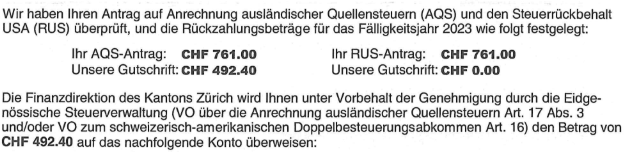

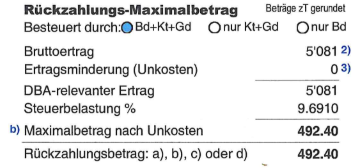

I live in the canton of Zurich. In 2023 I created an interactive brokers account and bought some ETFs (VT, VHT, EDV and others). All had US domeciles. From these I received a total dividend of 5085.41 CHF and 762.81 CHF are listed under withholding tax for that year by IBKR. A year or so ago I filled out that form on the interactive brokers webpage that automatically lets you reclaim 15 % of the withholding tax. The other 15 %, so I read online, I could reclaim through my tax declaration. But some weeks later I received a letter from the tax people in Zurich that I would only get 492.40 CHF back. I emailed the tax people and received an answer I do not understand. From reading the letter they sent me I calculated that they only refunded me 9.691 % (which is my total tax rate) of that initial 15%. But I do not understand why. Can you guys help me out and explain? I do not understand much about this subject. So maybe keep it simple ![]() Also, I need to know if there are other claims I can make at foreign tax agencies? Or can I do something to reclaim the full 15 % next year?

Also, I need to know if there are other claims I can make at foreign tax agencies? Or can I do something to reclaim the full 15 % next year?

I am going to attach some screenshots of the relevant documents. Thank you so much in advance.

Here is what the tax people replied via email (german):

Wie bereits im Brief erwähnt wurde ist dieser Faktor beim Steuerrückbehalt-USA entscheidend:

Interactive-Brokers Dividenden:

Der zusätzliche Steuerrückbehalt USA ist ein in der Schweiz auf Dividenden und gegen Coupons zahlbaren Obligationenzinsen vorgenommener zusätzlicher Abzug.

Erhält der in der Schweiz steuerpflichtige Antragsteller, Erträge direkt auf eine amerikanische bzw. sonstige ausländische (nicht schweizerische) Zahlstelle, wird dieser Ertrag nicht um den zusätzlichen Steuerrückbehalt USA gekürzt. Auf diese Erträge kann kein zusätzlicher Steuerrückbehalt USA gewährt werden.

Anbei sende ich Ihnen zusätzliche Informationen zum Steuerrückbehalt USA:

Falls es sich nicht um einen Fehler der Bank handelt, wurden die 30% Quellensteuern direkt von den US-Steuerbehörden einbehalten (siehe FATCA bzw. W-8Ben).

Der zusätzliche Steuerrückbehalt USA (15%) muss auf der Abrechnung explizit separat vermerkt sein (“Zusätzlicher Steuerrückbehalt USA 15%”), da dieser nicht von den US-Steuerbehörden einbehalten wird, sondern von der inländische Bank direkt an die Eidgenössische Steuerverwaltung in Bern abgeliefert wird.

FATCA

Mit dem Foreign Account Tax Compliance Act vom 18. März 2010 (FATCA) wollen die USA erreichen, dass sämtliche im Ausland gehaltenen Konten von Personen, die in den USA der unbeschränkten Steuerpflicht unterliegen, der Besteuerung in den USA zugeführt werden können. FATCA wird ab 1. Januar 2014 schrittweise anwendbar.

FATCA verlangt von ausländischen Finanzinstituten (foreign financial institutions/FFIs), dass sie sich bei den US-Steuerbehörden (Internal Revenue Service/IRS) registrieren und gegebenenfalls einen FFI-Vertrag abschliessen. Als Finanzinstitut gilt, wer für Dritte direkt oder indirekt Konten oder Depots führt (Banken, Lebensversicherungen, Anlagefonds, Stiftungen usw.).

In einem solchen FFI-Vertrag verpflichtet sich das Finanzinstitut, die von ihm geführten und von US-Personen gehaltenen Konten zu identifizieren und dem IRS periodisch über die Beziehungen mit diesen Kunden zu rapportieren. Soweit erforderlich muss es hierzu vom Kontoinhaber eine entsprechende Zustimmung einholen. Wird die Zustimmung nicht erteilt, gilt der Kontoinhaber als nichtkooperativ und unterliegen Zahlungen zugunsten dieses Kunden einer Quellensteuer von 30%.

Weigert sich ein ausländisches Finanzinstitut, einen FFI-Vertrag abzuschliessen, obwohl es hierzu verpflichtet wäre, gilt es als nichtteilnehmend. Amerikanische Finanzinstitute und teilnehmende ausländische Finanzinstitute müssen auf allen aus den USA stammenden Zahlungen an ein solches nichtteilnehmendes Finanzinstitut eine Quellensteuer von 30% einbehalten, selbst wenn die Zahlung zu Gunsten eines nichtamerikanischen Kunden erfolgt.

Anträge auf Rückerstattung der in den Vereinigten Staaten oder in Drittstaaten abgezogenen amerikanischen Steuern sind auf den amerikanischen Steuererklärungen (Form 1040 NR für natürliche Personen; Form 1120 F für Gesellschaften) beim Internal Revenue Service einzureichen.

W-8BEN

Laut US-Gesetz liegt der Steuersatz für Privatpersonen in der Regel bei 30%. Auf Grund eines Steuerabkommens zwischen den USA und der Schweiz, profitieren Schweizer Steuerzahler von einem verminderten Satz von 15%. Ein Kunde mit Steuersitz in der Schweiz würde daher eine Nettogutschrift von 85% des ausschüttungsgleichen Ertrags erhalten, an Stelle von 70%.

Mit Unterzeichnung des Formulars W-8BEN («BEN» für «Beneficiary») bestätigt der Kunde der Bank gegenüber seinen Status als Nicht-US-Person. In der Folge unterliegt er nicht der beschriebenen US-Quellensteuer (30%). Das Formular W-8BEN darf und wurde von den meisten Schweizer Banken durch ein eigenes Formular, meist in der Form eines Fragebogens, ersetzt.

Das Formular W-9 wird von denjenigen Bankkunden unterschrieben, die US-Personen und bereit sind, ihre Identität dem IRS gegenüber offenzulegen.

Das Formular W-8IMY («IMY» für «Intermediary») ist vom zuständigen Organ einer Flow-through entity zu unterzeichnen und zuhanden der Bank einzureichen. Darauf wird bestätigt, dass die Flow-through entity nicht Beneficial owner der entsprechenden US-Wertschriften ist. Die Formulare W-8BEN resp. der bankeigene Fragebogen sowie W-8IMY verbleiben in der kontoführenden Bank.

Sämtliche Formulare und die dazugehörenden Instruktionen sind auf der IRS-Webpage zugänglich:

http://www.irs.ustreas.gov/forms_pubs/index.html"

Die Kantonale Steuerbehörde nimmt keinen Kontakt auf bei der US-Steuerbehörde. Dies muss der Pflichtiger selber erledigen.