The big increase is raising an old question of mine again: How practical is it to have basic and supplementary insurance with two different providers? I read that insurers are allowed to charge an extra admin fee, up to 50 CHF, which could quickly erase any savings.

Any experience with Sanitas here, if they don’t charge the extra admin fee?

(Once you have an ongoing / past treatment you can’t change supplementary anymore without loosing too much)

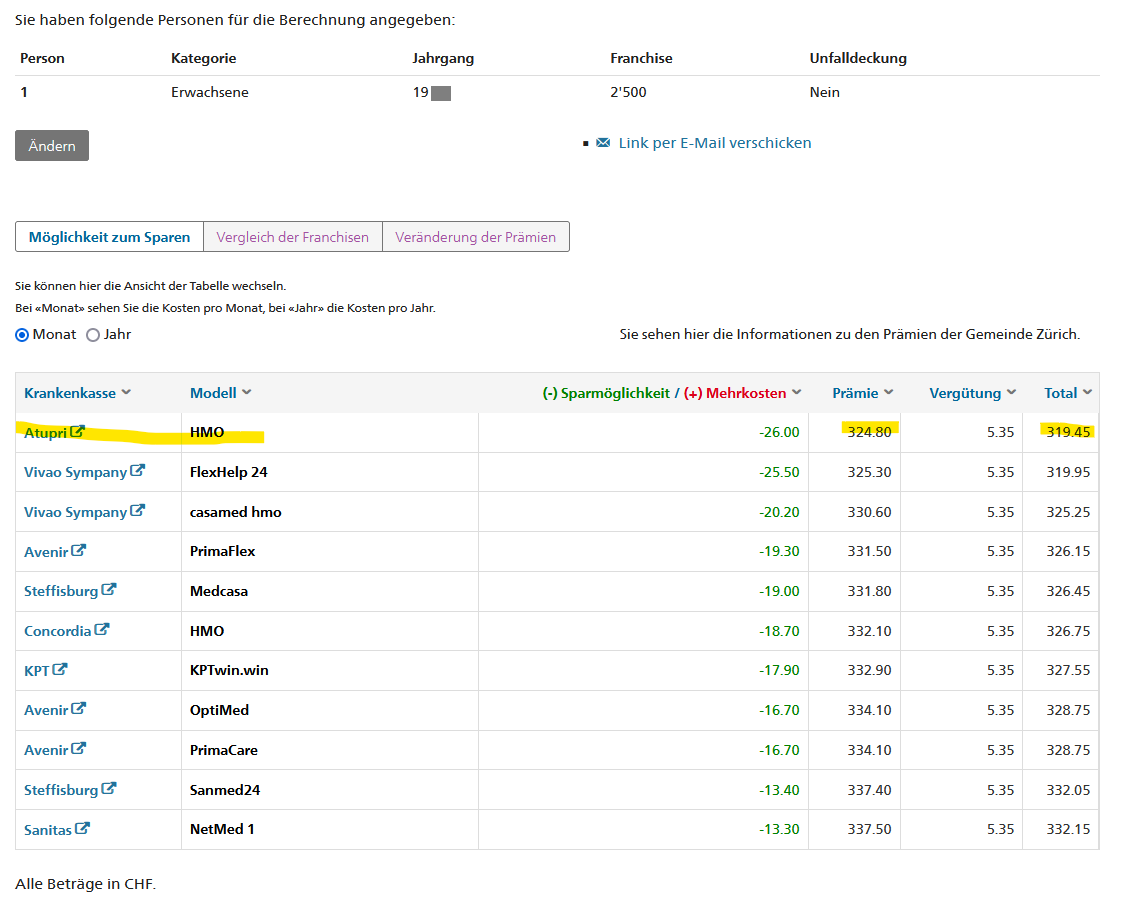

Any zurich city people here considering a move to Atupri?

I was with them long years ago, but never had to deal with them.

Interestingly, KPT and Assura are not at the top of this list

Those tables clearly shows that they talk to eachother. I can’t belive they don’t switch their position on purpose. Some Insurances moves too much on the classifications to be just normal business imho.

wouldn’t it show the reverse? I’d assume a “discount” insurer would want to stay discount. And vice versa (you might not want to have the people just going for the “cheapest” plan, switch for just a year, it’s a lot of cost/churn)

I called Sanitas and they told me they don’t either. Basic premiums are up a good 1200 per year for my family, so I’m seriously considering switching. Hard call, my experience with them has been really good, but at that price point…

@nugget : I have no personal experience with Atupri, but I read a NZZ article about their merger, which stated while they miscalculated premiums in the past and lost too many clients, forcing them into the merger, they are considered a good company otherwise. Also I saw a survey from K-Tipp, in which they ranked in the middle in terms of client satisfaction. Sympany was top, Assura was flop.

I will not consider them should we switch. Sympany is first on my list, then maybe KPT (which didn’t do too well in the satisfaction ranking, but I guess that’s because they were overwhelmed with new clients).

For my person, I will stay with Philos - Prima flex model.

The conditions are way better than KPT win.plus, the cheapest one.

The difference of CHF 11.30 per month is negligible compared to the very restrictive conditions I would get with KPT.

For the cheapest one for me (KPT win.plus) you can see that there is a lot of restrictions in terms of doctor or treatment choices.

If you do not respect, you get penalties.

Thanks for the pdf

That’s why most probably I will keep win.win, so I can have in addition telemed, decide the family doctor or in general where to go.

With telemed I can get a medical prescription, or go directly to a specialist, skipping the family doctor (and save the usual CHF 80-100 each time).

I will pay an additional CHF 200 per person per year. However, it’s a different service and can break even depending on the year.

Basically because it’s the cheapest and because for routine check-ups (dermatologist, cardiologist, …) I usually go to a neighbouring country paying 50%-70% less.

What is a huge red flag for me is that the conditions (link above) don’t mention anything about:

limitations of the choice of the pharmacy

tiers payant or tiers garant

And checking online doesn’t help at all. For example, for the tiers-payant/tiers-garant issue, I’m receiving contradicting answers:

I called Sanitas and they told me it’s tiers-payant. When I ask for the document in which it’s stated they point me to the T&C (in which it’s not stated!). So they could easily lie

according to moneyland it’s 24% tiers-garant and 76% tiers-payant (?!)

on frc.ch it’s tyers-garant. (Why should I trust an external entity more than the insurance company itself? I won’t be able to blame frc.ch in any case)

Who is right? The easiest solution is to have all the damn information in the T&C, and I can’t really understand how come the “best health insurance” has this kind of issue.

I don’t know if other companies have similar situations (this is the first year I’m very carefully checking the T&C).

I used to think that if you have a health expense that you can realistically plan (e.g. not urgent surgery), you could lower your deductible to 300 for the following year, do the surgery or whatever then, and increase again to 2500 afterwards. Some mini-optimization, together perhaps with change to semi-private and then revert back.

My insurer this year says they require a health check for any reduction of deductible (and I never did, nor plan to lower the deductible, it’s just an upfront information from their side)… is this common and/or can be challenged?

I’m no legal expert but Priminfo seems to say that you can lower the deductible without a medical exam:

In German:

Kann ich ohne Probleme jedes Jahr die Jahresfranchise anpassen?

Aufgrund des geltenden Rechts können Sie unter Einhaltung der Kündigungsfrist auf das Ende des Kalenderjahres von einer höheren zu einer tieferen Wahlfranchise oder zur Grundfranchise wechseln, unabhängig von Ihrem Gesundheitszustand. Bis zum 30. November muss die gewünschte tiefere Franchise der Krankenkasse schriftlich mitgeteilt werden. Die Wahl einer höheren Franchise kann auf Beginn eines Kalenderjahres erfolgen.

In French:

Puis-je sans problème adapter ma franchise annuelle chaque année ?

En vertu du droit en vigueur, vous pouvez en respectant le délai de résiliation opter à la fin de l’année civile pour une franchise moins élevée ou pour la franchise de base, indépendamment de votre état de santé. Vous devez avertir votre caisse par écrit, jusqu’au 30 novembre, que vous souhaitez une franchise plus basse. Le choix d’une franchise plus élevée peut également avoir lieu au début d’une année civile.

In Italian:

È possibile modificare senza problemi la franchigia annuale?

In base al diritto vigente, mantenendo lo stesso periodo di disdetta (entro la fine dell’anno civile), un assicurato può optare per una franchigia opzionale più bassa oppure passare alla franchigia obbligatoria di base, indipendentemente dal suo stato di salute. La franchigia più bassa scelta deve essere comunicata per scritto alla cassa malati entro il 30 novembre. La scelta di una franchigia più elevata può avvenire anche all’inizio dell’anno civile.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.