Last year I had an interesting opportunity I was never looking for: To become a land lord.

As you probably know, the requirements for down payment are quite high. It’s not uncommon that younger people get financial support from their family.

So did I. Actually, I didn’t even ask for it but my father staged the deal. He knew of a house that was for sale and offered to give me an advance of my inheritance under the condition that I had to buy said house.

Meanwhile, most of the bills associated with the transaction are paid and I think it could be interesting to the community to have an example to see what can be expected. Only future can tell whether it is going to be a good deal.

Rule of thumb by ubs is that monthly rent 1225 should equal the value of the house to call it fair value. In your case is 22001225=660000 so it looks like you bought it decisively under market value (if the rent in the region for similar object are around 2200). Or that you are renting well over usual rent and find someone.

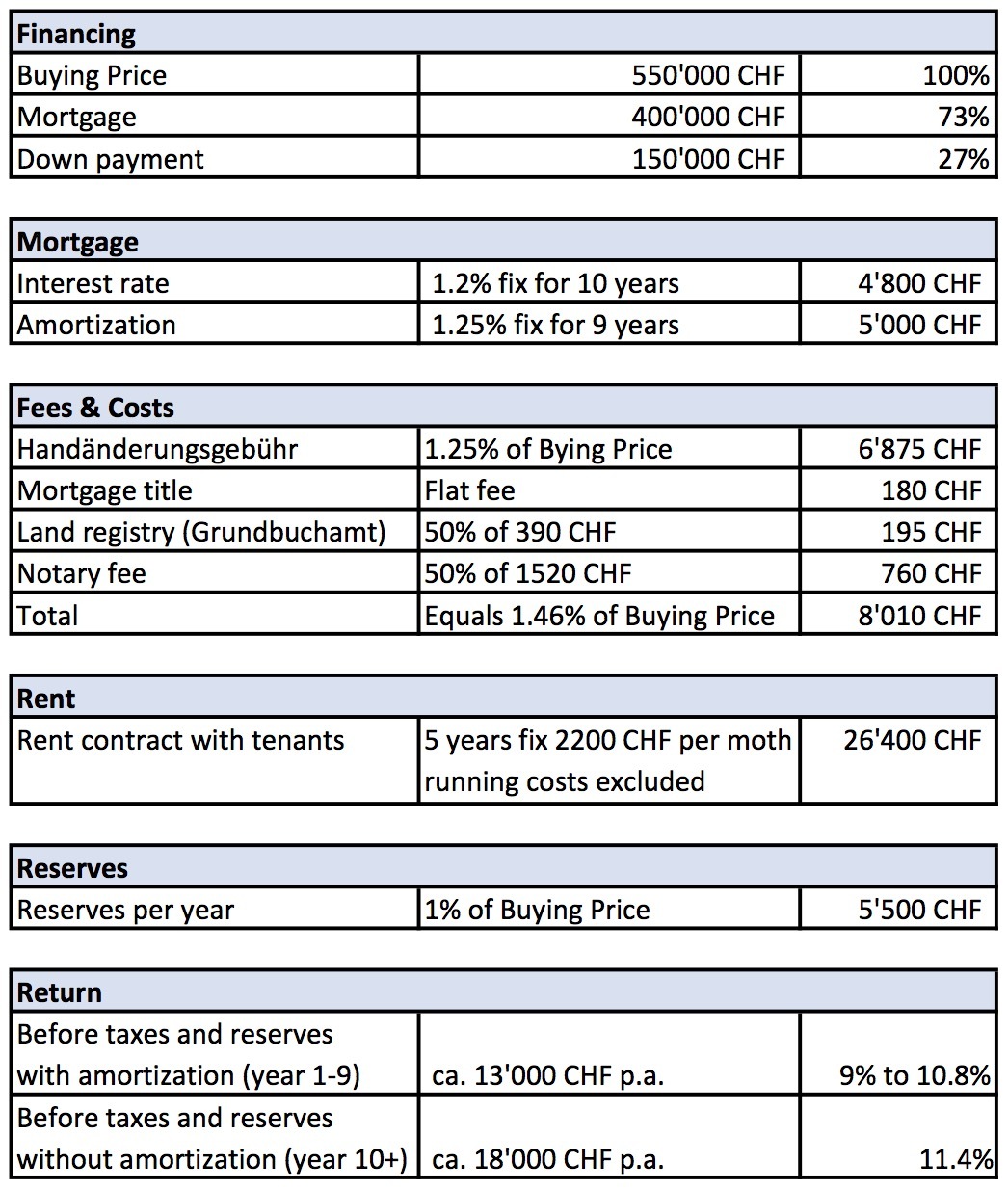

Very good job! Congratulations. Did you spend any money renovating something?

@ Grog: Thanks for the UBS reference. It probably is a combination of multiple factors that make it a good deal. It’s not a single family home but half a duplex which lowers the cost (land, facilities, etc.).

No renovations. The house is 8 years old and the rent stayed the same as the previous owner charged. Also the tenants are still the same. But I’m sure expenditures are going to increase over time.

I noticed that in your table you have no operating expenses. Are they truly all charged to the tenant? I was thinking about insurance, maintenance (excluding capital expenditure, etc.). I’m trying to run some numbers and the operating expenses seem to be what makes or breaks a good investment.

They are all charged to the tenant - except the buildings insurance which I forgot in the calculations as I have not yet been charged. The insurance of the previous owner is till running for the building. This situation might be a bit special.

Besides this I budgeted CHF 5500 per year for non-reoccuring maintenance costs which I think is conservative.

Everything I have read on this topic says you should consider the 1% rule on the monthly rent. You should be pulling 1% at least of the current market value (call it 550k) in monthly rent. This would be 5,500. Second is opportunity cost of your debt + equity (again 560k) invested in the market (index funds and bonds with similar risk profile. There iare some excellent writings about landlord maths on affordanything web site: http://affordanything.com/2016/04/28/one-percent-rule-gross-rent-multiplier

I am a landlord in Canada and found this site to be a great resource. Be forewarned -You might not like what you read with your numbers.

1% yield per month? Wake up from your dreams! We have a totally different country, market, currency and interest rates here. It’s not really comparable.

At best you’re looking here at 5-6% yearly yield net of NK (so called “Bruttorendite”). Look at the ads for multi-family houses to keep yourself informed of the trends. Recently properties even get advertised at 3-4% yield, which i find personally too low. I’ve even seen some bold ads with yield as low as 2.5% - I honestly don’t know who’d in their sane mind buy that, that probably wouldn’t even cover all the costs and a little extra for renovations. Probably same crazy so-called investors who buy negative yielding bonds.

You can probably get more, but only if you’re creative and willing to work long hours for it: maybe make a mini hotel out of it or WG, airbnb it, rip off clueless tourists with hidden charges… hehe

@SwissChalet I have to agree with hedgehog. I know affordanything.com. There are some interesting concepts but when it comes to numbers it is simply not relevant for the Swiss use case.

A daring hypothesis is that the US housing market has more in common with the housing market in a third world country than with the market in central Europe.

@hedgehog I just calculated the Bruttorendite (yearly rent * 100 / market value = 4.8%) for my half of the double family home which I consider to be a great deal.

Actually I am not dreaming or suggesting this sort of monthly gross rental yield is realistic in Switzerland and I do understand that things are different here. My own annual rent is at a 0.25% monthly yield to my landlord in Basel and I would never buy my house. Operating costs in Switzerland should not be drastically different to those in the US in terms of upkeep/insurance/prop taxes, meaning that a 1% monthly gross yield would typically get eaten up by at least 30-40% in operating costs so the idea behind the rule is that you should expect to net out 6-7% max on the MARKET VALUE, not the initial DOWN PAYMENT. The Canadian market (where I am a landlord) is currently very similar to Switzerland. Rents have not kept pace with property values and landlords have a lot of equity (or debt + equity) sitting in properties not working optimally for them. So we are in agreement that this 1% monthly gross yield is not a realistic expectation in Switzerland.

However I do not agree with using a different ‘yardstick’ to measure the feasibility of a rental-landlord investment in Switzerland because the opportunity cost (next best investment) appears to be, on this forum, some combination of US or World equity/bond ETFs and I have seen some (at least one) Mustacian post that he/she would not be willing to invest more than 3% in Switzerland investments overall. I could see measuring rental properties here in a more conservative ‘Swiss’ way if we were just comparing those to an alternate Swiss investment/REIT but we are not. Isn’t the bottom line then that Swiss real estate is not a good place to put 550k (whether leveraged or not)? Is 13k or even 18K a good return on 550k invested? Seems like a lot of ‘dead’ equity’ sitting around to me.

In fact I think the reason ElMago did not get much advice on this investment is because most Mustachians here are not ‘in’ rental property investments here in Switzerland. ??

The whole argument becomes moot anyway I suppose, as this investment was gifted to him, albeit with a few strings attached.

You can dream big, but let’s be realistic: nobody will sell you even remotely at 12% yield here. If somebody does, he’d be making you a big favor and the tax office will be after you on it for the gift tax.

12% yield at say typical 25 Fr/m^2 rental price per month in Zürich would mean 2500 Fr/m^2 apartment buying price. And have you seen the advertised prices? People are asking 10-15k/m^2! And it does get sold at these prices! Even before the prices started to skyrocket a decade ago, it was in the range of 5-7k/m2 AFAIK

Sorry didn’t read your whole post initially. When people talk about yields in real estate, they usually mean gross yields: yearly rent over buy price. 12% is not realistic.

What you seem to be talking now is return on investment or equity. 12% of such returns is realistic, depending how you compute - it’s less straightforward than gross yield

If I am not mistaken making 12% per year off a rental property would be considered abusive in Geneva. For sure the renter would be allowed to sign the contract and then fight it (successfully) in the first month.

making 12% per year off a rental property would be considered abusive in Geneva.

@Dago: As @hedgehog pointed out, the return is of the equity.

11.4% is the return with the current low interest rates without taking reserves into account (which should be around 1% of the property value) and it’s also before taxes.

Taking all of this into account, we get a decent but surely not abusive profit rate.

In a few years, I can better tell you, what the return will be but so far I don’t even exactly know how this will influence my taxes.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.