I am looking for a bank account to use as a salary account and to pay bills and purchases in foreign currencies. I should also be able to use Twint. I’m considering Neon and ZKB. Neon has the advantage of cheap purchases in foreign currencies, but it doesn’t have Twint (only UBS-Twint with much lower limits). ZKB has the advantage of supporting Twint. On the other hand, purchases in foreign currencies are more expensive. Of course, there is also the option of creating both accounts and using ZKB as a regular account and Neon only for foreign currency purchases. What do you think? Which accounts do you use? Thanks.

Neon is a Swiss company and has to follow Swiss laws - comparing to Revolut.

Saving money is nice, but not under any costs. If I save 10 Rp. per transaction, this does not justify - for me - the risk of potential account freezes as for Revoult (check the internet).

Also used Revolut couple of years ago, but switched to Neon.

For Radicant: they are under a lot of pressure, they even changed their business model, fee structure and BLKB had to write off hell of money so far. Same story for Alpian (change in business model, fee structure and needed more money from their main investor).

Decide yourself, how you weight different factors. But yes, in general, they all are suitable for FX payments.

I agree to be more conservative with an account containing lots of money. But if you keep as little cash as needed there (e.g. 1k) and only add more when needed, the risk to use Revolut or Radicant is minimal IMO.

Worst case my Revolut account gets frozen and I pay from the other “conservative” account (with higher fees) until the issue is resolved. Until then I save money on every transaction.

If this would be the killer argument, we should consequently also move away from IBKR (since it could take time to get your stocks unfrozen/moved in a worst case scenario).

Not just sending, also receiving. 5000 per year is very little.

Besides that: What are really the advantages of Neon over ZKB? Besides FX and if you use Neon for investing (I don’t), I don’t see any tbh. So probably I will use both; ZKB as main banking account, Neon just for FX.

True, but you have some withdrawal limitations there (10k, if its more you need to notify).

You don’t have that with e.g. Yuh or Neon afaik.

But I agree, if its more than 10k, maybe it would anyway be wise to store that at other places specifically optimized for interest (if it needs to stay liquid).

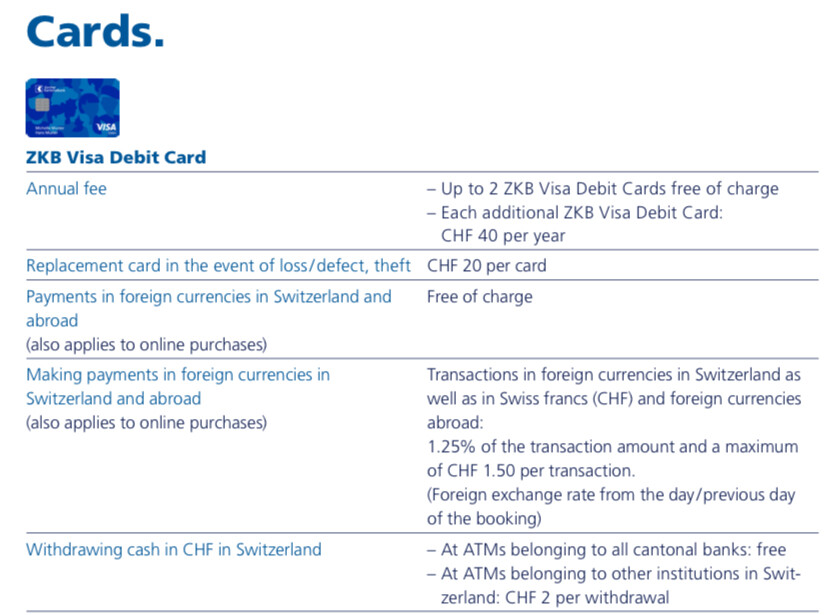

I am considering opening a ZKB account. I particularly like their option of joint accounts. One slight concern I have is regarding withdrawal. Although I don’t need cash often can somebody confirm if I am correct with what I read on their fees. Cash withdrawals (up to 10k/month) are free with the ZKB Visa Debit Card at any cantonal bank? Since I am not in ZH that would be the only limitation if I had to pay 5CHF/withdrawal for not living in ZH.

Here is the English version. It seems it’s free to withdraw cash from any cantonal bank.

However I cannot vouch as I live in ZH and I never used ATM from other banks. Basically I am paying no fees at all ever since they eliminated bank fees.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.