I don’t think Swiss banks offer it because swiss-based clients “normally” don’t need it.

i have various swiss brokers and all subtract 15% us tax and 15% swiss steuerrückbehalt, clearly as 2 positions.

the former is credited to my tax bill, the latter is refunded to me (after i declare it on my taxes).

i have never seen 30% us tax deducted in one position.

the 30% deducted in one position may be that Sq wasn’t convinced that @violetblau was a swiss resident?

you forget that the dividends are taxed as income, which is a function of your total income, deductions and where you live.

it may be 12% in Zug, it may be 20% in Zurich for a middle income and it may be 40% in Geneva for a big earner.

that’s why you get the 15% back and then pay at the tax rate applicable precisely to you.

That’s odd. I am a law-abiding Swiss resident.

I might have to call SQ to ask what’s up.

No, I didn’t forget it. You see, different people here give you different info. One said above that you will be taxed at 15% at least. Now, you’re saying that dividend will be taxed as income. You both are right. But those dividends will never be taxed lower than 15%, no matter where you live. They treat dividend tax differently according to some users above. So it will always be 15% and more. Not lower.

Again, I don’t know who to believe and who is right. But that’s OK. I will file my first US dividend and find out.

What are your Swiss brokers ? I’m surprised they have been applying a double tax treaty without you asking for it. You may not have signed a W8-BEN but something similar from your Swiss brokers (“check the box” when opening the account or an internal form similar to a W8-BEN).

Yes, you are right, my reply was wrong for the case that your income tax rate is less than 15%. For this case, the US dividend withholding tax of 15% is gone (taken by the US), and for this part of income you will have thus lost/paid 15%.

Switzerland will not refund money that actually got kept by the US.

The background is, it has to do with the DTA double tax agreement CH-US, that you don’t have to pay tax twice in US and CH. But if US takes more than CH would take, then CH won’t credit you something that they didn’t take.

Swissquote, CS, Migrosbank, Postfinance.

I suppose they all know where my residence is, and made me sign something saying whether I have any connection with US.

That may be equivalent to the questions on a W8-BEN for them?

I’ve only ever seen 2 clear deductions off the US dividends, 15% wht US and 15% steuerrückbehalt CH.

I heard it’s very time-consuming to do so. You basically have to contact IRS and file directly to them. It also costs something I believe. It’s not worth it unless you have thousands of dollars to claim.

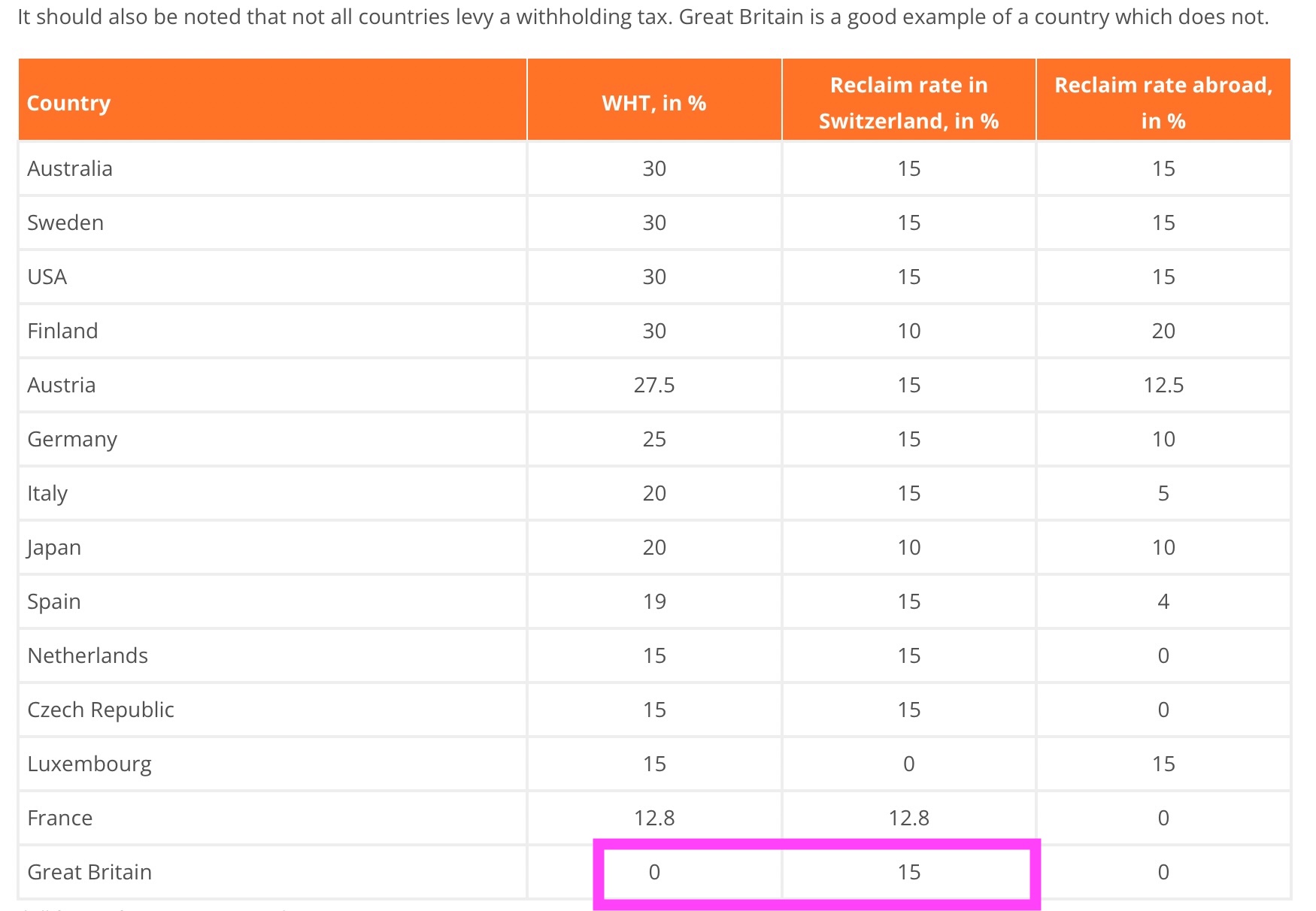

15% are always taken by the US. The IRS will never refund that to Swiss tax residents. The very least you pay on US dividends is 15%. There is no way around that for us. Thanks to the double tax agreement, you’re not taxed twice on US dividends, though (assuming US stock/ETF and everything is done properly: W-8BEN and DA-1).

The possible option for a refund from IRS is only relevant if you had 30% US WHT deducted (i.e. no W-8BEN). In that case it may be possible to get a refund for the extra 15%. However, that’s expected to be painful, time-consuming and the best result is probably receiving a US check from the IRS by mail, which you can cash somewhere with high fees.

The W-8BEN route is definitely preferable. If your broker can’t do this correctly (at least on request), switch to one that can.

Another note for clarification, if your Swiss tax rate is below 15% and because of this you’re not credited the whole 15% US WHT via DA-1, you still get a credit for your tax rate (assuming you’re above the CHF 100 minimum). E.g. if your tax rate is 12% you get 12% of the dividends credited (and the other 3% can be deducted from taxable income as wealth management cost, as far as I know). I.e. it’s not black and white. You don’t lose 15% of the dividends the moment your tax rate falls below 15%.

There is no additional Swiss tax withholding without W-8BEN. I.e. with Swiss brokers you should always get a 30% deduction, either 30% US WHT or 15% US WHT + 15% additional Swiss tax withholding. Never 45% in total. As the article assumes 30% US WHT, additional Swiss tax withholding does not apply. However, that assumption is a big red flag.

Whichever way that works - and I personally never really dug into it (additional tax additional withholding), since I haven‘t used Swiss brokerages much…

If you‘re talking about a Swiss investor receiving U.S. dividends, the applicable withholding taxes and how/where to reclaim them, surely you should mention it?!

If/when your tax rate is significantly below 15%, you may want to consider switching to Irish ETFs where possible. This doesn’t recover the 15% from US stock dividends, however, at least you won’t pay 15% to the IRS on non-US dividends (details depend on the domicile of each stock). You’ll have to make your own calculations based on your asset allocation on US stocks and possibly higher fees of Irish ETFs.

The Irish ETFs are quite unique. I might consider that as I have way lower tax rate than 15%.

Another alternative is to invest in ETF or dividend stocks. Having dividends is not always advantageous. One has to keep in mind that the stock price falls at the same rate as the dividend payout more or less. So it doesn’t really give you the edge but just another way to deliver income.

When selling stocks without dividend, we pay nothing as there is no capital gain tax in Switzerland unless you’re a pro trader. So it always depends.

The Irish ETF also has to pay (L1) withholding taxes for other countries besides the US, yes. Details depend on each country and their double taxation agreement with Ireland. However, the same is the case for US ETFs that hold non-US stock. For some countries the US has better double taxation agreements and for other countries Ireland has better double taxation agreements.

If the tax rate is just a bit below 15% it’s likely not worth it switching e.g. from VT to VWRL. However, if you have a US ETF with a high ratio of non-US stocks or your tax rate is extremely low, switching to an Irish ETF may be worth it. E.g. I would definitely recommend an Irish ETF for purely European or EM stocks.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.