Well, of course I don’t know the reason, but as Chuck Carnevale – co-founder of FASTgraphs and known as Mr. Valuation – would say: price follows earnings.

This seems roughly true for RB as well over long enough time frames (see FASTgraphs above). Earnings for RB have dropped last year and are expected to drop again this year and price has seemingly already followed?

Earnings are expected to grow again next year and afterwards and I would expect price to follow (up) again, eventually.

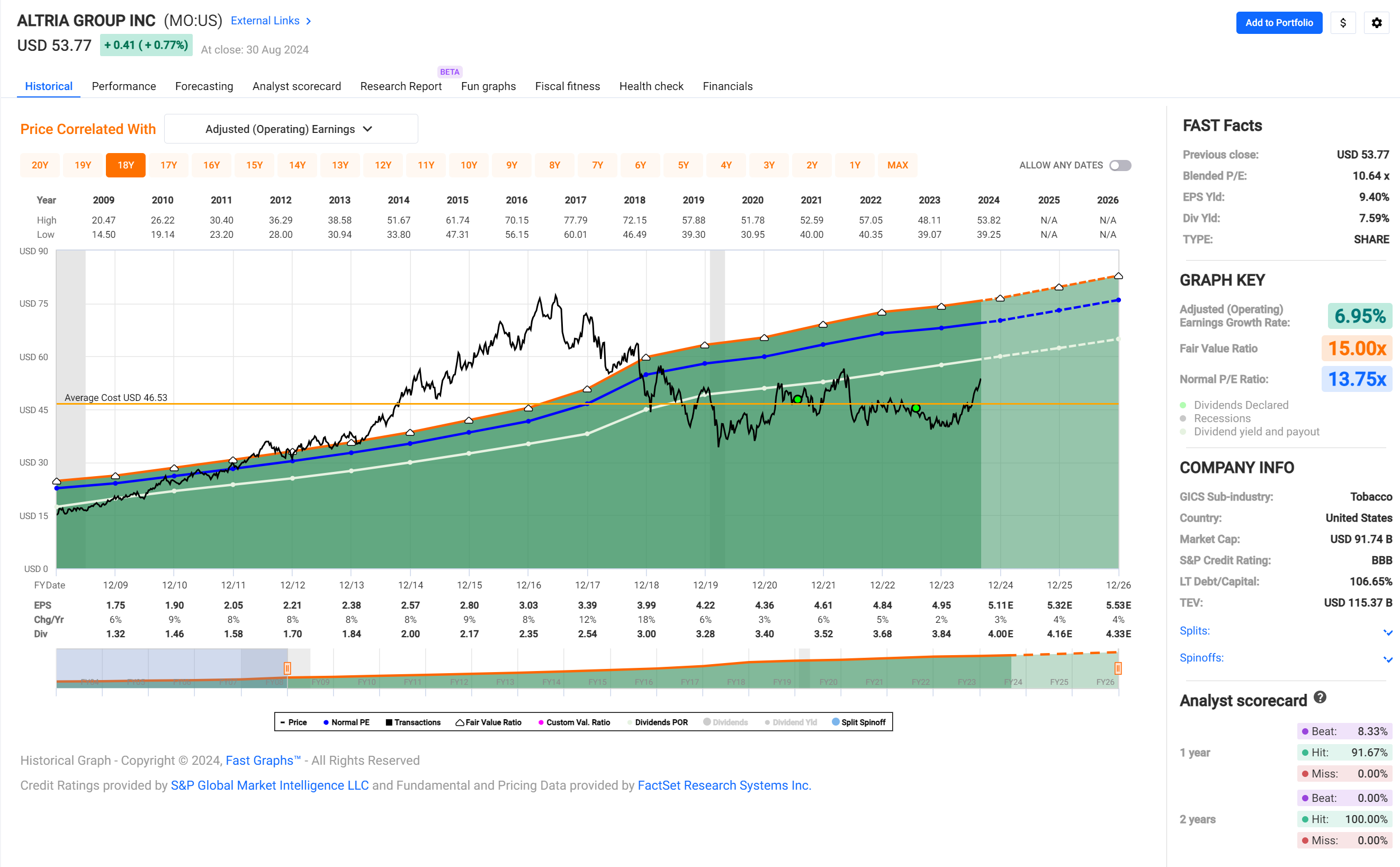

No prediction of course as sometimes it takes more than one or two years for price to follow earnings, as e.g. everyone buying Altria in the past six years or so would have to admit.*

While waiting for Altria's price to follow its earnings, you can console yourself with that dividend cash flowing in ... at least that's what I am doing. :-)

I personally like to invest in …CHDVD. That’s the lazy way of investing in dividends

I am tempted to use my PF credits to buy some swiss insurance stocks though. As a waaaaay generalistic reason I’m not afraid of the impeding loom (global warming, wars etc) since 99.99% of the time insurances don’t pay that kind of risk.

Will be interesting to see if there’ll be a sector rotation (towards div yield stocks) happening given lower interest rates coming and tech stocks valuations being so high.

" Convincing plan to unlock value

Drastic portfolio reshuffle to give rise to a compelling reliable compounder

Yesterday, Reckitt took the opportunity of its H1 results to introduce a new ambitious

strategy which should drive a drastic reshaping of the company’s portfolio over coming

years. Reckitt’s plan effectively means that 29% of the group’s turn over is now under

strategic review with the group looking to divest £1.9bn of non core Hygiene revenues

(13% of sales) by the end of 2025 and “considering all strategic options” for its Mead

Johnson Nutrition operations (16% of sales). The remaining business (“new Reckitt”)

should have a compelling - clearly top quartile, earnings growth model (see here) owing

to: a) its above industry average LFL sales growth (7% LFL between 2018-23); b) simpler

& more agile structure (11 PowerBrands generating more than 80% of sales, new

organization); c) elevated gross margin (61%) and operating margin (>24%) both well

ahead of US peers; d) a fixed cost optimisation program which should yield £450m in

savings over the next 3.5 years and allow higher investments and offset any potential

dis-synergies arising from future asset disposals; and e) management commitment to

“returning surplus cash to shareholders, including excess proceeds from future

transactions” - while also signalling the low likelihood of medium to large size deals.

Short term benefit: current valuation anomaly finally addressed

We would acknowledge that Reckitt’s new plan will take time before being fully

completed and comes with several areas of risks and uncertainties - including the

potential disruptions caused by the portfolio and organisation reshuffle as well as the

value of the Essential Home and Mead Johnson Nutrition businesses. That said, the main

merit of yesterday’s announcement is that it is actively addressing Reckitt’s depressed

valuation by forcing the market to look at its sum of the parts (SOTP); indeed, our own

SOTP, which bakes in quite conservative assumptions for the non core assets, evidences

an unwarranted and exaggerated discount for new Reckitt relative to peers (see here).

Tornado impact reducing 2024 EPS by 1% but 2025 EPS unchanged

We have lowered our 2024 LFL sales growth forecast to +1.6% (vs. company’s guidance

of +1% to +3%) chiefly due to our more cautious forecast for Nutrition (-10% for FY24)

as a recent tornado has considerably disrupted the business’ supply chain - and will likely

shave off £150m of the group’s sales in Q3. For Health & Hygiene, we model +3.9% LFL

(was 4.5% previously) on account of slightly more intense promotional activities than

initially anticipated. Our FY24 margin forecast remains unchanged at 23.4% (+30bps

yoy). All in all, our 2024E EPS comes down by 1% to 321p but our FY25E EPS remains

unchanged at 362p. PT unchanged as a result.

Valuation: Shares on 12x 2025E P/E, a c50% discount to US peers"

Why not look just choose from the dividend aristocrats list? I used to work for one and had RSUs, it was nice seeing the dividend come in Dividend Aristocrats | Nasdaq

Anyone experienced with getting the Quellensteuer back from some of those European dividend payers?

I’ve recently become interested in some French and German ones, but it seems like it’s a pain in the butt to get the tax at source back even with Switzerland having tax treaties in place with those countries.

I sent my first request to get back taxes from Sweden. I might get news in the next months. I hope it goes well as I have now 6 swedish companies. For the french tax, I haven’t even try, but I only have 1 company.

Reckitt stock surges after US jury rejects claims against infant formula

Shares in Reckitt jumped 10 per cent on Friday after a US jury rejected claims that one of its infant formulas caused life-long injuries in a baby, the first positive outcome for the group in what has become a widespread litigation.

The claimants in St Louis, Missouri, were seeking $6bn of damages from Reckitt and US formula maker Abbott, in a rare joint trial of two corporate giants. Four further trials brought by parents of premature infants are scheduled for next year.

Shares in the London-listed consumer goods group fell to a decade low this year after two separate juries found against Reckitt and Abbott.

Reckitt is seeking to sell its US formula business, Mead Johnson, in a wide-ranging restructure.

Still got no money back from Sweden in a year. I don’t know where it failed because for Sweden you have to send it to our tax office and then it get sent to Sweden. I was waiting for the money from my 2023 dividend before making the demand for my 2024 dividend

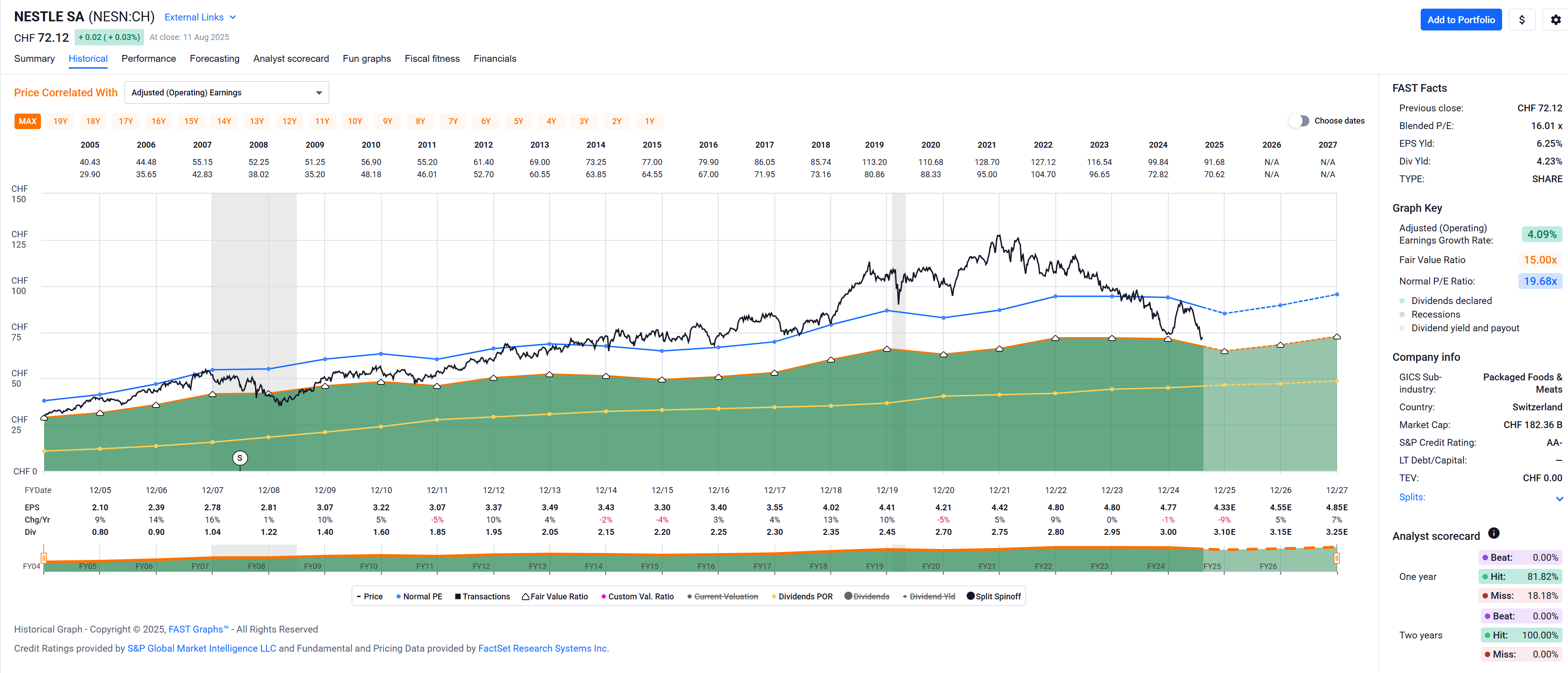

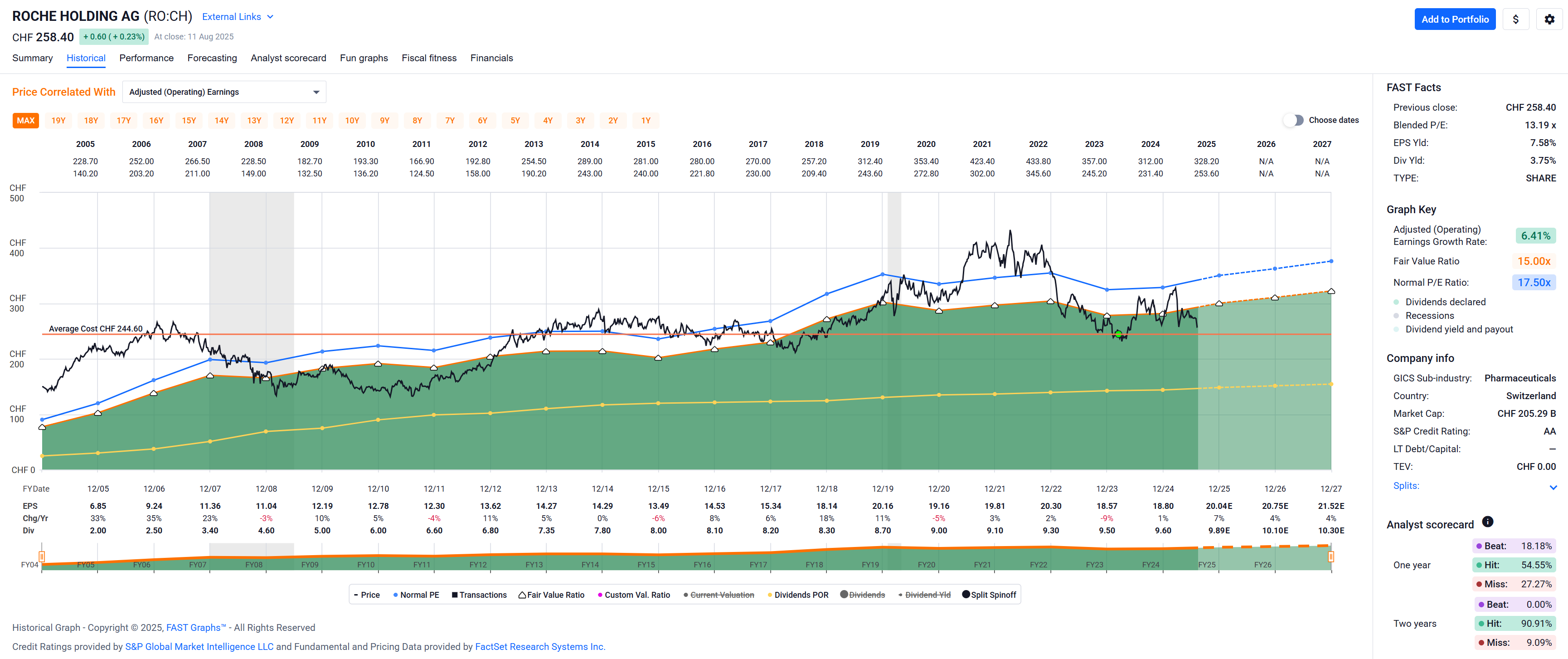

I shifted so much of my portfolio to high dividend yield stocks (and have also had to rotate due to written covered call options being triggered) and still my overall portfolio is at a record high. Crazy market but I hope it continues! I’m starting to look at some quality (and solid yield) Swiss stocks which may have been beaten up due to tariff nonsense (Novartis, Roche, Nestle) - nothing (also not the tariffs) will last forever and there may be an opportunity there. I have put options written on all 3 so happy to collect the premium even if I don’t wind up getting the stock.

What’s on your Swiss high yield watch list with your finger on the trigger?

Certainly one that might be attractive to be writing Puts on. I keep getting attracted to it, but I kind of dislike their anemic earnings growth history over the past two decades (although, seemingly, the next couple of years seem to look better).

Bought it in my son’s portfolio a year ago or so, but the growth story isn’t entirely convincing, either. Their multiple has been just as bad even without the Orange Mad King.

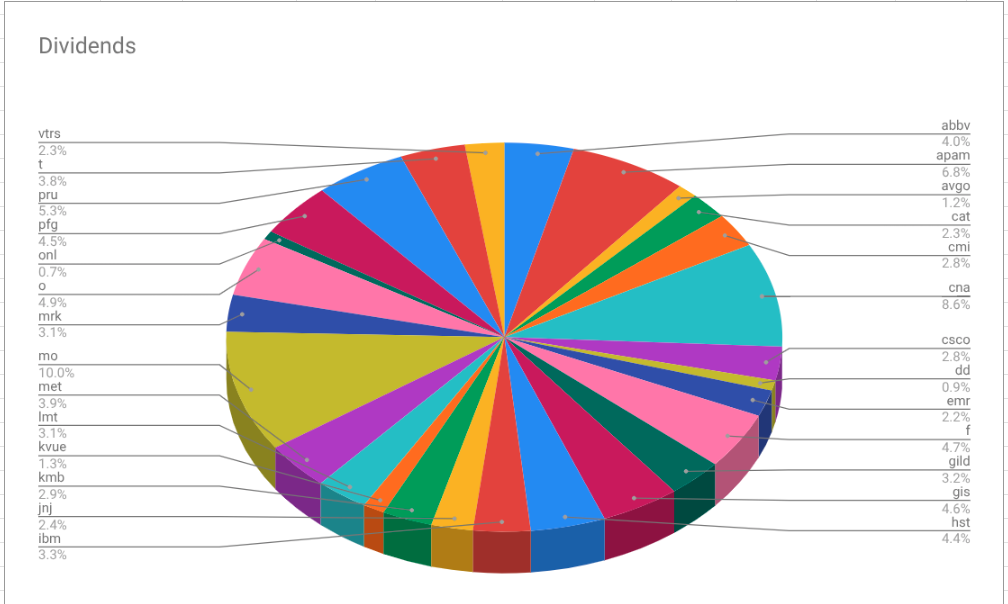

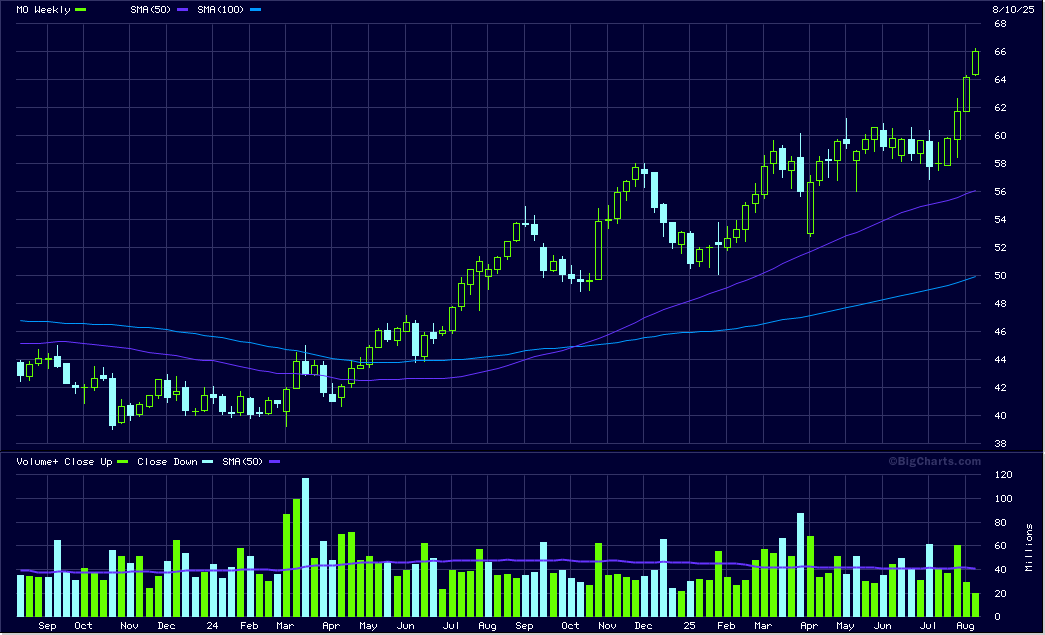

CNA pays a special dividend in February, so I still don’k know if this number is correct. But my all-time favorite is Altria Group (Philipp Morris), just beautiful:

It was undervalued for a long time being an out of favour non-ESG stock. Combine that with it slowly paying off debt and digesting an acquisition as well as some (perhaps undeserved) optimism on future smoke-free products had the stock return to value.

IMO, it was such as ‘sure bet’ that it was 40% of my portfolio at one time, before I became more disciplined and capped position sizes to reduce idiosyncratic risk.

Altria and PM were once the same company but they split some time ago on geographic lines (to ring-fence US liabilities).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.