How does the repayment schedule work? Is it over a fixed period?

The loan and the interest are payed from the liquidity in the account right? So it would be like a normal mortgage with the tricky bit that your asset are acting as collateral and the interest rate is relatively low unless the market goes crazy.

I am struggling to understand how the loan is payed.

The interest goes against your cash balance, how about the principal?

If you take the loan out to buy stocks I guess that as long as you meet the margin is OK and then when you liquidate the leveraged position you close the loan.

What happens to people like MMM that take out a loan to withdraw money and use it externally? How do they repay the principal part of the loan?

Either they never pay back the principal before the end of time, or they either get money from their account (dividends or sale) or they send back money to IB. They can of course be liquidated if they don’t meet the margin requirements

I think it’s faily simply. Depending on the portfolio you have I belive you can get up to a 1:2 margin, i.e. if you have 100K you can borrow up to 200K.

What is suggested by this is basically that you take a short position in USD, by withdrawing it (or whatever currency you choose).

You don’t need to repay anything as long as you don’t get a margin call (if your portfolio value decreases, you may get positions sold automatically to cover it). If not, you just keep paying interest to keep the borrowed cash (pretty much like a CH mortgage once you stop deducting the debt). Just make sure you don’t take too much of the margin like MMM did.

And looking here, seems this is available for :switzerland investors:

As other have said, there are no principal repayment requirements unless you reach the limit of the margin you are allowed. Be wary that your debt amount is fixed, aside from accruing interests, (say 100’000.-) but that, unlike a house, the value of your assets moves wildly. Your assets can loose half of their value overnight (well, not quite overnight but pretty quickly) so what could have been a 100% margin (100’000.- of debt, 100’000.- of assets) can become 200% (100’000.- of debt, 50’000.- of assets) without you doing a thing, resulting in a margin call.

If your margin is called, you’ll have a few days to cough up the difference in money. If you can’t, your assets are sold at their low price to get you back into “acceptable” margin territory. This can happen again and again if the price of your stocks keep falling.

Note that margin becomes dangerous when stock prices drop. Big stock price drops tend to happen when other bad things happen in society, meaning two things:

you could be out of a job, if you’ve loaned the money, the person you’ve loaned it to could not be able to repay it anymore, the value of your house could be reassessed (dangerous if you have a mortgage too), the value of your other assets may decrease too, making it a very bad time to sell anything. In short, you could be in financial troubles already ;

the situation may be too dire with too many people on margin so that the broker needs to adapt its margin requirements, either lowering the total margin available (you’d get called when you thought you were safe) or the interests due (your margin becomes suddenly unsustainable).

Margin loans are part of the things that go well as long as all goes well but can get really, really, really bad when things get bad. Apply caution. MMM is a very enthusiastic person and, in this case, writes in a genuinely reckless way without emphazing the consequences margin play can have. That he just discovered a tool that’s been there for ages may mean he hasn’t truly internalized what being margin called really means when you don’t have the money to meet the requirements. He, himself, has got the money, after all. Be wary if you’re not a multimilionnaire yourself and are borrowing more than you can repay in a blink.

I think as long as you keep the margin low (10-15% range) there won’t be any issues. So if you have 100k in assets, you could take a 10-15k margin loan and would only get margin called if the stock market drops by 85-90%. The global stock market never dropped that much. I don’t remember the exact numbers from 1929, but I think Swiss stocks dropped by 50% and something like VT (if it would have existed) by 65-70%.

As soon as I pass the 100k mark in IBKR, I will close my emergency cash fund and invest that in stocks too.

I’d feel relatively safe with a 10%-20% loan too but the concept makes way more sense, in my view, for a retired american person who pays capital gains on their stocks (which have considerably increased in value over time) than for a frugal swiss person in the accumulation phase who can cashflow most small needs (including raising a small amount of money to help friends) and wouldn’t pay capital gains by liquidating stocks when they need more.

Also, I’d not take a loan and keep a cash/bond allocation together (outside of the 2nd pillar), including no emergency fund. The two play the same purpose and can fail at the same time. If I’m not at ease with the concept of needing to request a margin loan in case of an emergency, I’d not be at ease with the concept of having one when that same emergency occurs. Margin loans are for highly risk tolerant profiles in my book (or specific strategies which are not the topic of this thread).

Yes, capital gain are an important part for US person to consider and margin loan help with liquidity without triggering taxes for them.

But I don’t agree with you that liquidating stocks is always feasible for a swiss person. I would not keep a consistent margin loan “active”, but it would actually make me sleep better to know that I can withdraw up to 15-20% in cash in a few hours without having to sell. Selling during a crash to cover some emergency or unexpected purchase can be devastating to your long term gains.

And here comes some considerations:

the market doesn’t crash 50% in one day. It may take 5-6 months. In that period, you can fasten your belt and go super saving mode to cover the margin loan you may have took out to avoid selling during a crash. If they fire you, you still can go super saving and there is arbeitslosigkeit versicherung.

If the market crash, the loan interest rate will go up for sure, but paradoxically your margin loan calling risk may come down. Let me explain my thoughts: if you need too much cash to be paying with your cash reserve, and the market has crashed 50% from all time high, instead of selling stocks you can open a relatively safe 10-20% margin loan because it is highly unlikely the market will crash again 80% AFTER crashing 50%.

If the market are at all time high, then if an emergency come, I would sell some stocks instead of taking out a margin loan. Because we don’t ahve capital gain taxes.

I have right now 15k in cash “losing” opportunity cost of 5% per year. And I have 210k on IB where 10% would be 21k.

I will test some things out, but if it works well I’m doing something with that 15k (maybe even dump it in my 2nd pillar to lower my taxable income and make 1% interest). I will not open actively a margin loan, but I will be sleeping better knowing I could use it just in case.

To me it makes sense even if you are Swiss, because the interest you pay on CHF is so low. I don’t see why the loan interest would go up in case of a crash. Anyway the reference rate is negative now so you still have some margin before it increases for CHF.

But if you take money out, it is obviously safer to keep it to a small share of the total portfolio like maximum 20%.

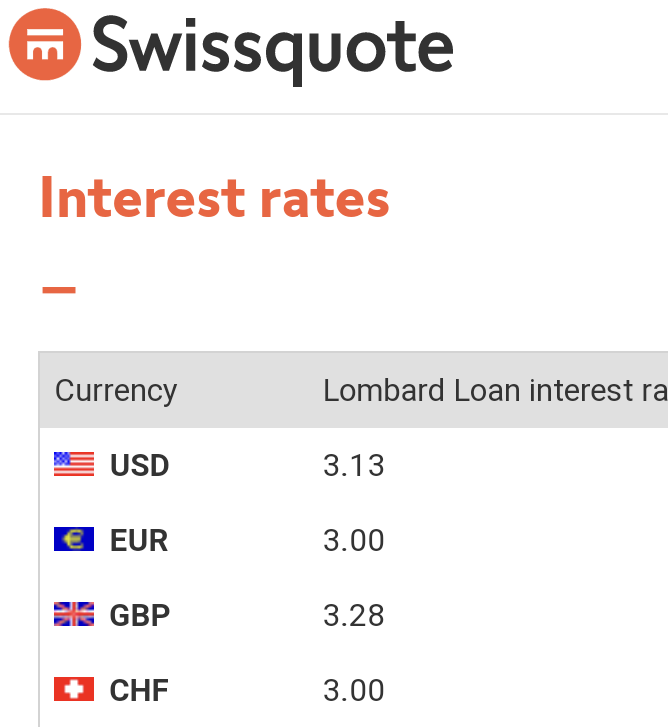

“Interactive Brokers has margin rates of about 2.5% for their lite accounts right now, 1.5% for pro. They will issue you a debit card that allows you to make purchases using your margin, no cash withdrawal required. It’s a fantastic setup as long as your collateral securities are all fairly stable and/or you don’t push it too far.”

From Bogleheads. Is this debit card available for us?

Last I checked the card was only available for the US (as well as it was the margin loan)

but now checking again I see there is an .eu website promoting it:

it may be they open it up for Switzerland as well?

I’ll try to find out more later on

so I converted my account from cash to margin. Now I see that I can withdraw up to 50% of my total account balance by auotmatically creating a margin loan. So they already limit how much you can withdraw to 50% of the assets.

Nice! Monday I will test a withdrawal that exceed my cash availability, timing how long until it shows up in Zak, and then I will immediately retransfer it into IB. I’ll do it on Monday so I don’t risk having the transaction hanging over he weekend and pay unnecessary loan interest fee

btw, you can withdarw once per month, then is 11 chf per transaction:

ABOUT WITHDRAWALS

Fees: One free withdrawal is allowed per calendar month. After the first withdrawal (of any kind), subsequent withdrawals using this method will incur a fee of CHF 11.00

This for me is a game changer! An open line of credit at 1.5% that is moderately safe until 20% of your total account value is truly cool.

Question: we are renting, but if a cool occasion shows up, we may make a move for buying. Unfortunately that would mean keeping a sizeable amount in cash in order not to have to sell during a downturn in order to finance the home.

Would I be able to use a margin loan to finance part of my cash position (the famous 20%) or would that be frowned upon (excessive indebtement?) Or the bank would not care where I got the money from?

Strictly speaking this margin loan wouldn’t qualify as your own capital (20%). But there is no way the bank could tell if those assets from IBKR came from selling equities or from taking a margin loan.

The idea is cool though. When you need to buy a new car, better to take a margin loan with 1.5% interest instead of taking the leasing with 3-5%.

yeah car purchase is another, you can create your own leasing and only with 1.5 % interest, if is not a good moment to sell etc.

Do you know if banks ask for a global disclosure of all your debts and assets when purchasing a home? In that case you could not avoid disclosing the margin loan.

They will ask for your tax declaration in order to check your asset and debt situation. But there won’t be a margin loan listed as you take it at the moment of purchasing the house.

I did a test today:

09:00

Cash position on IB:

100 chf

500 USD

Created a withdrawal for 800 chf to my Zak account

10:00 I see the 800 chf on Zak → I get to actually use them to get a Zak Deal, lol unintended side benefit.

Cash position on IB:

-700 chf

500 USD

margin loan: - ~200 chf

So they don’t convert USD unless you do it.

10:30: I create a payment from Zak to IB, at 11:00 I had my money back on IB

Quite impressive, complete roundtrip in one morning. This convinced me to ditch most of my emergency fund, keeping only really a minimum (from 15k to 5k) and use margin loan as emergency fund.

The only negative really is that the second withdrawal per month is 11chf, so i not completely free, but I don’t see it really happening anyway.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.