My question is simple : for all the invoices/services that you can pay yearly (and often pay a bit less in the process), does it make more sense to do it, instead of monthly?

I always paid monthly so far, it seems more logic to avoid spending one big amount of money at one time. But on my way to the mustachian’s transformation I’m starting to think that it can be an additional economy…

From a ROI point of view it doesn’t probably make sense. What you usually get by paying in advance is about 1-2% annually and that’s lower than what you can expect on average with an index fund.

On the other hand I sometimes pay in advance for few reasons:

I consider them as bonds/money market to balance the rest of my portfolio that is heavily invested in stocks. 1-2% is more than what you can expect for a safe investment in CHF nowadays.

I do it once per year and I don’t need to think about it the other 11 months

Same as Paolo, here. They are a short term investment and my cash allocation is aimed at covering short term needs so I consider the difference between already paid services and the remaining amount to be paid until the end of the year in my cash allocation, allowing my cash to earn a tiny bit more than the 0.0x% they would do in a savings account. The wealth tax savings should be counted in that increased returns too.

Be sure to still have enough cash to cover your other expenses for the length of time you expect it to (that is, I wouldn’t let my actual cash allocation go negative - or too low (think <1 month of expenses) - due to this accounting).

You pay on the 29 december, so you don’t pay wealth tax on the full amount for that ending year. Then of course you’re richer because of savings and tax savings but who cares If you pay a bit more on that small amount.

In practice does caring about those things matter? Aren’t those bills like a few percent of your income at most?

Changing jobs or getting promoted is probably going to matter order of magnitude more In the end there’s only one thing that matters, savings rate and once the low hanging fruits are done in terms of lowering spending, the easiest is often to increase the income.

I don’t care about investment returns and opportunity costs.

I‘m managing it on a purely “psychological” basis:

Daily consumables and discretionary expenses are always paid by credit card

Basic monthly necessities and (quasi-) monthly bills are paid from income on my current account: rent, electricity, internet, incidentals and the monthly credit card bill. All on a relatively tight budget.

Larger yearly expenses (some of which I deliberately chose to pay annually) are paid from my savings account: tax, health insurance, yearly 3a contribution, transport pass, education, travel.

I‘ve set up a monthy standing order to transfer the sum of anticipated yearly outgoings from my current account to my savings account in monthly “instalments”.

I’ve also set up a monthly standing order to transfer a fixed sum each month from my current account to my investment account.

At the end of each month, I swipe the remaining balance on my current account and transfer to my savings account as well (though every once in a while I cheat and buy me something really nice).

At the turn of the year, after having paid all yearly expenses (and for christmas gifts), I swipe the remaining balance from my savings account as well, transferring it to my investment account.

That basically sums up the entirety of my cash management strategy - and budgeting as well. I’ve just had to come up with a reasonable yet somewhat tight figure for monthly consumption and expenses that I’m allowing myself.

Thanks for the detail, I really like your setup. I have something like that in mind, but I’ll have to create some buffer first to be able to pay yearly the first things.

Is there a discount with taxes if you pay early, instead of the monthly slice during the year and the final balance the year after?

To be more precise, where is your saving account? I guess income in a standard account, investment account in stocks/EFT/whatever, but the saving once? Another standard account or something more specific?

It is all, as they say, no rocket science by any means.

But it there’s a couple of things that make it work very well for me:

A considerable part of my income each month will be invested fully automatically.

I actually don’t think much about my day-to-day spending. Personally though, while I enjoy good lunch and some chocolate at times, I’m not prone to spend on alcohol, soft or energy drinks or expensive coffee - or make impulse purchases for small-ticket items (other than food, sometimes).

It is not rare that my day-to-day current account will be empty at the end of a month, just due to the bills I have paid. And I really want to avoid digging into my savings. That makes me feel like living "from paycheck to paycheck". Some months it’s not hard, others it really is a bit of a challenge to stay within my budget before the next pay day, if an unexpected bill hits. So keeps me being frugal.

I am getting monthly “feedback” on my expenses by seeing how much is left after having paid that credit card bill.

If I then still manage to save just a few, maybe two or three hundreds on and until pay day (or manage to squeeze that yearly SERAFE bill into my monthly budget), it feels innately rewarding.

…whereas my yearly spending and bills are otherwise pretty much fixed or predictable. Paying them annually reduces the wiggle room on my monthly “accounting”, thus lets me focus more on my monthly spending habits. That’s why I prefer annually payments.

I think the tax office used to pay interest on early pre-payments of around is 1% (until the payment deadline) up to a few years ago. That was quite good but they have drastically reduced it in recent years.

Since the interest rates are basically zero everywhere anyways, I just use my Cler ZAK account. They regularly offer “Zak Deals” on payments credited to the account, that let you buy discounted vouchers for online stores.

I made a quick excel to quantify this topic here.

input parameters:

yearly health insurance bill of CHF 3500

2% discount if paid upfront

5% return on your investment portfolio

compounding calculated monthly

no wealth tax considered

case 1: pay upfront, and compound the discount saving on the portfolio

case 2: pay monthly bill, and invest what you havn’t spent yet on paying the monthly bill

result: case 2 gives you CHF 37 more than case 1

which results in CHF 1200 over 20 years.

although this is very small money, makes me reconsider my billing system…

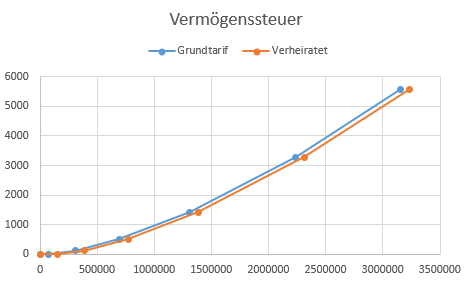

If you want to add wealth tax, see here (ZH)

ore visualized:

Paying upfront should be considered a cash allocation in my opinion, so it should be compared to cash rates of returns, which would make it more attractive. If you have no cash allocation neither emergency fund, then paying yearly doesn’t make much financial sense to me.

Edit: Thanks to nugget’s spreadsheet (thanks!), with a rate of returns of 0.5% for cash, option 1 whould come ahead by CHF 59.00. Safe assets are not there to generate returns, so it’s not such a big deal, but it’s still interesting to see that if we keep only a small allocation in cash, there are still some alternatives to generate some returns on it.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

In the end there’s only one thing that matters, savings rate and once the low hanging fruits are done in terms of lowering spending, the easiest is often to increase the income.

In the end there’s only one thing that matters, savings rate and once the low hanging fruits are done in terms of lowering spending, the easiest is often to increase the income.