one of my big financial nuisances is the “systemfremde Quersubvention zwischen den Jahrgängen der 2.Säule” (“the Cross-subsidization between the 2nd pillar age groups that is alien to the system”)

With the latest attempt to do something about it, it is the third time that a BVG reform is stopped by popular vote.

So i thought, why not come up another initiative that focuses on the core problem, the cross-subsidizing (which i believe is generally perceived as not proper). The idea would be to write something to the constitution like “Die Quersubvention innerhalb der 2.Säule zwischen verschiedenen Altersgruppen ist zu vermeiden, und ab 2028 verboten.” E.g. a formal ban of cross-subsidizing between age groups.

The thing is i have zero knowledge on how to go about this idea, i have no political network or experience.

As a first test, what is the reaction of [the not exactly representative sample of the swiss population of] you, the forum users?^^

in the end the key requirement is the signature of 100k supporters, which i naïvely could think of doable^^

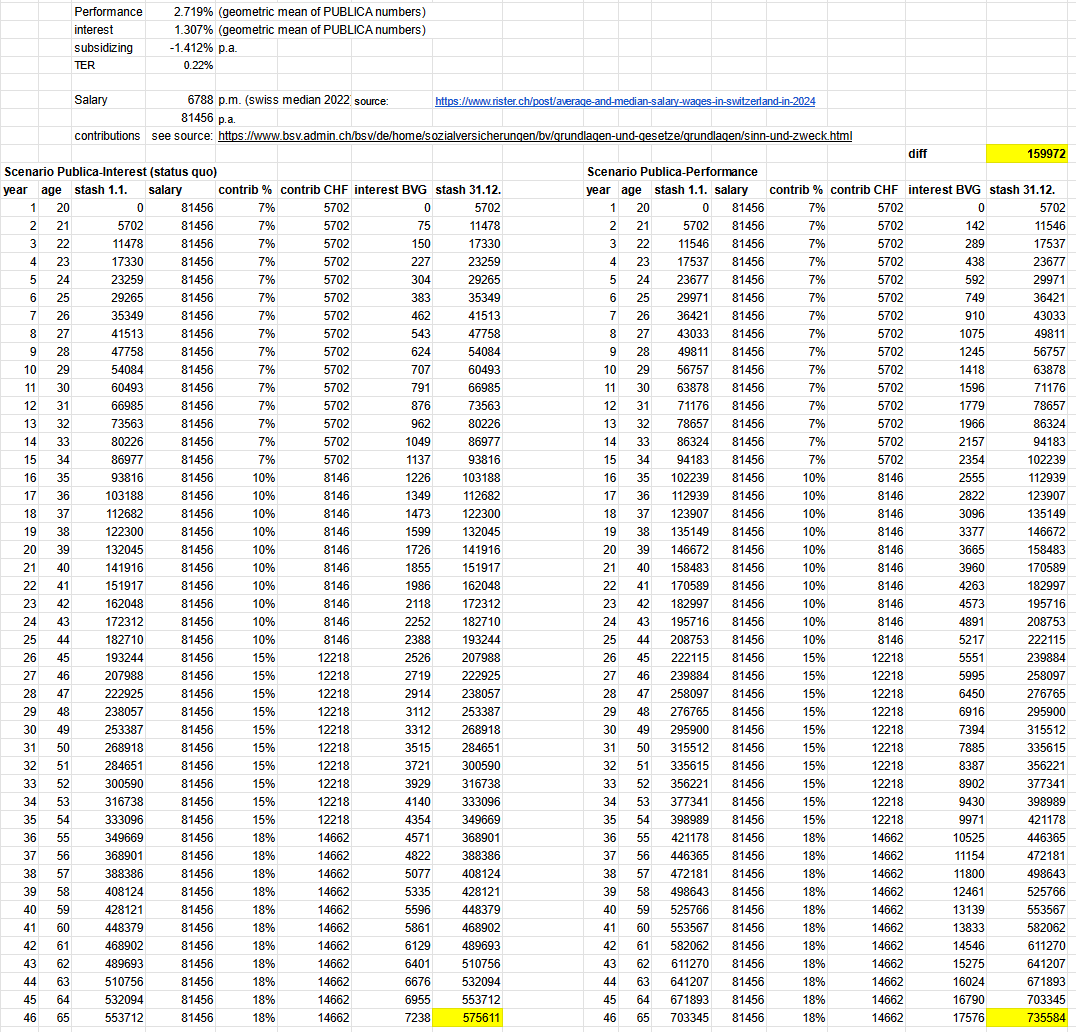

For the record: in the scenario of a median person working form age 20 to 65 for the swiss median salary of 80k, using published BVG performance values from PUBLICA, the federal Pension fund, loses out on about 160k over his lifetime due to the hidden Quersubvention:

The problem is that most people won‘t get it. Anything more complex than „I get less/more“ isn‘t something most of the voters will understand. You are talking about a „highly technical“ finance problem. Like discussing passive nuclear power plant safety systems and which to implement (by vote).

Plus you have voting fatigue. People won‘t care about BVG reforms for s couple of years. If you try to get signatures now they‘ll think „didn‘t we just vote on BVG?“.

I think it would be difficult as all cantons have voted against the reform of the conversion rate. For an initiative to pass, both a majority of votes and the majority of cantons is required, that’s a challenge.

I don’t think getting the 100k signatures would be the hard part. The text would be fought by the same actors as the reform of the conversion rate, with the same arguments (the easiest and most practical way to avoid cross subsidizing between generations is to lower said conversion rate). They are apparently able to reach far.

The second problem I see is that once the text enters the constitution, the parliament has to come up with a law. That law can be subject to referendum and would bring us back to square one. That means that the text of the initiative should include provisions in case no law can be passed before a certain date, which would make it less generic and less easy to defend on the basis of a discourse of: “what we want is to write the principle in the constitution”.

That’s not impossible, but it requires a lot of energy to get there. We should make sure we’re willing to expend it. First step would be to constitute a motivated comitee, with a motivated support group. We’d need to reach further than just this forum.

I think for intellectual purposes , this exercise could be interesting because it might help all of us understand how difficult such things are.

But rather than fixing one of the issue which makes one party happy, the reform need to address all the issues. As far as I get it , there are following problems with „mandatory pension“

Facts

Let’s list down some facts. I hope they are right

every employee contributes to their pension fund. Let’s say the total salary is X. There is a limit for contribution to mandatory pension. Let’s say it is Y.

contribution A -: any contribution made for portion Y, goes into mandatory bucket and attracts 6.8% conversion rate (by law ) at time of retirement if employee choose annuity option.

contribution B -: Any contribution made for portion (X-Y) goes into non-mandatory bucket and attracts lower conversion rate depending on employer.

As far as I know Y = 88,000 CHF at this moment. It should have been lower 10 years back. This refers to annual income.

Pension pots for retirees and contributing members are same for Mandatory portion. For non-mandatory portion some companies offer 1E plan and pots are separated.

Pension funds invest money and earn return net of costs, let’s say its R

Challenges

next points only refer to Contribution A

Everyone who has been making contribution A in last years (many years) made contribution under assumption of 6.8% and are expecting that money to be paid. If this number were to change they are not happy

We need to acknowledge that not everyone lives until 95 years old. The problem is not only related to actual payment but perceived concerns in case someone lives longer and run out of money.

There are people who might be in middle. Let’s say they contributed 20 years and need to contribute 20 more years. I think for them it might not be clear what is a better solution. Lower interest on their contributions or lower conversion rate at time of retirement. Some sort of calculator need to show people exactly what it means. I have to say that if people understand that they themselves are negatively impacted, then they would have more incentives to go into detail.

Pension funds are struggling (not all) to provide 6.8% conversion rate if they only consider money that is in fund of retirees. Thus they often take money from contributing members.

Rough math suggests that 100 CHF in pension capital would last 14.7 years (6,8% conversion) with 0% return on invested capital. This pension funds need to keep money invested to increase the duration. 3.25% return on investment would ensure money lasts for 20 years. 4.7% would be needed to make it last for 25 years.

But seems the returns are not enough due to longer life expectancy.

This cross transfer lead to fact that contributing members get lower interest (I) vs Investment return (R). Not for all pension funds though.

Lower interest ( I) would lead to lower pension capital for currently contributing members and thus this issue is seen as pushing can down the road.

Any solutions proposed need to address all of the challenges and not just one. Otherwise there wouldn’t be any agreement. We cannot assume that people would vote Yes when they are not in agreement (I.e negatively impacted)

Stopping cross financing only fixes one challenge and hence not a real solution. In addition education need to be made about all aspects. We need to be able to keep ourselves in shoes of others while making suggestions. Young vs old discussion does not go very far.

In my view solution would need following element

plan to cover shortfall for retirees if any

plan to stop cross financing

Plan to let people move from one option to other (common pool vs individual pool)

There usually is a gap of maybe 5 years in between two initiatives about the same topic.

I suspect that in five years’ time, a vote that could reduce second-pillar pensions will have a much better chance of being approved than it does today.

This is because all of the baby boomers (the largest voter group) will have already secured their paydays and will be more inclined to “save” the pension system.

break the current setup (capitalization based), keep the current rates and eg add redistribution explicitly funded by an increase of taxes (ala first pillar)

make the current system sustainable and link the conversion rate to the inflation/risk-free rate/life expectancy

Maybe if proposals are contrasted people are more likely to think harder about a long term fix (and paying with taxes tend to make people think more about the consequences than leaving the next generation deal with it)

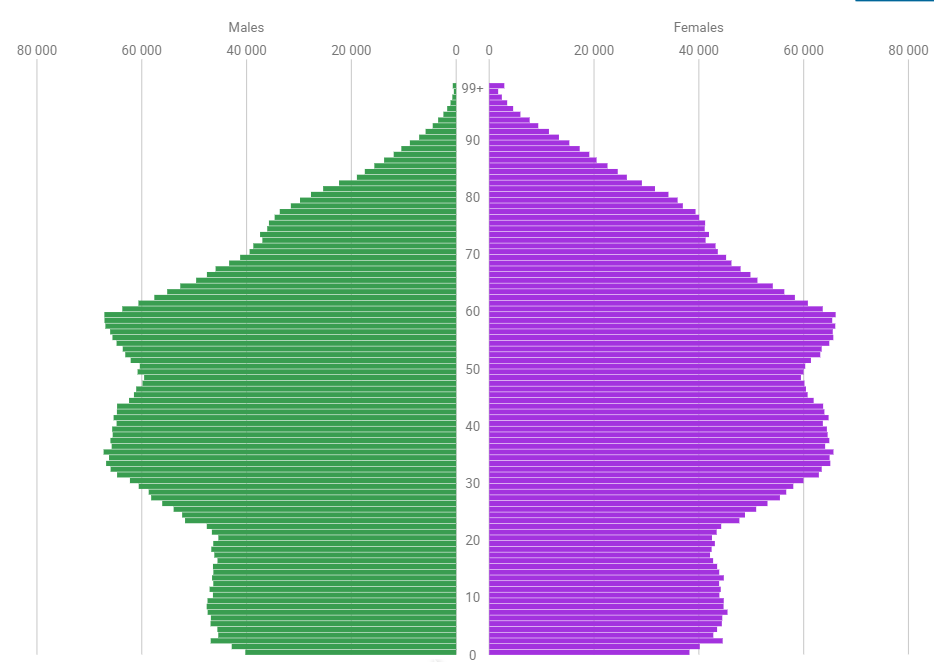

This chart shows the problem. We currently have (using eyball mark 1) about 2 workers per retired person. In 20 years, that becomes 3 workers per retired person.

If politicians want to have success with a new law, they should not propose changes for the people, but for pension funds. It is now very clear that people don’t want to pay more and/or get less later.

Pension funds should change, they should be able to invest better, and with longer time horizons, get better conditions.

The fixes all make mathematical sense. They’re also going to be extremely hard to pass.

For most low income people the low pensions are not going to be a problem. They will receive tax funded Supplementary benefits (Ergänzungsleistungen/Prestations complémentaires). It is mostly an issue for experts and wealthier people.

So, there’s not a lot of incentive to fix the system.

My prognosis is that at best small fixes are going to be made and that the fundamental issues are not going to be touched.

We’ll just keep keeping the whole pension system afloat through taxes, and companies with high income people will switch to providers that have a almost no retirees.

In general, the 2nd pillar is going to be under attack from many fronts and will become less attractive as a pillar.

The Federal government is proposing to abolish the favorable tax rate on capital withdrawals as a means to plug the deficit.

Reportedly, the political left wants exactly the opposite, namely using the second pillar increasingly to redistribute funds - if not abolishing it altogether in favour of a ‚stronger‘ AHV. So you can’t count on thei support.

Next, if you want to make the change, people will ask you whether they‘ll ‚lose out‘.

So you tell them. Presumably, people in the run up to retirement will lose out (yep, that bulk in the age pyramid up thread), so don’t count on their support. What, you propose to also touch existing pensions, after a few years, to make the numbers work? You are cooked right away.

Or you don’t tell them or keep things in obscurity- speculations will follow possibly making things even worse.

create an option for a market where different players can offer 2a plans. Let’s call it Fin2a. The conversion rates for these Fin2a plans would be determined by government based on market situation of annuities and should not need any referendum to change. Imagine how today mortgage reference rates work, similarly annuity reference rate can work. Employers can also offer Fin2a plans but they need to segregate individual accounts.

create an SB pension fund (backed by sovereign) to cover liabilities of retirees after age of 80. This is applicable for employees who would continue to use 2a plans (non Fin2a). Until age of 80, 2a will pay the pension, post that pension would be paid by SB fund.

all capital for the employee should be transferred from 2a plan to SB fund at age of 80

#2 would allow separation of fund accounts for contributing members and retirees.

#1 would reduce the burden on 2a plans over time.

Now the question is how can SB fund the liability of pensioners once they reach age of 80. Today this is funded by contributing members of individual companies. Perhaps a mechanism can be developed to charge the companies accordingly who transfer liabilities. Or a payment could be extracted via tax system because eventually contributing members are paying for it anyhow. I know this is the most difficult part because no one wants to own this part. But without someone owing this problem won’t be solved. I wonder what exactly is the liability in pure CHF terms.

I think if Fin2a prove to be efficient and attractive, people would gravitate towards them because it’s like 3a account where multiple players can play role to bring costs down. Inclusion of SB fund can help pension funds to invest appropriately and maximise returns for their employees. Hopefully this would reduce the eventually negative balance for SB pension fund.

Choice of Fin2a should be optional for employees above certain age let’s say 45 years old. For younger employees , no choice as they would have 20 years to make up for the 15% lower conversion rate and ideally should have better returns in Fin2a to make up for it.

P.S -: I assumed that first 15 years of conversion can be paid by company pension fund because pension capital should be enough to cover those years.

FYI I think using a central bank is a no go (really not the job of a central bank to have that kind of things in its balance sheet), do you mean some kind of sovereign fund backed by the confederation instead?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.