quite some people on here work in the financial sector and/or have an entrepreneurial background. a thought that crossed my mind regularly in the past couple years:

someone should really disrupt VZ [vermögenszentrum] and the likes (and make some nice money in the process).

vanguard-like, bezos style “your margin is my opportunity”, right?

tough challenge, i know. but hey, there’s a tiny chance we could connect the right people, so why not ask?

so, in case there’s any interest, step forward!

thanks,

your [non-executive] board member & venture capitalist

I was involved in due diligence for a German Fintech who was looking for a banking license and wanted to disrupt the likes of Revolut and Robinhood with trading, credit cards, payments and later move into wealth management. They never made it, but due to other reasons.

Size matters and I believe the Swiss market is too small. Also, regulations might be the reason for higher TER in Europe than in the USA (Vanguard products).

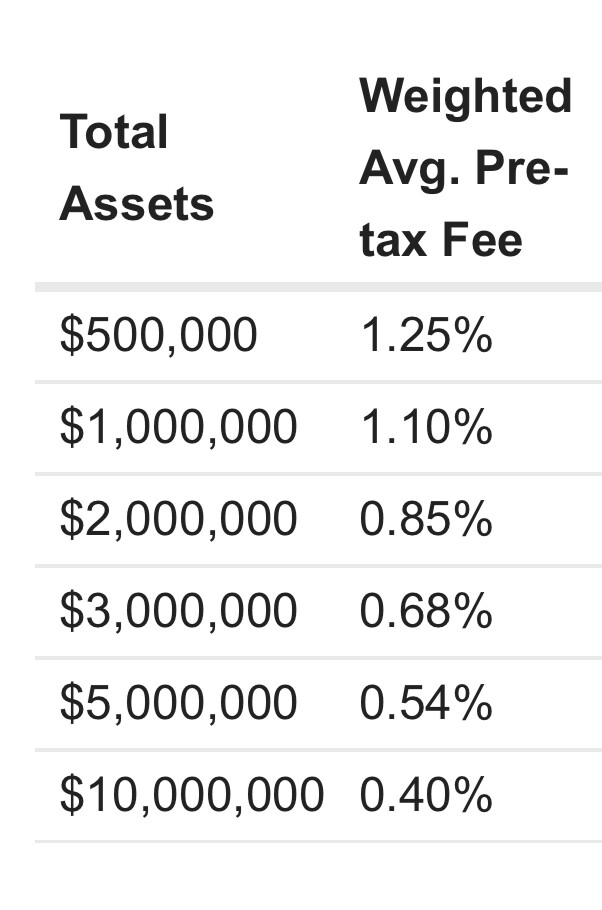

What AUM? I thought the point was to provide financial consultations/planning without any assets management.

White coat investor writes a lot about this problem: there are hardcore DIY in investing, there are delegators, but there are also validators - people who would like to check from time to time if they are on the right way. They also write how difficult it is to get a fair advice for a fair price, and that many calling themselves financial advisors are selling financial products “designed to be sold, not to be bought”.

And this is in US. In Switzerland, I feel that it is even more difficult for an average person to get a fair financial advice without being scammed. Catch 22: if you need an advice because you don’t have enough financial literacy, you are going to have difficulties recognizing that you are given a bad advice.

I’d also be interested. Although I do have concerns about the business model. There are the “sheep” who buy what their house bank tells them to, the Rappen pinchers like us who agonize about 0.01% p.a., and those between who would be potential clients. And I don’t know how big that middle group is.

I think that VZ do a fairly decent job. They are cheaper than traditional banks, are relatively independent, offer fee-based advice. Also they are positioned more towards people 50+, with a lucrative pension market in mind, people with some assets (so worthwile financially for VZ).

Although I still think there is potential for other providers. Maybe for younger people? I often feel they are lost with what they should do with their money, how to invest. Probably also open to a more digital experience.

What about an investment platform that focuses solely on ETFs (just found InvestEngine in UK, maybe something similar). But then there are already Neon, Yuh, VIAC finpension with a large customer base, but still open to have a better product maybe.

I think the big challenge is the acquisition of customers. This will cost a lot for marketing.

I think will be hard to have cheap and good advisors, my feeling is that a good advisors can get fairly high rates. And a bad one can also get decent income selling life insurances. Not clear to me where the disruption would come from unless you automate everything (but then comparison is robo investors/neobanks)

So- don’t buy active funds - but end up paying same fees for index funds

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.