I have a question related to our very specific position as Swiss fire investors. Our ultimate investment véhicule would answer to the following criteria:

Highly diversified (hence US and world index funds)

Very low TER (max around 0.2%)

Liquid investment (transaction volume)

Limited currency exposure (hedged)

Reading through a lot of threads and investment strategies, I went on my own quest for the ultimate ETF for Swiss investors, and I would like to have the community’s opinion on that.

Synthetic means the ETF does not hold the securities, but a commitment from a counterpart to deliver the index return, with a 90% collateral value in the form of G10 gov bonds hold in an “escrow” account. This means if UBS default on delivering the ETF counterpart commitment, it can pull 90% of its value to return it to its investors.

Are you familiar with synthetic ETF? What is your opinion on this product What is your ultimate Swiss investor ETF.

I hardly like anything about this fund.

If you have read a lot in this forum, you should have also come across the forums’ favourites… compared to those, the mentioned fund loses basically everywhere as far as I can see: too expensive (compared to us-based ETFs), not physical (but synthetic),…

But maybe that’s just me and I amissing something?

Pretty much spot on. @Moustachu I encourage you do some more reading before asking these sorts of questions. Hedged UBS funds have been discussed as well.

Thank you for the comments. I’m not so concerned about swap ETF, but more so about the cost of hedging, which indeed from other threads seems to be an expensive insurance policy that is not easy to read from the fact sheets for a novice. Currency exposure is good to some extent, and I hold already 50% of my portfolio in euro and usd which I bought at a convenient time, but I don’t feel comfortable exposing more than that to usd. Hence my question above.

Why exactly are you afraid of more exposure to the dollar/euro?

For equity investment, in the long run currency exchange rates fluctuations are immaterial and easily outshadowed by stock returns. 1970 to now USD/CHF dropped from 2.5 to 0.98 - it may seem like a lot, but it’s merely -1.68% per year, whereas stocks returned on the order of 10% (in USD)

Your exposure is not limited to currency in which stock prices quoted, but more related to fx exposure of underlying companies and many large cap companies are active worldwide. It’s actually even not that easy to get exposure to CHF in equities from this perspective. If you just dump the money into SMI index, consider that the biggest components of it are actually giant multinational companies whose busineses have very little to do with Switzerland. Nestle’s making just a whopping 1-2% sales in Switzerland. It is not a CHF exposed company at all, even though it’s quoted in CHF.

Currency hedging is a bet that works both way: dollar drops => you gain from the hedging positions, just as you’d expect, but if dollar rises => you lose and there’s no option not to take the loss - those hedging contracts are futures, not options. Ultimately you get the USD performance of your target index in CHF, minus relatively fixed hedging costs of about 2-3% today.

Good point. Currency hedging is getting the return of an instrument’s original currency, but in your desired currency (and not for free).

A true insurance policy are forex options. You buy an option to exchange USD to CHF at a certain rate, so if the rate ever goes lower than that, you can execute your option.

It has been used by polish companies before 2008, as PLN was getting massively strong. They were trading a lot in EUR, and wanted to protect against strong PLN. But the banks sold them a packaged deal: an option protecting companies from strong PLN with an option protecting banks from a weak PLN. And of course as soon as the financial crisis started, PLN lost a lot in value. So much for insurance

Currency hedging doesn’t really cost that much. On average you will get the same return.

I think most make the mistake to compare nominal currency exchange rates over the last 20 years or so. Overall it is zero sum, there may be long streteches of time where hedging is better and times where it is worse.

Hedging equities doesn’t improve risk adjusted returns, so it us not worth it to do. Underling currency risk of a stock is also quite hard to determine.

However currency hedged bonds improve risk adjusted returns. The problem for Swiss investors is that bonds don’t return much.

I haven’t read all the posts, so maybe the following was already mentioned. It was for sure mentioned on this forum already somwhere else because I have the information from there.

The bottom line is that globalization has grown so deeply into almost all companies that currency hedging is senseless. Every Company buys supplies from a company that might operate in another country and sells its product to other countries. The only reason to do curreny hedging is, if you would invest in a US company that produces everything with US made supplies and sells everything within US but even then the buying power from its customers might depend on some exchange currency because they are selling their product mainly to the EU? So good luck on your dive into the rabbit-hole if you would want to really figure out the cost/benefit ratio of currency hedging - it’s for sure not worth my time.

It *is* the cost of hedging. These forward contracts are exactly what your hedged etfs are buying, because it’s how their benchmarks are constructed, and those are the prices they are paying.

Yes, the hedging cost is strongly related to this difference - no free lunch, covered interest parity…

You don’t hedge in order to keep the nominal value of the exchange.

If the expected future forex rate turns out to be exactly true, then the hedged and the non-hedged investor will have the same return. If we assume that the markets are at least somewhat efficent, then the expected return of a portfolio stays the same, hedged or not.

For equities hedging doesn’t make sense because it doesn’t reduce volatility for them. If you hedge bonds, they will have reduced volatility and it is sensible to hedge.

I don’t think currency rates are that predictable. For currencies with high interest, in double digits, or from countries with high inflation, sure, you don’t need a crystal ball to see where it’s going, but for stable currencies like USD, EUR, CHF, with yields hovering around 0% +/- 2% and low inflation rates I think the forecasts based on interest rates alone are very unreliable.

Dollar was at around 0.95 CHF 5 years ago and 3% interest rate diff would have implied it should be now at at 0.82, yet here we are with the dollar at 0.98!

Yet with hedging you’re going to pay the full price according to current interest rate diff at all times, whether that forecast is right or wrong! And a very steep price as Swiss frank has punitive -0.7%…-1% interest rates that you’re going to pay if you bet against it.

It will turn them into negative yield and it would not make sense to buy them at all.

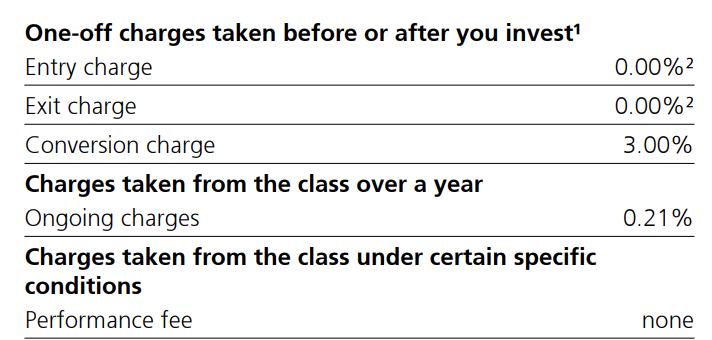

Why is the cost of hedging not included in TER and not transparent?

First of all, I have to go dig into the Key Investor Information (KIID) document to figure out that there is a one off “conversion charge” on top of the annual charge (TER):

(This seems to be important enough information to be in the charge table of the fact sheet rather than KIID only)

Second of all, when I try to find how exactly UBS defines a “conversion charge”, it is nowhere to be found. Conversion could mean different things in ETF glossary, from converting an ETF into a fund title, to converting currency.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.