I was requesting details for a property, that will be done in late 2026.

Naively, I thought that you would pay a reservation fee out of pocket, then take out a mortgage upon completion. So this way the developer is guaranteed liquidity upon completion.

Unfortunately, this doesn’t seem to be the case. Between the documents, there was this “Zahlungsplan”, and it turns out that they’re financing the whole building process and then some with money from you. (I guess for paying ahead, you do get a sort of discount already in the price)

Questions:

Are there going to be 6 different mortgages, or a single one, split into tranches?

If split, are you contributing one-by-one, 20% for the upcoming payment?

are the interest rates fixed at the same time, or it will be different per payment?

In my case in similar situation construction payments had to be paid from construction loan (with higher than mortgage interest rate on it) separate bank account which I opened with my bank, then in my case after there is more than 100K debt in the construction account it can be consolidated into the mortgage (up to you to decide to fix it or take it as SARON). So to answer your question, yes it can end up with 6 different mortgages or you can group payments and consolidate at the same time.

For the second question, you pay 20% from the pocket first and then everything else is paid by construction loan the size of which you have to agree with the bank in advance (in my case it was possible to have some buffer in construction loan which basically paid the interests during the construction). Also construction loan can in theory finance some extra costs like more expensive materials, etc. if your affordability allows. So 20% + construction loan can be more than price of the house.

Interests rate are fixed at the time of consolidation. There is a way to fix it upfront but then you have to pay the premium and it is not the rate of today you will get the rate forecasted by the bank on the time mortgage will start.

What does grouping and consolidation mean in this case?

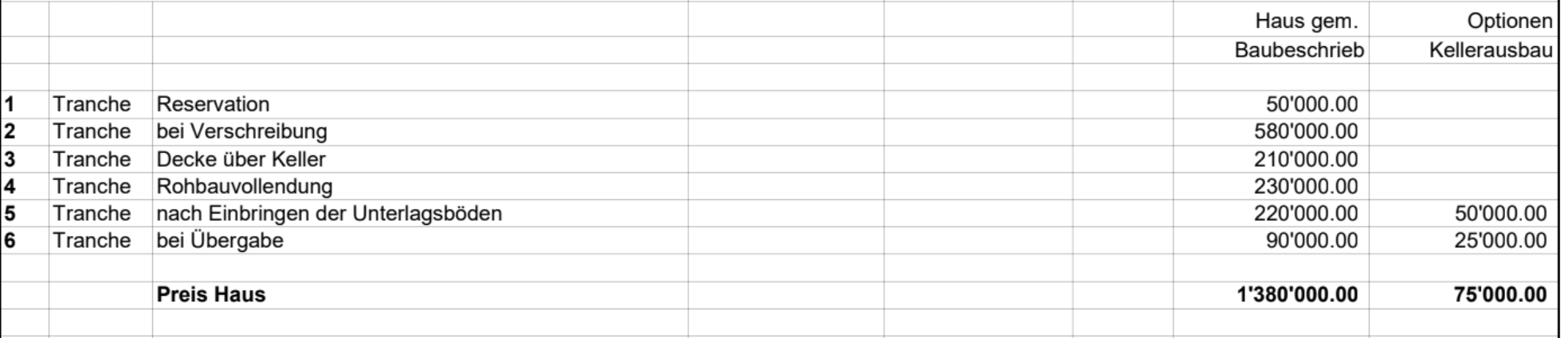

e.g in the scenario from the screenshot, would it be something like:

Pay 10k, that is 20% for tranche 1, with a rate of 2%

when the second tick of the payment is due, pay 116k for tranche 2 maybe at 1.5%. Consolidate these two together and have a new interest rate for the whole thing that is proportional with the amounts?

what it will mean in the basic scenario the following

1380000*0.2 ~ 280K (for easier math), should be financed outside of the mortgage and this has to happen before bank will start giving you money (there are other options (pledging, etc) but it will highly depend on the bank and goes outside of basic scenario)

1st payment 50K: pay by your own money

2nd payment 580K: 230K by your own money (so now 20% is covered) and 350K by construction loan, so now interest is to be paid on 350K of loan quarterly, also there is an option to consolidate 350K to mortgage to lower the interest or wait for next payment and consolidate 350K+210K=560K, and so on

In my mind debt consolidation is mostly for bookkeeping purposes.

e.g I won’t have X mortgages to pay, but bundle/consolidate them together, and at any time, I’m paying a single one.

In this scenario, by consolidating and converting into a mortgage you mean that until the 20% is not paid, you can get a loan only? After you reach that threshold you can convert your loan into a mortgage and from there either have more mortgages or bundle them up.

What I don’t follow in this approach is why would you even need the loan. If we pay the first 50 in cash, and then in the second tranche we pay the remaining 230 to reach 20%, the bank only comes in at this point, so it should be a mortgage to begin with. Am I misunderstanding?

A construction loan is a bit different from a regular mortgage. It’s a credit line.

Essentially, it’s a bank account from which the bank will pay the constructor in the schedule described in your document. But you will not get all the money at once in this account from the start (and thus won’t have to pay interests on everything from the start), only when you need it to make a payment.

When it starts, on this account you will have your own funds and pay nothing (depends on the exact details of the construction loan, but 0 interests anyway). Then, as they get depleted and you would go negative, the bank starts loaning you money. So if you need an extra 100k or you would go negative, then you start paying interests on those 100k. Then next month you need another 100k, and so forth until the end of the construction.

At the end of the construction, you don’t want/need to keep this account open. You want to turn the credit line/construction loan in a regular mortgage, that’s the consolidation. At this point in time, you know exactly how much you’ve borrowed in the end.

There are banks that allow you to consolidate before the end of the construction: every so often you transform the x you currently owe in the construction loan into a mortgage (which has lower interest rates). They all get added to the same mortgage.

It can be interesting because the mortgage rates are a lot lower than the construction loan rates (currently maybe 1.5% vs 2.75%). On the other hand, the banks like it because it binds you with them: you cannot consolidate early with a different bank than your construction loan provider. It means you cannot shop around when the construction is finished, and thus probably will not be getting the best rates. You trade lower rates during the construction (via early consolidation) for probably worse rates long terms.

As to why you cannot get a mortgage from the start and have to go through a construction loan, I am not entirely sure. It feels like you could “auto-consolidate” every time you need to make a payment, and the result would be the same. I assume it’s because in your case you only make a few big payments, so there won’t be much difference between payments to constructor and consolidation. But a construction loan can also be used to pay every little thing separately, so you can have a lot more transactions in the construction accounts, and only consolidate 2/3 times over the entire length.

Also, the loan type you describe is probably a good fit when there is uncertainty in the final amount of the construction, however, in this case, the price should be final, and it’s only a way for the seller to have liquidity and parallelise even more constructions.

I’m wondering if they would classify this as a construction loan, I think they shouldn’t.

I made an appointment with the bank for next week, will update the thread with their answer.

I am in a similar situation right now, and I don’t think you have any chance to get a “regular” mortgage which increases with every due payment, even if you only have 5.

Such a thing does not exist, or rather, it is the construction loan. It’s more work for them (and I assume more risks), which is why the interest rate is higher. Also less competition.

I’ll be interested to see what your bank says.

however, in this case, the price should be final

I would seriously reconsider that statement. If you read the GC contract in details you will find that:

some risks are not covered. E.g. if they find rocks or polluted soils when digging, you’ll be on the hook

a lot of things are budgets: 20k for the kitchen, 80 CHF/sqm2 for floors, … Then depending on what you actually choose, you might spend a bit more than budgeted

pretty much every change from the initial contract during the construction phase will result in additional costs (“we would like an extra socket in this room” kind of stuff)

One last thing, I do not see the land in your contract. Usually, that’s the first thing you buy, and it’s likely to use all your own funds and then some.

then in my case after there is more than 100K debt in the construction account it can be consolidated into the mortgage (up to you to decide to fix it or take it as SARON)

Do they really offer early consolidation as SARON? That sounds a bit too good to be true. I see the offer of early consolidation as a way for the bank to lock you in with them. If they offer you SARON, then what prevents you for shopping for a new mortgage once the construction is finished?

If that’s really the case, which bank is it?

in my case I had such option, so and the plan was exactly like this, to consolidate as SARON and shop for the fixed mortgage after construction is done. The bank name starts with U. Unfortunately I hadn’t stick to my plan until the end and because of raising rates fixed half of it for 2 years which is not too bad but a lesson to learn. So I ended up with half fixed and half SARON.

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.