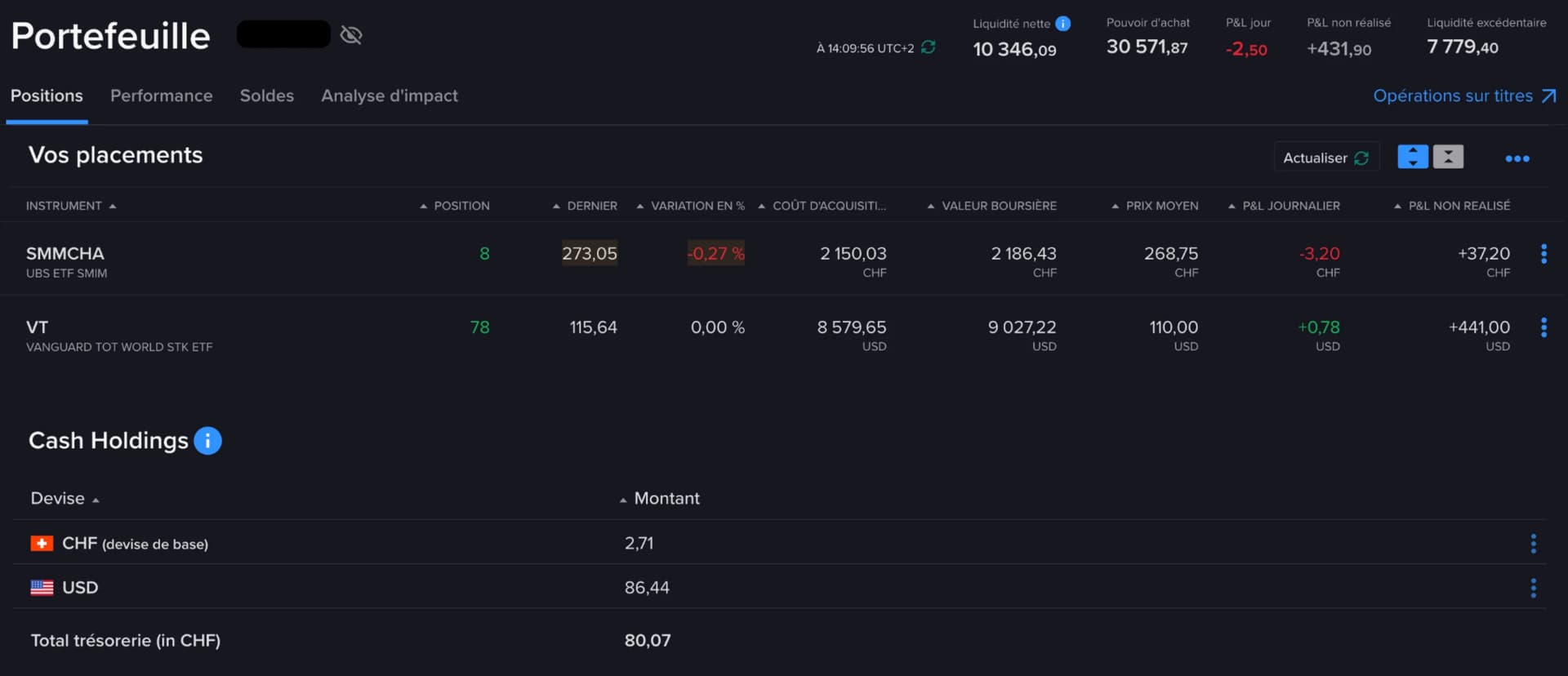

The net liquidity is CHF 10,346, while the unrealized P&L is CHF 432.

I’ve invested CHF 10,000 so far. So, why isn’t the net liquidity CHF 10,432? Could it be the purchase fees for the ETFs? Is there a summary report that synthesizes all this?

Also, I’m having a bit of trouble fully understanding the concept of compound interest on ETFs. If you have an explanation that summarizes this, I’d appreciate it.

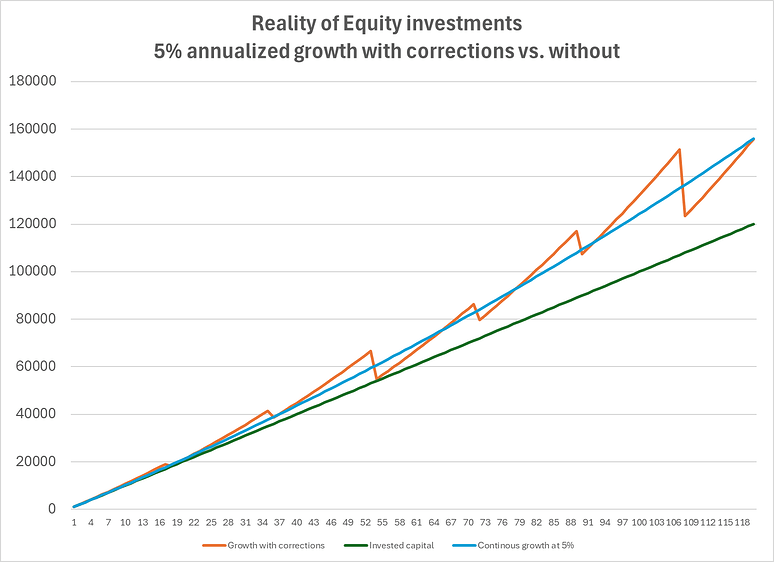

Equity ETFs compound over time, but they do not do so with any guarantee.

There is a difference between Equity ETFs vs. Fixed deposit.

Let us assume you made two investments. Each of 1000 CHF

Investment 1 -: Fixed deposit with fixed interest of 5% for 10 years. All money stays in depot until maturity of deposit.

Investment 2 -: Stock ETF with “expected” compounded growth of 5% over 10 years. Note the emphasis is on the word ÊXPECTED.

At the end of 10 year period, both investments would have same amount of money. However, following two points apply-:

Investment 1 will for sure have 1000 x (1+.05)^10 = 1628 CHF

Investment 2 is expected to have 1628 CHF as well, but there is no guarantee and it would depend on how market would perform. It can also be that you end up with 2000 CHF or 1000 CHF

Same is true if you invest equal amount of money on regular basis often referred to as Dollar cost averaging. Lets say the for illustration purposes, the expectation of 5% was correct. During this 10 year period, the growth profile might be very different. An example below for illustration purposes. Orange line shows how the ETF growth might look like and blue line would be for investment where you deposit money every month and have guaranteed 5% return.

Hmmm need to add some nuance to this: if it’s a (theoretical) fixed 5% interest or a bond coupon rate. The bond wouldn’t compound, it’d just return the coupon rate until maturity. I’m probably confusing the OP even further…

OP, stocks don’t compound interest, they compound growth. For all intents and purposes it’s the same thing. Compounding simply means growth of, or on top of, growth.

Picture a $100 stock appreciating (gaining) 10% in a year, it’s now worth $110, $10 is what the appreciation gave you. Now picture the same stock gaining another 10% in a year, bringing its value to $121. That extra $1 is due to compounding, growth on top of the past year’s growth.

Now picture a $100 bond with a coupon rate (=interest) of 10%/year. It’ll give you $10/year until maturity (=when it expires) and you get your principal - the money you bought it for - back, along with all interest payments you got over the years. In 10 years you’d get a total of $200 from the bond and $259.70 from the stock (if you sell…!).

I just checked my own data. It seems Net liquidity is updated at different rate vs unrealized P&L. You need to click the refresh button next to NET LIQUIDITY.

However, I have to say, you need to do your calculation differently

Unrealized p&L + Cost basis across all positions including cash = Net Liquidity

Cost basis might be slightly different than what you deposited due to exchange rates etc.

Actually, it’d be critical to sit down and make a plan (if you haven’t already). In many people’s opinion the exit, or endgame strategy and everything in between is as important as the entry strategy. It’ll help you avoiding mistakes, stress.

Put down what’s your end goal, how you’ll get there, what will you do in case of scenario A, B, C, how you’ll utilize the savings/investments and on what condition, long-term tax considerations, family and estate planning etc etc

The plan is quite clear: I aim to reduce my work percentage by 50-55 years old (I’m currently at 30). I have a strong second pillar, and my wife and I also have a third pillar.

We are able to invest 2,000 CHF each month in ETFs (80% VT and 20% SMIM), and we also have savings.

My idea is to avoid being too emotional during market “crashes” and to reevaluate the situation in 10 years to see the outcome of this strategy.

I’m, of course, happy to hear any advice on this strategy.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.