But practically I think I have only very little of the big high flyers in my portfolios. The reason is that I started too late, like <6 years ago with my momentum portfolio. For that short time I had quite a lot of high flyers (>1000% return), but had to sell most of them already.

Theory or practice, exponential growth cannot be eternal. So in my opinion the most important is position size followed by sell rules. Or in other words, money management and position management.

It is true, most of the long term gain comes from very little companies, I think 3-5%, the rest does hardly beat inflation over 25 years. But then there are shorter periods where a lot of other stocks do very good. I try to catch at least some of them. Knowing that I probably cannot hold forever I go “hold as long as possible… but not longer”.

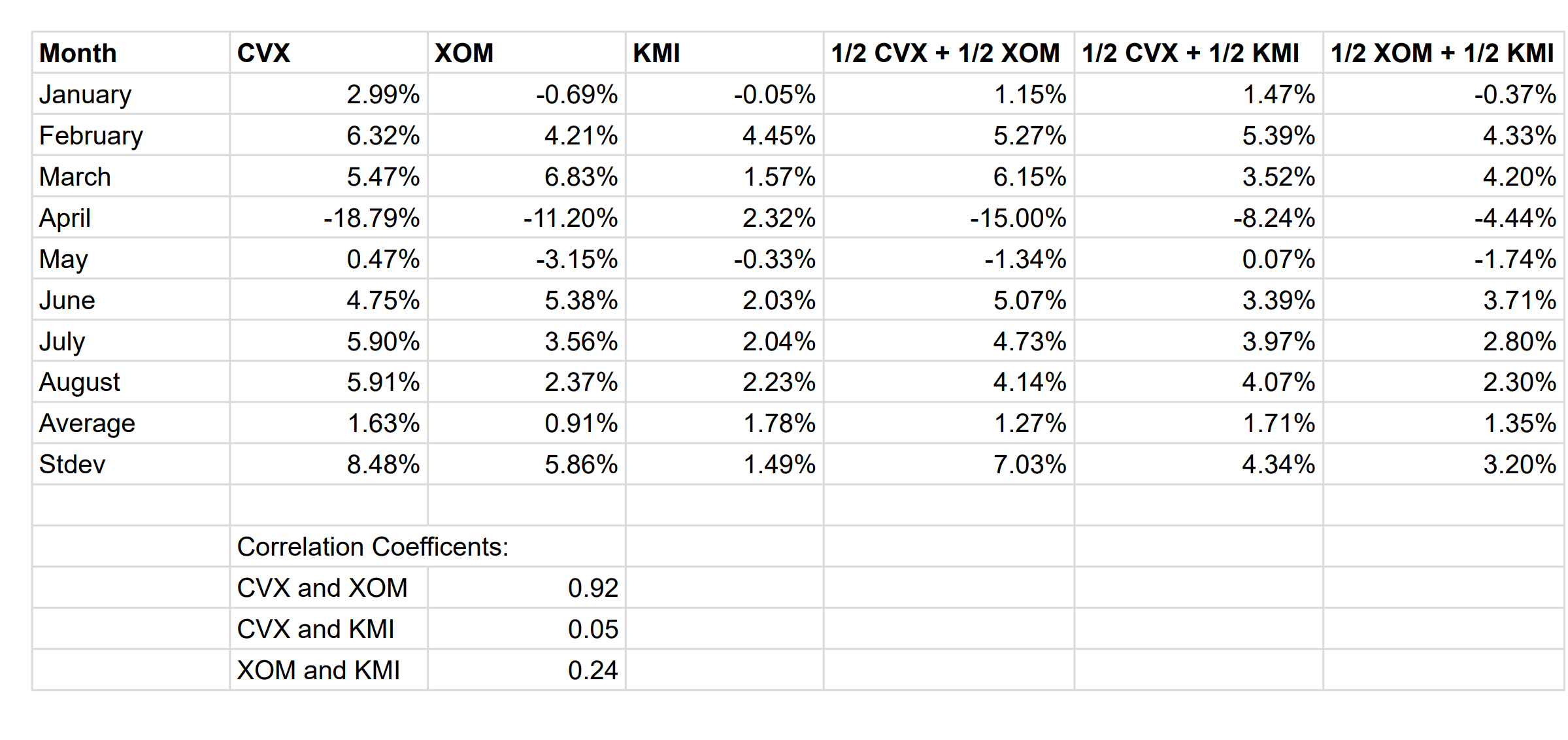

It depends on the stock, not just the number. If you have XOM and CVX, there’s probably not much diversification benefit there.

If you hand picked stocks for max diversification, I think you could get there with 6. Maybe if you had a limited universe to choose from you’d need 10.

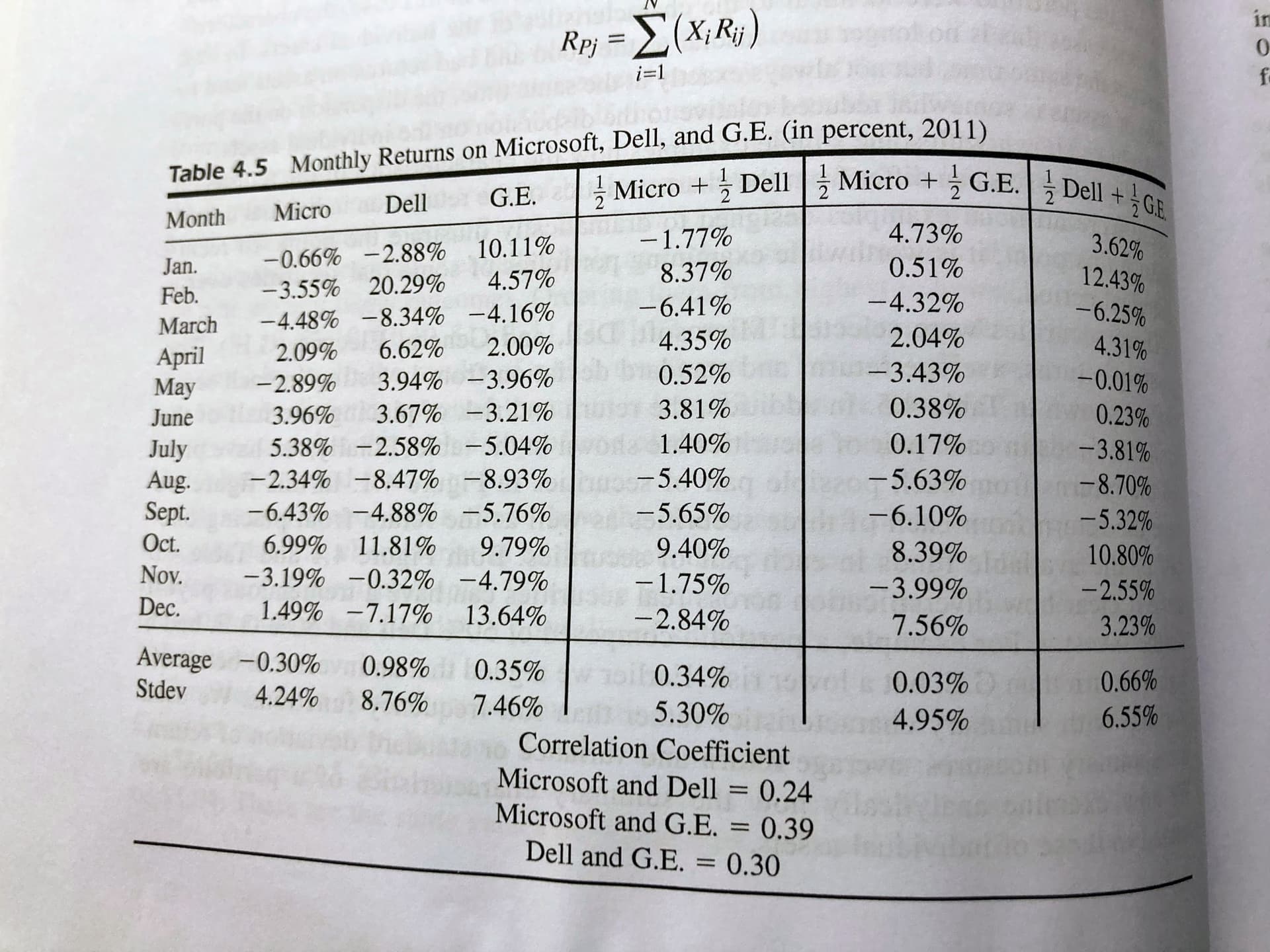

In my MPT textbook (for the reference see above) the authors look at a diversified (was tempted to put the term in quotes) portfolio of Microsoft, Dell and General Electric over the course of 2011.[1] Turns out over the course of that year, the returns were as follows:

So probably best to mix CVX and KMI based on January to August of 2025.

I’m still fairly opposed to equal weighting sectors, but I don’t have the numbers to back it up, just a gut feeling that market cycles will take care of balancing out allocated sectors in my actively managed part of my portfolio, and that within sectors, you’ll see some divergence – as with CVX/XOM vs KMI – as well.

All numbers price returns only (without dividends).

1 In my naive first look I thought that at least Microsoft and Dell were fairly highly correlated in terms of returns.

Edit:

E Just picked somewhat randomy three out of the Energy sector for 2025. Two seemingly highly correlated ones (as suggested by you), one less correlated one.

My tobacco portfolio (Altria $MO, Philip Morris $PM, British American Tobacco $BTI, Imperial Brands $IMB.L, Japan Tobacco $2914.T; reluctantly equal weighted) has done a pretty good job at growing over the last three years and set off a ton of dividends

Yes, but they’ve started paying dividends recently (low payout ratio) while continuing to grow revenues a nice pace. A lot of room for dividend increases.

What is the PayPal business? Is it still mostly online transaction processing? Don’t they have a lot more competition in that area from Stripe and a plethora of new entrants?

But that just covers 0.5% of the cash flows between people in Italy. The 99.5% transacted (by the mafia) still uses just plain cash in physical envelopes …

First some stats: they’re growing revenues 6-7% annually, 19% EBIT, have a PE ratio of 12, will starting paying a close to 1% dividend in 2026 (10% payout ratio), have close to zero net debt,.. so plenty of room to grow that dividend.

Re Paypal itself covers multiple lines of revenues:

credit (consumer and merchant),

Branded Checkout (its core business),

PSP (payment service provider - i.e. unbranded)

value-added services (this bucket includes non-transaction-based revenues, such as: interest and fees on customer balances and funds held; revenue from partnerships (e.g., PayPal’s rewards, currency conversion fees); referral fees and data/analytics services for merchants; other financial tools, like fraud protection and payout services)

and Venmo (peer to peer payment app)

Branded Checkout makes up ~30% of volume, but ~2/3rds of transaction gross profit. Growth rates (and margins) of the different revenue lines differ.

They have different competitors depending on the revenue line.

I think the technical term by Benjamin Graham is “cigar butts”, but in this case it seems you picked up just a filter. Anyway, some filters are known to grow into full tobacco trees, I think that’s why Greeks like to plant them in the sand in the beach.

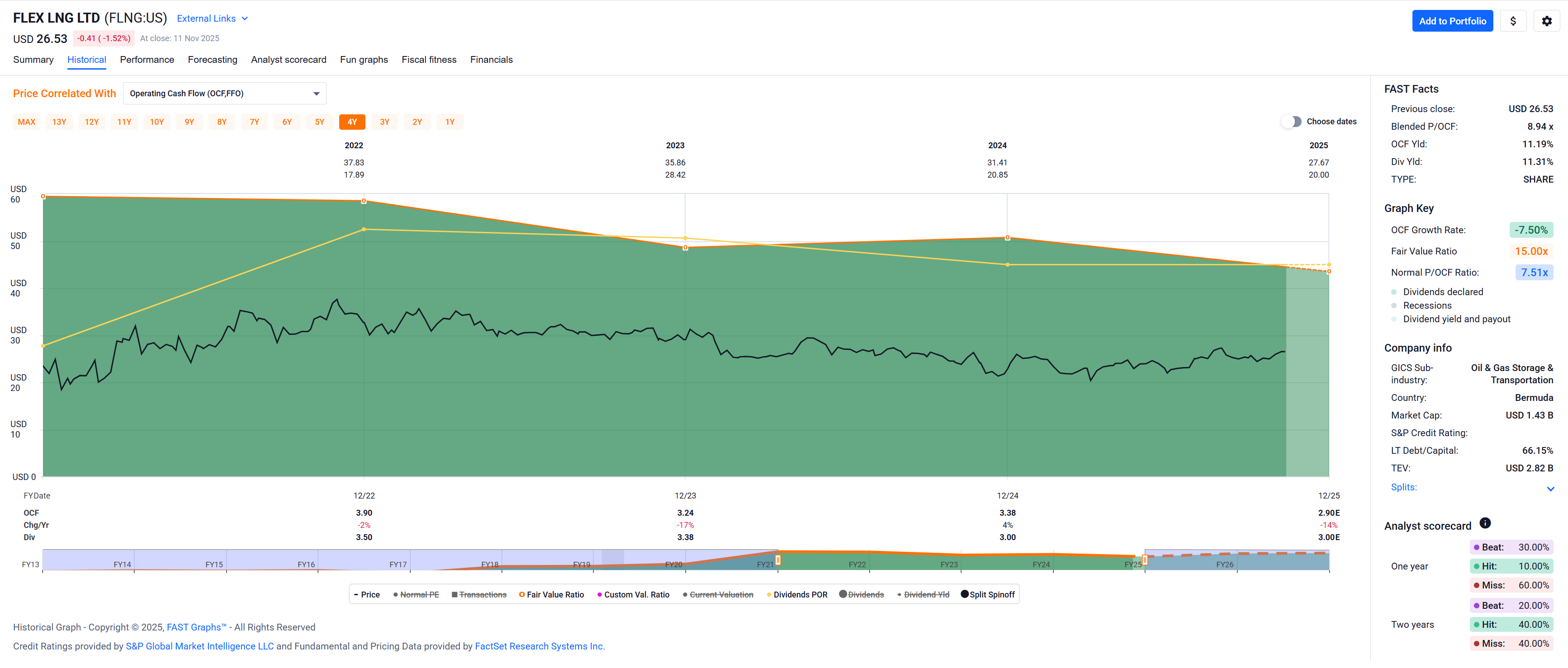

Eh, yield means nothing, around 2021 the yield was around 3% if I squint hard enough!

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.