I understand the main concepts of the mortgage (2 tranches, one is 15% of the value, the other the remainder, SARON is variable rate, fixed is locked for the duration the contract, mind the duration to avoid being locked in…) and my assessment is the following:

If we bring the bare minimum of 20%, we would need a mortgage 880k CHF. The second rank mortgage would be 132k CHF, the first rank would be 748k CHF. We are petty risk averse so we would like to have direct amortization at fixed rate locked in for 10 years.

Would there by any reason to

Have third tranche on the mortgage ? If so, what would be the rationale and maths behind it ?

Have a trench at 5 years and another 10 years (as we could renegotiate the whole thing at 10 years) ?

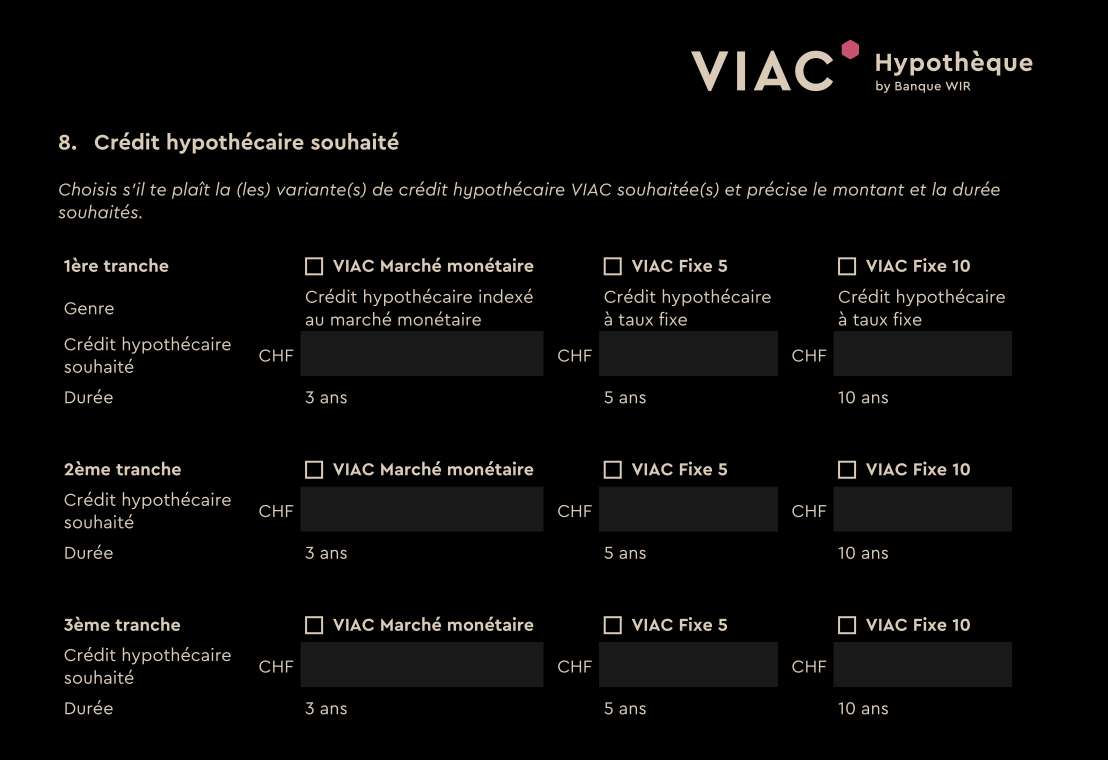

These would be first and second mortgage, you call them “ranks”. Tranches are separate debts with different durations, i.e. SARON, 5 years fixed, 10 years fixed, etc.

The division onto 1st and 2nd hypotheke is more a legal thing and is not important in practice. Most mortgage providers will give you the same conditions for both (?).

The division to tranches is more important.

If you are not sure, take only one tranche covering both parts of the mortgage.

As I understand their offers, you can’t have a 5y SARON with them. Their SARON (money market) duration is 3 years, that makes it difficult to match the maturity of the tranches between fixed and SARON.

I would check with them if the SARON can be repaid at any time or if they prevent full amortization (but offer flexible partial amortization, or no discretional amortization at all) during the 3 years. If they don’t allow for full repayment, I would not mix and match tranches with non-compatible maturities as that makes difficult to change bank and/or negociate as the whole mortgage could not be moved together.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.