I think it’s lower based on other feedbacks.

Finpension use CHF funds in 3a.

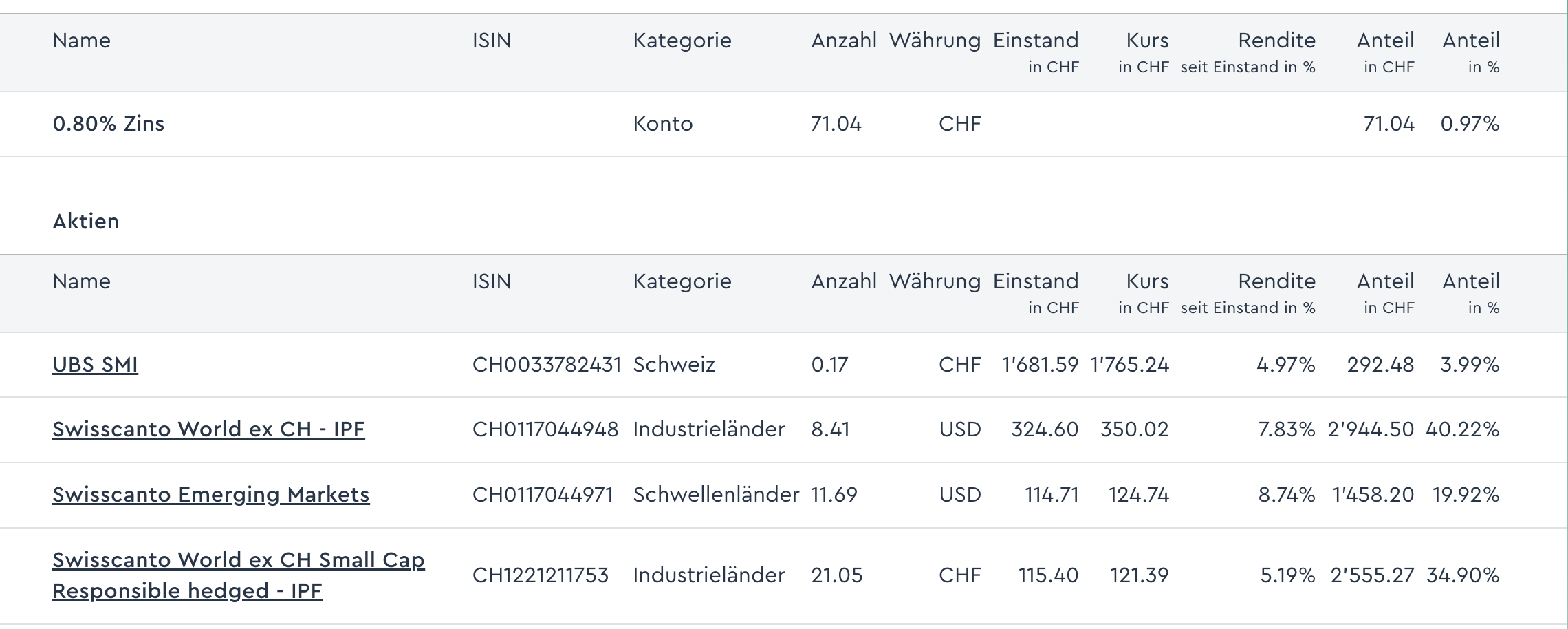

Mine is:

VIAC strategy to replicate an all world ETF:

• 86% - CSIF World ex CH - Pension Fund Plus

• 10% - CSIF Emerging Markets

• 2% - CSIF SMI

• 1% - CSIF SPI Extra

4 Likes

The news announced and discussed on the other thread

Swisscanto emerging market should have lower fees than CSIF.

Thinking about the minimalistic approach:

90% CSIF World ex CH - PF Plus

9% SPI

1% Cash

Still overweighting Switzerland four times (Swiss contribution to an All World Etf is around 2.5%)

Any considerations for this minimalistiv approach from you?

2 Likes

This is my test strategy of replication of the all world ETF to beat Global 100 . Started at 21.11.2023 and im now +18%

1 Like

For the reasons mentioned in Comparing 3a fund performance: ETFs vs. CSIF, Swisscanto, UBS - #51 by covfefe, I’m gonna go for 99% CSIF World ex CH instead.

thanks for this. seems like you even more minimalistic…! you write, that with one fund, there will be less fees. as far as i got it, fees are fixed anyway in viac (around 0.4%), regardless of the rebalancing. offtopic: i was asking myself, if the hedging in chf (awailable for seweral funds) comes with higher fees or not, because the fees writen in the ‘viac-fund-selection-menu’ are the same and im wondering, if/why you can get this hedge for free…

The cost of hedging is built-in the fund itself and is not even reflected in the sticker TER. So no, it is not for free.

2 Likes

Are you guys switching your 3a Strategy in cash instead of stocks ?

2 Likes

In general it’s a bad idea to react to market event (it’s a sign you really overestimated your risk appetite, normally there’s no reason to change allocations).

3 Likes

No, 3a is too inflexible to shift around to new allocations. If you want to sell something I would do it outside of 3a. I personally will be shifting more to CH-Stocks in 3a, perhaps exclusively so, howeber this drop messed with the timeline

No… buying more today using my 2025 deposit which I was waiting to deploy.

Yesterday I allocated it to equity (unfortunately VIAC/Finpension only rebalances on tuesdays instead of daily)

I’m not close to retirement (and if I was my allocation would look different anyway)

2 Likes

I’ll keep

5% IBIT

10% Gold

5% Commodities

rest cash

I am keeping same strategy…

5% IBIT

15% GOLD

79% Stocks (World ex CH , CH, world High dividend)

99% stocks (Dev ex US), as usual.

(US and EM etc. are outside of 3a)

3 Likes

I have gold, commodities, real estate and stocks.

Current allocation:

CH0429081620 CSIF World ex CH – PF Plus - CHF (fee 0%; Subscript. Fees : 0,05%; Redempt. Fees : 0,02% ) : Allocation = 78%

CH0214967314 CSIF World ex CH Small Cap – PF - CHF (fee 0%; Subscript. Fees : 0,10%; Redempt. Fees : 0,06% ) : Allocation = 10%

CH0117044971 SwissCanto Emerging Markets - USD (fee 0%; Subscript. Fees : 0,17%; Redempt. Fees : 0,23% ) : Allocation = 9%

CH0215804714 SwissCanto SMI - CHF (fee 0%; Subscript. Fees : 0,01%; Redempt. Fees : 0,01% ) : Allocation = 2%

Crurent allocation:

- Cash - 1%

- SPI ESG - 29%

- World ex CH - 70%

I’m thinking to going back to the VIAC Global 100 strategy. I will see by the end of next year.

Did anyone do a thorough analysis on individual funds, instead of a stand-alone strategy? Meaning within larger portfolio, what to move to 3a or VB first?

I do remember some discussions, but could only find some posts in the tax optimization thread. Is there some specific discussion I missed in my search, not only limited to VIAC but in general?

There’s a nice comparison from Dr. PI, and I tried some ranking, based on fees and taxes, with assumptions on dividends etc. but not detailed enough to be conclusive.