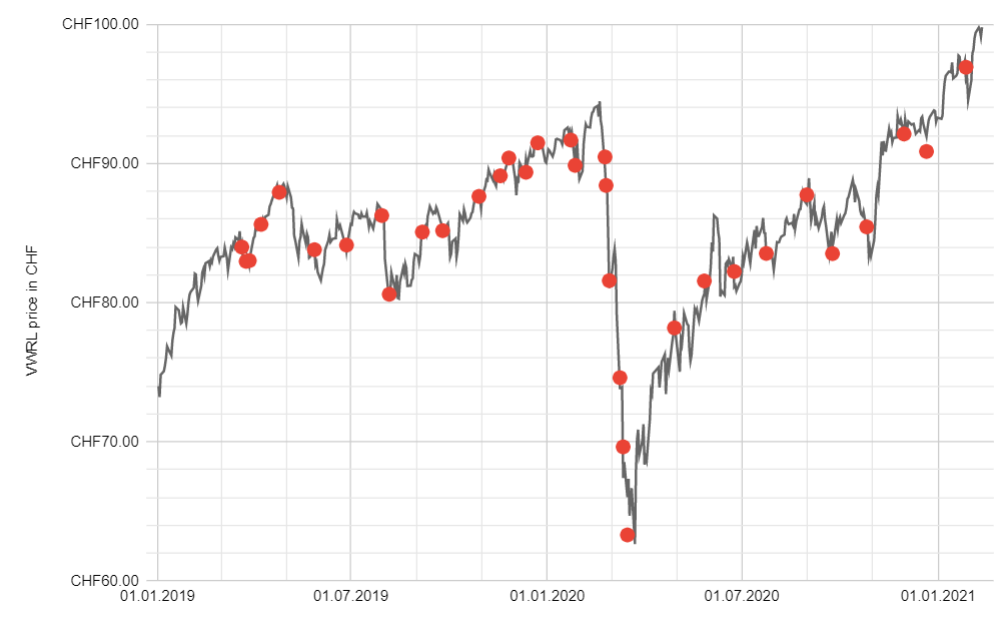

Red dots are purchase dates. Cash as part of my assets went from nearly 30% to 14% from March 1 to June 1. Turned out this was a good choice… but it is easy to forget the uncertainty at that time. Also, I am not sitting on millions and planning to retire in the next couple years… I would likely have acted very differently had that been the case.

Maybe it‘s also relevant why one acted in a certain way (closer to RE, far away from it). But then again one should have an investment policy and just follow it, no matter what. It‘s especially valuable in a „crash“

Done. was unaware of this functionality.

However, I think it is more interesting to hear about people’s pre-corona crisis self-evaluated risk tolerance vs. their actual risk tolerance.

I just kept buying as planned…I had troubles sleeping at times but it was more because of a deadly pandemic than because of the market crash…

If anything it confirmed that my risk tolerance to death is much lower than the one to market crashes

When it kicked off, I sold some individual shares that I dabbled with until then at the profit.

Then kept buying (a bit more intensely) ETFs on the way down and up (and a few corona-stock picks to play with).

Held off a bit recently, as I am filling in some other asset classes now up to my desired AA.

So I’d need a multicheck selection.

When the markets tanked last year I dissolved my TrueWealth portfolio almost at a loss (after 2 years of throwing money at it) and started investing in IBKR, tried to short the market after March 23rd… came to my fucking senses and only bought VT and ARKK from that point on (and some little Tesla gamble where I realized some 5k profit).

So I selected I started investing more aggressively…

Invested more aggressively during Feb-Mar but then shat my pants off once prices returned to all time high and let my USD money lose purchasing power during the last 6 months

I was supposed to receive some money towards the end of April and decided I wanted to invest it before actually receiving it. I ended up keeping some margin until now and probably will for the foreseeable future.

Your story is one of the reasons I am reluctant to cash out my shares even at the more extreme ATH prices today!

Most likely I am just going to slow down my DCA into more shares. Maybe commit 30% of my usual monthly investment and keep the other 70% in CHF until I have a bit more confidence in valuations.

I find it very hard to believe VT will not be lower in CHF terms again at some point over the next 5 years.

I’d prefer to look at it as “I am not interested in putting such a high % of my cash into the SHOPs at $180bn valuation with $2bn revenue and no profit”.

I don’t expect it to last 5 years and will have a significant amount of exposure (>80% anyway).

Are you really rushing to add your paycheck into the market each month at current valuations? Swiss property will return more free cash flow soon.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

was unaware of this functionality.

was unaware of this functionality.