I’m deep in this topic of rent vs buying. For a simplification, let’s assume for my situation renting for the same object is 2k/month whilst my calculated total cost of ownership (all inclusive, including opportunity cost of initial capital¬ary fee, 2% mortgage, tax implications etc) is 3k/month.

This means that if I rent, I can actually increase my nest egg of 12k yearly for the same cost of home ownership, compounding at 7% over 30 years in an ETF.

How do I translate that to a final additional monthly opportunity cost which goes on top of the 3k for the final true cost of ownership? Which formula do I use?

12k per year at 7% for 30 years, second year an additional 12k 7% but only for 29 years etc.

Do I calculate the total additional nest egg in 30 years and divide by 12*30? Seems crude, but could be effective.

I think you can keep it simple. Let’s say investment horizon is 30 years. I am going to completely ignore wealth taxes etc .

Option 1 -: you rent the property for 2K per month and invest the 1K into an investment plan which yield 4-5% return on annualised basis. I wouldn’t assume 7% because that is not so standard in CHF terms. Your final value of the investment plan can be calculated using following calculator

In your example , 1K invested over 360 months (30 years) with annual return of 5% will end up with 835K CHF. With 7% it would be 1.22 Million CHF.

Option 2 -: you own the property and your cost is 3K per month. I am assuming you have included all that needs to be included. However at the end of 30 years the property will also be worth more than what it is worth today. Your final value will be (Property worth at end - mortgage value at end)

For example 1.5 million CHF apartment with 2% annual gain over 30 years would result in 2.7 million CHF in value.

So this comes down to your assumptions. You never know how the world with move in future. Sometimes real estate can also have very significant returns because of the leverage potential. Real estate investments of course depend a lot of other factors like location, economic situation and demographics.

P.S -: in the calculator, SIP means Systematic investment plan. It’s just a fancy acronym to say that you will invest monthly.

In the end it’s all impacted by two “knobs”:

choosing the rate of return on real-estate and the return on stock ETF.

Since 2013, my IB account invested mainly on VT returned XIRR of 10.13%. Subtracting inflation and so on, makes my assumption of 7% I think realistic. But I can tune it down to 5% or 6% to have a “worst case scenario” for renting.

On the other hand, I’m not convinced about real estate. There is a concrete upper limit to home price which is the affordability calculation of median salary + 20% initial deposit. A “standard” home that should go to middle class family, cannot continue to increase indefinitely at 2% from today prices…

The price shouldn’t be higher than what people can afford to buy, right? Even if home owners will only be the upper class and no longer middle class, there should be a way to estimate the “median upper class salary” in 30 years, and from that retrieve max mortgage and monthly payment as per affordability, plus ability to save the initial deposit, and see what would be the home prices in 30 years…and backcalculate the CAGR.

So basically instead of backwards looking to real estate returns in the past 30 years, and apply the same logic, I think we should extrapolating from salary evolution and affordability calculation

As you said, it’s all about assumptions.

It’s really tough to forecast next 30 years.

Past is not reflective of future real estate returns but same is true for stock markets. From my perspective , all I wanted to share was that assumptions matter. That’s all.

Real estate is more complex and concentrated though and also illiquid. I prefer stocks as well for this reason.

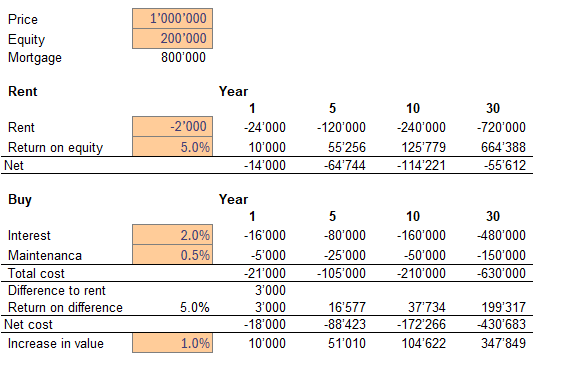

I compared rent with cost of buying for several time periods. Only then added opportunity cost.

A monthly comparison then doesn’t seem helpful to me, as the opportunity cost will increase exponentially over time.

If you assume historical returns of stock markets, why not historical price increases on homes? Although, I doubt most owners think in terms of returns for their property.

The comparison is so sensitive to expected returns on opportunity cost, inflation, interest rates that I ignored one-time cost, additional amortization, assumptions on increasing maintenance over time etc.

If that helps, it’s sometimes easier to see that outside of the context of renting vs buying.

If you own a place you’re kinda paying a rent to yourself, and you can figure out what the approximate net yield is, based e.g. on how much you’d be able to charge someone to rent the place (after charges and maintenance costs).

Then you can compare this investment to other (potentially leveraged) investments (incl. diversified leveraged RE fund, equity, etc.).

Fair enough, but I don’t consider personal property as an investment or in terms of yield. Especially when not comparing apples to apples.

I might as well add a line in the table labelled “personal satisfaction: priceless”

It is very important to consider all the financial aspects, it seems all the answers here agree on that. And that’s how I read OP’s questions, but it might as well have been from a theoretical standpoint.

Yet even from a pure financial perspective, to me there’s just too many variables to simulate over 10, 20, or 30 years and then condense it into a monthly cost.

So on this specific topic, if you can afford to buy, to me eventually it’s not about a precise comparison, but also a less rational whether you want to, or not

Haha, they basically had almost the same points, even similar dummy numbers

Maybe the perspective on the conclusion differs

Based on the file, you could even add the basis of the Eigenmietwert, consider that amortization could be (partly) done indirectly, tax effects of bigger renovations, using pillar 2 to amortize based on interest rates and what not.

Won’t add much to precision or decision making, I guess.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.