According to ZKB Pensionskassen-Monitor the average net performance for 2025 was 5.3%.

So 5.2% till Nov wasn’t that measly. ![]()

1 Like

And considerig that pension funds have to invest conservative. 5.2% return in such a year is pretty good actually.

3 Likes

Can’t wait for Profond to release their numbers

Any Day Now

Yeah same, I assume 4% or less (otherwise pretty reckless when you see most pension fund delivering 4-5%+ have > 115% reserve)

2 Likes

Btw anyone with profond for more than a year?

(I only had a partial year so not entirely sure about the rules and if it differs)

I did receive a pension certificate for january, with a 2.25% interest for 2025.

If so it reinforce my opinion of the fund, they went for headline grabbing return rather than stability (at 6% last year they’d probably have still claimed their title of best return over 5y period, 8% seemed wild if you’re not at 130% reserve already).

- 2025: 3.25%

- 2026: 4%

- Funding ratio at 115%.

2 Likes

Same for me:

Die Verzinsung für das Altersguthaben im Jahr 2025 beträgt 2.25% (BVG-Anteil 1.25%)

For 2024 it was:

Die Verzinsung für das Altersguthaben im Jahr 2024 beträgt 8.00% (BVG-Anteil 1.25%)

Do you find any explanation for large difference between 2024 and 2025?

They distributed most of their return in 2024 instead of building up reserve (imo the goal of a pension fund is to smooth returns, otherwise it’s like a 1e but worse, but I can’t make sense of their reserve strategy).

So they started 2025 with less reserve and more international (US) exposure than their peers.

3 Likes

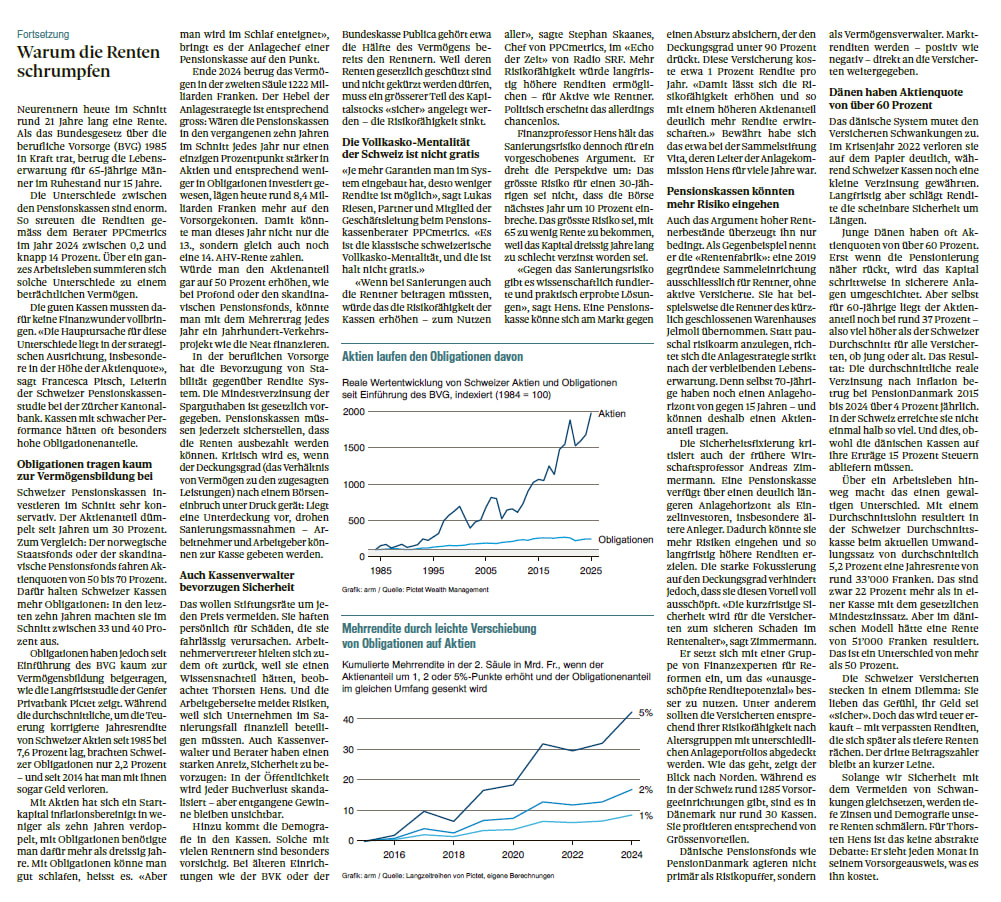

Here’s an article in German on the way pension funds invest and let members participate (or not).

summary: Swiss pension funds prioritize stability over returns, investing conservatively in bonds rather than high-performing stocks. This “safety-first” mentality reduces long-term growth. Experts suggest that adopting riskier strategies, like Denmark’s, could increase retirement pensions by over 50%.

edit: source Sonntagszeitung 11.01.2026

1 Like

They have a Funding ratio of 111.1% per 30.11.2025, which looks find to me. Or how much would you expect for a pension fund to be healthy? (I have no idea)

But yes, the interest paid over the last 10 years has varied greatly:

| Year | Fund Return | Interest paid |

|---|---|---|

| 2025 | unknown | 2.25% |

| 2024 | 9.8% | 8% |

| 2023 | 4.6% | 2.25% |

| 2022 | -8.4% | 2.2% |

| 2021 | 12.8% | 8% |

| 2020 | 2.7% | 1.75 |

| 2019 | 13.5% | 3.5% |

| 2018 | -4.2% | 1.5% |

| 2017 | 11.3% | 3.5% |

| 2026 | 3.7% | 1.25% ] |

Source: https://www.profond.ch/kennzahlen

But I don’t know if that’s a bad thing… What’s much more important to me is good performance over time and downside protection.

4 Likes

If they’re 111% now, imagine how close to 100% they were in April.

From what I’ve seen, the funds that distribute most of their return tend to have at least 115% (but often 120%).

I like when fund publish the rules for computing returns, e.g. axa professional invest has a formula like (CR = coverage ratio):

| Level | Funding Ratio | Interest Formula |

|---|---|---|

| 7 | ≥ 120.00% | 4.50% + 50% × (CR − 120%) |

| 6 | ≥ 117.50% | 3.25% + 25% × (CR − 115%) |

| 5 | ≥ 115.00% | 3.25% |

7 Likes

It’s actually in the interest of the open-ended pension fund to stay close to 100%. New entrants bring new money, but you cannot ask them to bring 111%. Companies leaving only get 100%, not the extra reserves, so they wouldn’t be happy to have too much reserves either.

1 Like

I have 2 second pillars (because reasons), Nest gave me 3 %, Axa (Columna Sammelstiftung) gave me 2.25 %. Last year was not bad either, but Profond and some others are way ahead.

I wonder if that’s necessary, though? It could also reduce retirement pensions by 50%, and then there’s hell to pay, mostly for retirees. I feel that in CH, with tax-free capital gains, it makes sense to have conservative pension funds beating inflation (in CHF), rather than chasing for returns.

1 Like

I’m afraid this does might compute mathematically: if pension fund contributions of employee and employer were combined 15% of salary, you would end up after 44 years of work (× 15%) with 6.6 years’ of salary. Maybe you spend less and can survive with less, but your life expectancy at this point is another 20 years.

We (as a society with a median salary of ~7k per month) absolutely need to do more than just beat inflation!

1 Like

Hmmm, yes, you sound right. It hits on the Ponzi aspect of pension funds.

There is also the option to reduce the current length of the retirement to, say, 15 years, which is about where it was back in 1985, when BVG came into force.

(used to be 11 years in 1948, when AHV came into force)

In other words: If we want the reward of higher returns, we (everybody) also need to be able to take the risks, which could mean no more “guaranteed” annuity for retirees, but a flexible one.

1 Like

Life expectancy is around 85 for men at retirement age.

Yeah, it’s bad to be in a fund that’s getting a lot of new members.

But is it actually true? At the individual level yes, but would have assume a company leaving might have a claim on some of the reserve? (Esp since they might be ask to pay for missing reserve if they’re leaving with reserve <100%). But I didn’t look in details.

(Definitely the best setup is a stable/big company with their own fund and some aggressive Investment with a not too generous pension conversion)