Struggling to replicate VT through VIAC without using CHF hedged funds, I’m not really sure how to approach this correctly. Obviously you have to overweight Switzerland massively as the law requires you to invest atleast 40% in CHF, so that’s why (without hedged funds) you are forced to invest 37% in Switzerland, 3% cash.

What about the rest? How did you manage this? I don’t like the idea of having 28% in SMI with the Global 100 solution. I’m thinking more about 5-12% SMI and 25-33% SPI Extra. The other 60% would be invested according to VT (so 60% x 55.3% for USA = 33% SP500 for example, 7% EM, 5% Japan, 3% Pacific ex Japan, 2% Canada). Leaving 10% left either for Europe ex CH or World Small Cap. As Switzerland (with 40%) is already part of Europe, 10% World Small Cap makes more sense.

My recommendation is to look at all your assets together. Instead of mentally dividing them up in pots, make one strategy/asset allocation for all, taking into account the limitations and advantages of each pot.

E.g. 3a is only ~7k per year. Fees incl. currency exchange are more expensive. Dividends in 3a can compound untaxed. Switzerland and Europe have high dividends. If you choose a package with VTI, VEA and VWO, you could slightly reduce VEA for example.

Look at your assets holistically (together).

Edit: SLI is a variant of SMI that helps to reduce the strong weight of the 3 heaviest components (Nestle, Novartis, Roche make up over 50%). This might also be an option.

I looked into allocating more of my VIAC 3p to REITs a while ago.

This is because REITs have equity like returns and owning some will slightly lower your portfolio volatility.

Under Swiss tax, REIT returns are taxed as dividends/income so they are very unfavourable to hold as a taxable investment compared to equity (no capital gains tax.)

3p could be a good solution as there is no tax on dividends when held in the 3p.

However, my conclusion was that it was more effort than it was worth for my current situation. You can only allocate a certain % (I think 30%) of your 3p to REITs so it would give you a max exposure of a bit over CHF2k a yr. At the start of a 40yr time horizon intra-year volatility is a bit irrelevant to me.

I was looking for which thread to add this to, and this Thread title fits perfectly, even though I am aware the OP meant asset allocation of different securities/ETF’s in a 97% security scenario within 3a, and not asset allocation cash:securities.

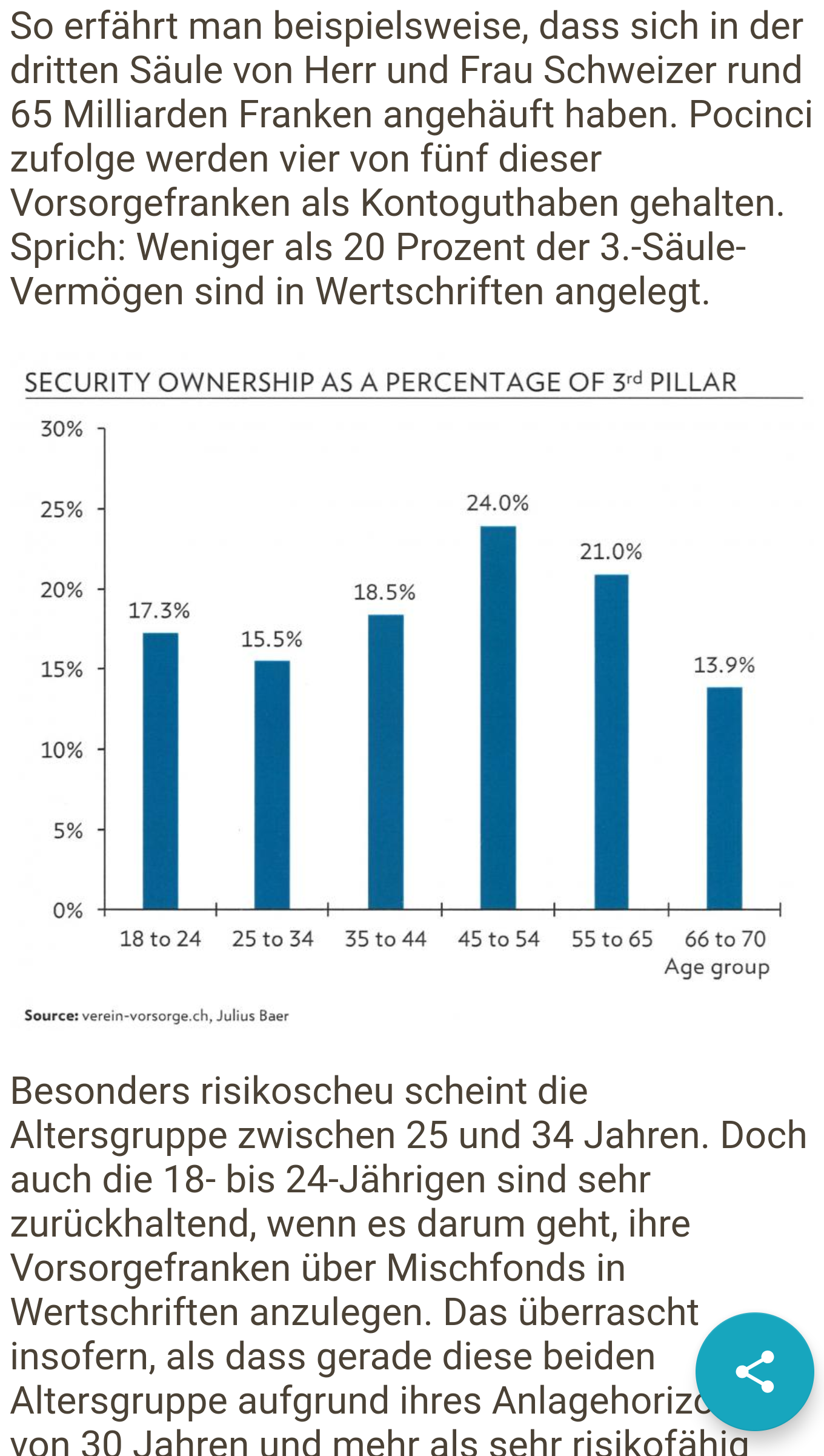

Anyhow the graph (probably) shows the (100% - cash 3a accounts) allocation within 3a assets in CH.

Crazy to see how low risk (=low win) even the age group to 34 keeps their 3a assets (almost 85% in cash, earning 0.1 to 0.3% for the next X years).

This is from an article on the cash website, I tried to find an original report with more info, ut couldn’t find anything.

Especially the verein-vorsorge.ch interested me, until I found out the members are all 3a fund providers, so it’s just a lobby organisation really. They are lobbying for an increase in the yearly amount, esp. if you haven’t paid in a lot in younger years. That would be interesting for an expat, come for a few years, max out payment for your age (thereby reducing income tax), then cash out after a few years at a reduced tax rate when u leave.

Here’s my strategy:

2% CSIF SMI

2% CSIF SPI Extra

50% CSIF World ex CH - Pension Fund

33% CSIF World ex CH hedged - Pension Fund

10% CSIF Emerging Markets

3% Cash

My goals:

Diversify as much as possible

Not overweighting the swiss market, but a good diversification too (that’s why I took SPI Extra as well)

The hedged fund is not that nice, I know, but better than holding cash

Why not look at the whole of your wealth when allocating, you likely have other things besides 3a, right? Unless 3a is a large part of it, you can always rebalance on those other things (e.g. keep cash outside for example, there’s little benefits to have the cash part of the portfolio in 3a, that’s losing tax benefits you could be using for other assets).

Is that an ETF of the SXI Real Estate Funds Broad ? I don’t advise to buy the index; and I dont’ advise to hold funds that owns directly the buildings (or the index, which is partially composed of those funds) in the 3rd pillar, but outside of it for tax reasons.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.