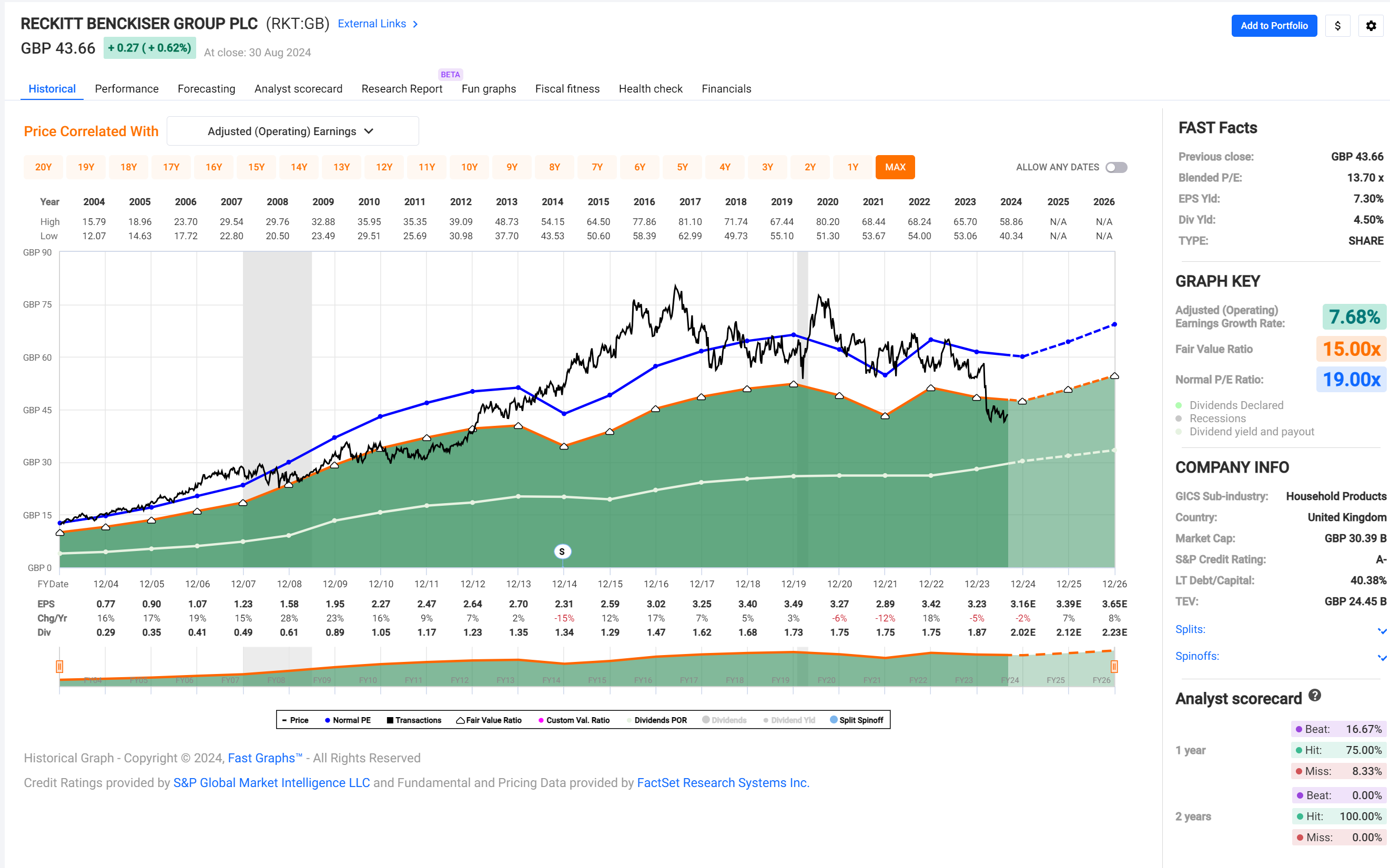

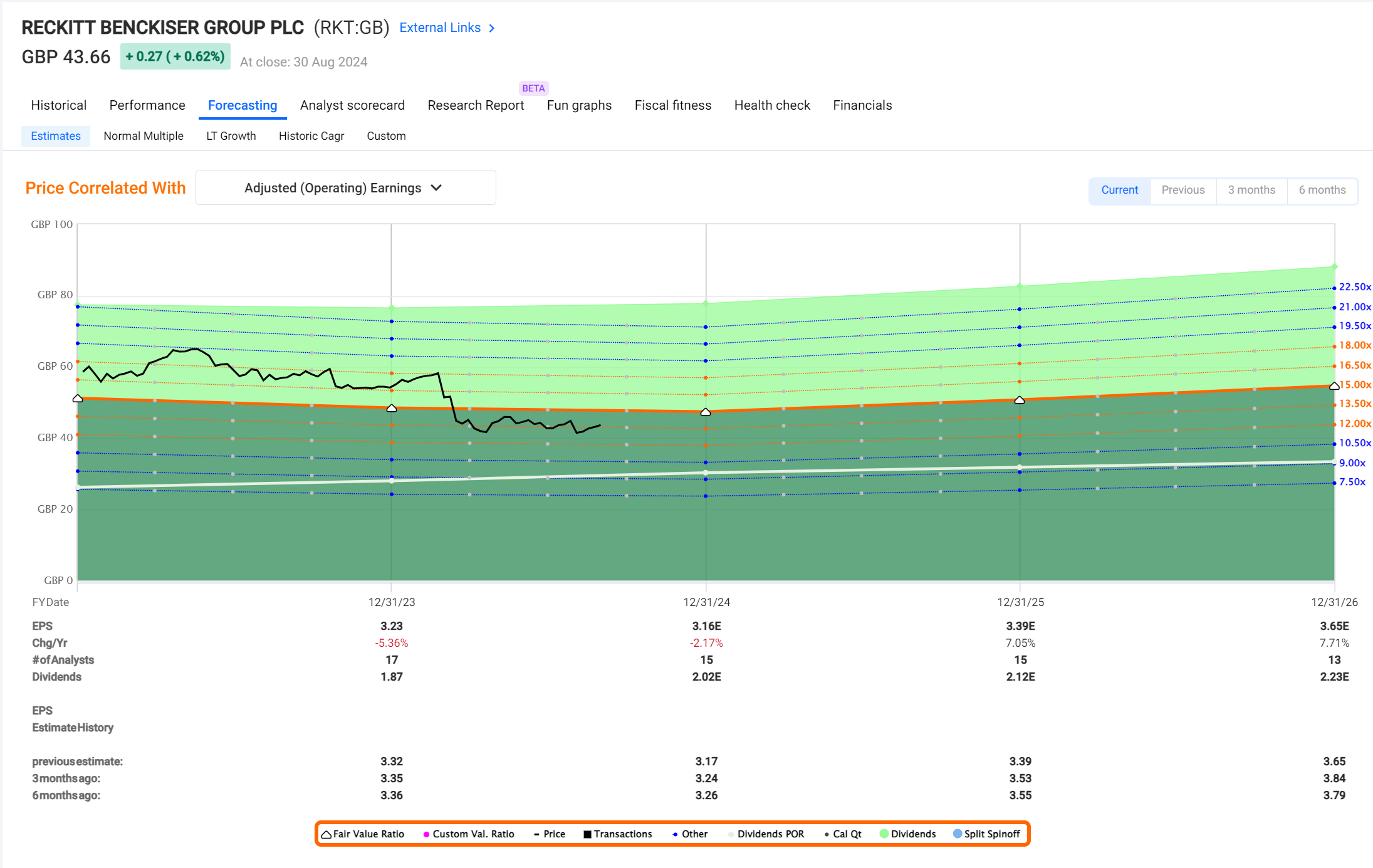

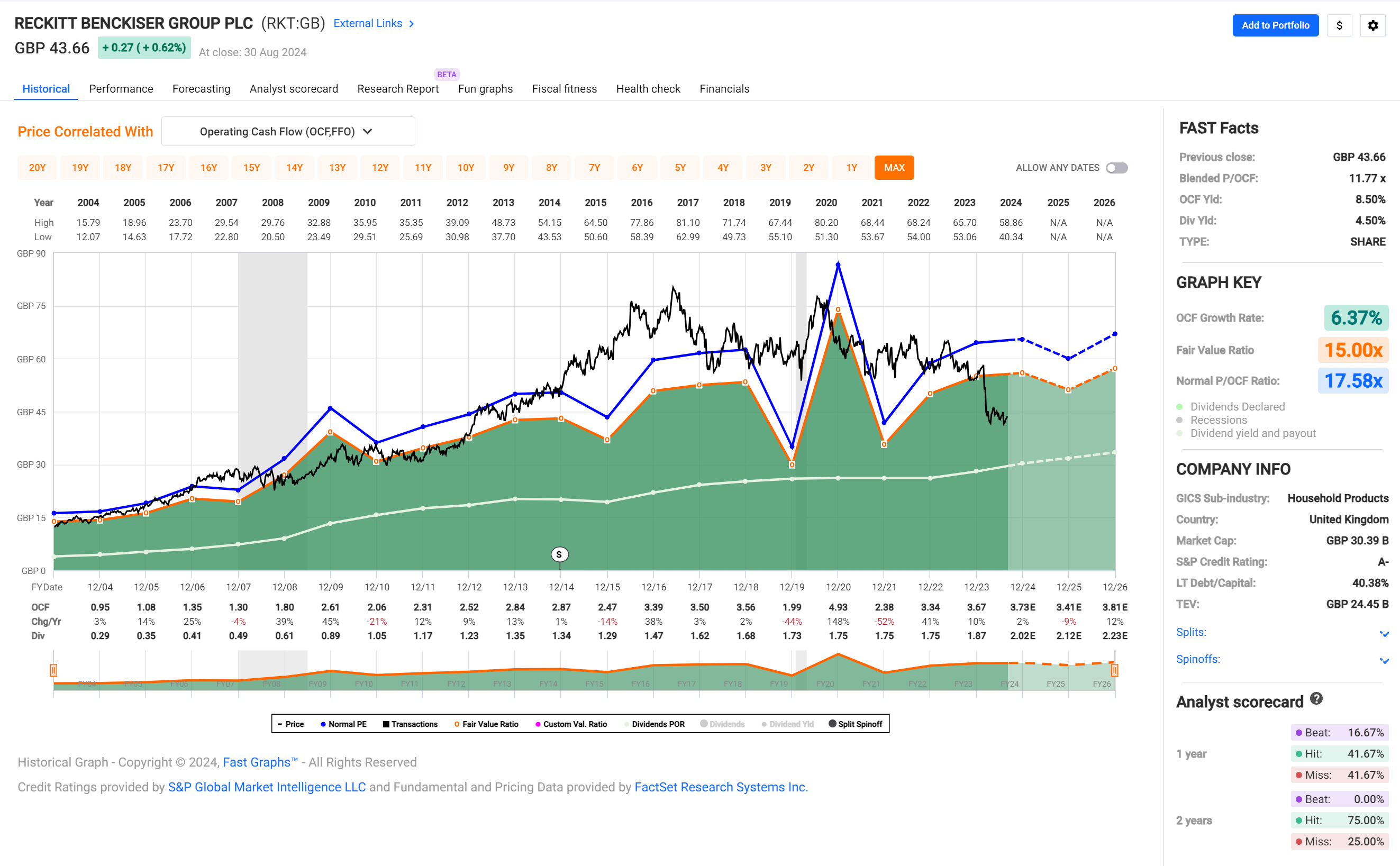

Reckitt Benckiser looks fairly interesting from a valuation perspective and is indeed also on my watchlist.

Growing earnings (mostly), growing dividends (mostly), great credit rating and an earnings yield of 7.3%. If anything, maybe a bit high on long term debt and a fairly high (but seemingly sustainable) dividend payout ratio.

The other ones aren’t my cup of tea. In short: too unsteady.

I just today started going through my watchlist again and these popped up for a closer look:

I love the idea of dividends, and dividend growth investing. Caveat I’m not implementing it because it’s not the time, but will do in time.

And some musing: it’s been a favourite of dividend youtubers to talk about Yield on Cost, their key exhibit is Buffett’s KO investment, at ~50% Yield on Cost. They say “It pays him his money back every two years without doing anything!!!1”. While impressive at first glance, having spent some time thinking it through…it’s more than anything a feelgood “metric”, isn’t it? Like telling yourself “Dang boy that was a smart move”, but not really impactful in terms of growing your capital…which circles back to the idea that dividends can be great, but not a way to aggressively grow your capital. /musings end

Agree - the “yield on cost” point is just plain BS as far as I am concerned. It ignores how long it took to get you there as well as the alternatives (opportunity cost) which you may have missed.

In my view , during accumulation phase, for a Swiss investor it shouldn’t matter if the returns from the equity investment is generated via dividends or capital appreciation. In the end total post tax return matters.

I often hear that people want to build dividend portfolios. But it only helps if you need to use the dividend income on recurring basis. Otherwise the goal should be to build a best post tax return portfolio which can maximise the capital at the end of capital accumulation phase.

Everything else like Return on cost , dividend yield is just like marketing gimmicks and doesn’t really impact CH investors.

During consumption phase / withdrawals -: perhaps dividends might be more useful as they can protect investors against sequence of returns risk. But even that I am not completely sure is data driven or not.

Reason being there is no tax on gains anyways. So selling 4% of your portfolio per year should be better than 4% dividends in terms of taxation. Not sure how much of it gets compensated with sequence of return risk.

I agree with @Mirager – “it’s a feelgood ‘metric’” – and I like the nuanced view as expressed by @Abs_max.

Personally, I enjoy gloating over some of my yields on cost.

When you then also look at the current yield of such high yield-on-cost investments, you can use it as a signal to sell (or buy more) taking into account the fundamentals.

Agree. I never calculate this as it is meaningless. In my daily spreadsheets, I don’t even show purchase price nor calculate gain or loss on positions to avoid anchoring bias.

I think dividend yield is a useful metric as you can compare it to the yield on treasuries to benchmark and ask yourself the question how much premium do you earn, what are the other benefits of holding stock and do these sufficiently outweigh the risk above Treasuries that you are taking on.

I see quality (high) div yield stocks as a part of my diversification as often (but not always) these are stocks which will be hammered less in case of a crash. The sweet spot of course is high-ish yield, low payout AND potential for earnings growth and multiple expansion. We’re all searching the holy grail:)

Apple’s a nice one: growth + yield (which appears low but that’s partially due to the PE rewarding the growth) AND substantial share buybacks

One of the things I like about high div yield stocks is that a drop in the share price actually is an opportunity to buy MORE and further fuel the yield.

But this was on sale between $28-$29 with a 10% dividend yield.

This was 40% of my portfolio, before I told myself this was stupid concentration risk no matter how bullish I was on it and made myself sell down half of it (giving up around 27% capital gains since selling on top of the lost dividends).

Nice responses, it’s nice to have an intelligent conversation away from the “dividends are iRrElEv4nT” nonsense and the “but muh no captial gainz tax3s” toxicity.

As usual @Abs_max writing is perfect pitch!

Agree, was going to somewhat disagree but the last sentence caveat saved it. Just need to say that from the handful of people I know who actually live off their investments there’s not a single one without a sizeable (>60%) part of their NW in income-generating instruments, be it dividends, real estate, even bonds and CDs. Not one. And not one is fond of selling anything, ever, either.

Hmmm, I doubt it matters whether one is in CH or not, and dividend yield is an important metric open to a ton of abuse and misunderstanding. I am sure you know of the concept of “yield trap”, ie buying into a company just because of having a huge yield, and missing the point that it’s yield went up was because the stock got seriously hammered, like Bayer. Someone buying into anything based on yield % could end up with shitty companies just about to die, or at the very least cut their dividends. There’s research showing dividend initiators and growers overperform the market, while dividend cutters underperform.

Totally agree on the sequence of returns risk point in the first sentence, and doubt any sort of data would help much. If one doesn’t ever sell then paper gains and losses are just that, on paper, while cash is real, and if you’re in the enviable position to live off your dividends then you have a huge buffer of protection from sequence of returns risk, downturns and can wait things out.

On the second sentence is where I get upset with the dividend-hating zealots, either here or on reddit, as I feel they miss the human element in all of this. Some people may never want to sell, and may not be looking for the absolute “best” performance. In fact I believe that there are as many versions of “best” as there are people on earth. Remember that selling is an act of market timing, which we’re supposed to consider a bad thing that nuhbody can ever do etc. I can totally see the human element in not wanting to sell, even for seasoned investors. In particular if a stock or index fund is on a tear and is going up…they’ll get thoughts about opportunity cost.

I am not necessarily against dividends. In fact I like the dividends from my VT portfolio. I also think that dividends are useful in case the investor migrate out of CH because then it might be worthwhile to avoid capital gains tax as much as possible

The main point I am stressing in general is that dividend by itself doesn’t make an investment good from financial perspective. What really matters is what the needs of the investor are at the point of time and what the overall return one can get from the investment.

Zurich (ZURN) still yields above 5%. I bought it for my son’s portfolio on a dip in April this year when the yield on cost … , er, never mind.

Would you consider Zurich a high risk position?

AA credit rating, 34% long term debt / capital, a bit cyclical in earnings and mostly steady and growing in dividends; overall steady earnings growth rate of about 5%.

High payout ratio, I’ll give you that … but then again, I’m not sure they – as a multiline insurance business – have lots of avenues for better capital allocation?

Admittedly, there’s not many Swiss companies with high yields that I would put my money in.

Since I am not very much into individual stock valuation, it’s tough to say if the stock is currently over priced or underpriced.

But overall the stock has performed decently over the last 5 years and even outperformed the SMI. So I would say unless someone bought during the 1999 period, this particular company has been a good investment

The good thing about 5% dividends is that if the company manage to stick around for 20 years then the money would be back no matter what

I was tempted to buy into Roche at 220 CHF just to test this theory. But then I realized that SPI already have a lot of Roche so didn’t want to extend the exposure. Post that stock rallied anyways and would have been great investment.

Roche is the other position I dipped my son’s portfolio feet into in March this year …

He has no* index exposure, so I’m not bothered by Roche making up lots of the SMI/SPI.

* Ok, he has no Swiss index exposure, but owns VOO and VXUS bought at the the-world-is-ending time of the COVID crisis in early 2020. Bought them mostly for educational purposes that the rumors of the world ending were much exaggerated.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.