I am planning to split my current portfolio in two.

30% value investing mutual funds

70% permanent portfolio

I would like to reuse my 15% VIAC global 100 as permanent portfolio “stock” quarter. Even VIAC global 100 is “global”, it has a strong geographically CH bias, it has 37% in Switzerland. To fulfill the stock part of the permanent portfolio I will need to buy a little of ETFs in Interactive Brocker, I could buy some ETF that excludes Switzerland. So I reduce the CH bias.

Do you think this VIAC reuse in a permanent portfolio may be convenient?

Why do you need a permanent portfolio? Are you retired and live off your money?

you should use 3rd pillar stock funds to overweight geographic segments with the highest dividend yield. These are Pacific, Japan, Europe, and Switzerland.

Surely you should treat all your brokerage accounts etc. as one common portfolio.

Are we speaking of Harry Browne’s Permanent Portfolio of 25% stocks, 25% long term bonds, 25% short term bills/cash and 25% gold or something else?

What is your target allocation?

Edit: provided I have understood correctly that you want to use your VIAC account for stocks only, as part of the stocks allocation of your permanent portfolio, you can use the CSIF SMI, CSIF SPI Extra, CSIF World ex CH - Pension Fund Plus, CSIF World ex CH Small Cap - Pension Fund and CSIF Emerging markets funds to build up a worldwide cap weighted allocation, or tilt it in the ways you want with potentially other funds.

Edit2: @Dr.PI has made an awesome job of figuring out the best use of 3a space taxwise in regards to geographical areas. If you’re going to invest stocks in 3a and in taxable, you could use that: Splitting the world

I have my value investing mutual funds for 7 years now. I like their managers, and I would like to keep them by buy & hold.

Mainly since I moved to Switzerland 5 years ago, I have just invested every year only the 6.8K through VIAC global 100.

For reasons unrelated to investment market, since I am in Switzerland mainly I have done no other investment than these 3rd pillars full in stocks. So I have piled up quite a lot of cash.

Today my portfolio looks like:

30% value investing mutual funds

15% Viac global 100 (stocks)

55% cash

This 55% in cash is valued in 200K CHF. It ends in a bitter pill to swallow. In the past I used to do dollar-cost averaging in my value-investing mutual funds to just avoid my current problem. Piling up to much cash and being afraid to move in stock.

As I wouldn’t feel comfortable investing this 200K CHF in stock at once, I thought to implement a permanent portfolio (Harry Browne) as a sub-portfolio by merging 15% VIAC-global-100 and 55% cash.

I don’t think would be a good idea to use my value-investing mutual funds in the permanent portfolio as they are very contrarian. They could not perform as expected stocks by Harry Browne.

If I could reuse the VIAC 3rd pillar as permanent portfolio stocks quarter. I would just need to buy 0.15% of bond-ETF, and 0.15% gold (Bullion Vault). Ending with sth similar to:

30% value investing mutual funds

70% permanent portfolio

– 15% VIAC stocks

– 15% gold - Bullian Vault

– 15% long term bond ETF.

– 15% cash

Probably I don’t need a permanent portfolio. I don’t plan to retire very soon. No sooner than 5 year. But my concerns are that I am afraid to put in risk this 200K. The market seems to be very overpriced after this central banks stimulus, and a bear market might be coming.

@Dr.PI I have to analyze in deep your 2nd point - “overweight geographic segments with the highest dividend yield”

I’m neutral on that (and mainly wanted to make sure I had understood what your idea was), a good allocation is an allocation that allows for you to reach your financial goals while also sleeping soundly at night. It sounds like this one might and it’s certainly within Benjamin Graham’s 75/25 rule (never have less than 25%, nor more than 75% in stocks). I like the permanent portfolio, though I’m not a fan of bonds under the current circumstances, but both of these are personal.

Maybe, maybe tomorrow starta the biggest rally in stocks ever, no one knows. What you describe is timing the market, like this you will never invest your money, because you stand on the sideline and ask yourself when the right time is to invest it.

When do you invest it again? When the market rises again? But maybe it was just a small rebound and will fall even harder.

What I want to say is, time in the market beats timing the market.

Remember the financial crisis in 2008? Shortly after in 2009 was the largest rebound ever and you could easily double your investment in less than a year.

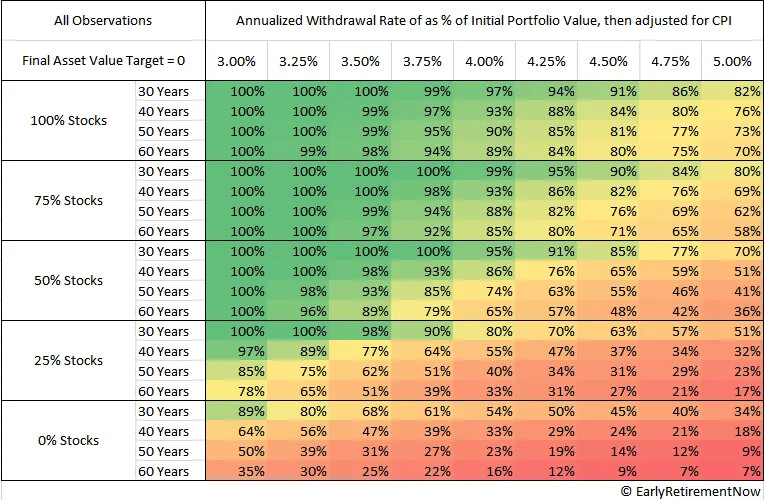

5 years would be a relatively short investing horizon, so would warrant the conservative approach. A 40/60 portfolio diversified globally has come awfully close to reaching negative returns on a 5 years period during the GFC (2007-8) in nominal dollars terms (so not that relevant to Swiss investors, that’s just to illustrate the risk level and appropriate investing horizon for the portfolio): All Country World 40/60 Portfolio: Rolling Returns (time series considered since 1995).

That’s probably not a problem if you keep investing and have some flexibility (1-2 years) regarding when you actually retire or your level of expenses in retirement.

Once retirement is reached, a lower stock allocation can warrant a lower Safe Withdrawal Rate (other withdrawal methods can be used but exposure to the Sequence of Returns Risk (SORR) would probably be similar).

So I’d want enough stocks to reach my target while still being comfortable with it, then adjust my withdrawing expectations accordingly. If your plan does it for you, then you’re set (otherwise, adjust accordingly).

Indeed, but if we have to use our second pillar to rebalance, doesn’t that mean that our allocation would actually call for us to have less bonds, but that we can’t do that because we can’t sell our second pillar?

Having bonds outside of that allocation wouldn’t change that. If I want to be 90% stocks, but have to have 20% of my assets in my second pillar, then I am just 80% stocks and have to be content with that. Sure, I loose the ability to rebalance but I don’t need to rebalance into stocks if I have already as much stocks as I possibly can.

I am totally newbie in bonds. I have to research a lot about this topic.

Probably I will choose 20+ years bonds ETF from USA and Germany.

If central banks raise the interest rates the other assets in permanent portfolio (gold, cash, stocks) should hedge it.

We can neither forecast where the rates will be in 5 years, they might be lower than now, they might be very negative, and bonds should work well in deflationary market.

What you describe is timing the market, like this you will never invest your money, because you stand on the sideline and ask yourself when the right time is to invest it.

I believe what I am planning isn’t market timing. I need to allocate now 200K CHF. I could choose 100% stocks, but I will not sleep soundly at night. Otherwise I could invest this cash based on permanent portfolio, which has lower drop down of 100% stocks, and stick with it. I don’t plan to rebalance to 100% stocks when I will have the right gut feeling.

Even I don’t plan to touch my current 30% portfolio of value-investing-funds. I will be still invested in them.

I agree with you market timing strategy in long term does not work.

The 2nd pillar bond allocation would be a problem, just if we don’t have further bond assets in our portfolio (ie German 20+year ETF) that we could cash it.

If our portfolio bond allocation is built ie. 60% 2nd pillar bonds + 40% bond ETF. If bond allocation is overweight we can sell this 40%. Probably this 40% buffer might be enough for rebalancing.

Similarly approach with stocks. If we have VIAC + stock ETF rebalancing buffer. Besides in VIAC we can choose different strategies invested 20%, 40%, 60%, 80% and 100% (by now I am using only 100%)

I see, I think I misunderstood you. It sounded to me like you don’t want to go full sgocks now, because of overpriced mafkets, buy would do so if markets were not that overpriced.

I have just checked the asset allocation of my 2nd pillar. I was expecting mostly a pure bond strategy. However, it has a lot of stocks. It seems it attempts to achieve a strategy that just beats the inflation. Probably it has very low volatility.

Specifically bonds in Harry Browne permanent portfolio are long term (30-20 years) treasuries. Because they react very aggressive to the interest rate changes. I don’t think this 2nd pillar could achieve such behavior.

Probably this 2nd pillar might be use in Bogleheads portfolio as bond allocation.

You count your 2nd pillar as bonds, because they pay out a minimum required amount (currently 1%) no matter how their portfolio performed, like a coupon payment on a bond. Some 2nd pillars pay more in good years.

If your 2nd pillar would only invest in bonds, it would go bankrupt sooner or later, at current conditions rather sooner than later as they are required by law to pay out at least 1% to the employees. The excess return is used to pay pension to already retired persons and also to build reserves for bad years.

The allocation you showed is pretty standard (I work at a pension fund provider).

Swisscanto has more stocks than some other P2 providers, but it’s still a relatively conservative portfolio. As @Burningstone said: it’s a pretty standard P2 portfolio.

They need to have some stocks / real estate to be able to pay you the 1% minimum guarantee. When I had to chose a P2 provider in 2018, Profond had the highest ratio of stocks with 46%. I’m curious how this year is going to evolve in terms of stock markets, but if it goes sideways or slightly down, P2 providers with higher stock allocation might suffer more. In the last years during the bull run, they also made more money.

I wouldn’t compare P2 with a Harry Browne permanent portfolio. I think that the P2 fund managers know what they are doing, and they will not only rely on one portfolio recommendation.

Personally, I think Swisscanto is a pretty good P2 provider. When I decided to P2 provider, it was between Swisscanto and a different provider. Latter one made it due to larger total assets and some minor advantages.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.