Generali : 20 year, CHF 243.70/ year

Capital : CHF 200’000

Any better offer from your side ?

Generali : 20 year, CHF 243.70/ year

Capital : CHF 200’000

Any better offer from your side ?

I haven’t been able to look it up yet. The baby is 1 week old and corona made sure that family could not fly in to help ![]() I’ll write back here as soon I as I have some more info.

I’ll write back here as soon I as I have some more info.

I also had a quote from Mobiliar. More expensive than PAX and Swisslife, but they had some interesting perks (for example, doubled payout if 2 persons insured die at the same time, how unlikely this may be).

The quote will vary significantly depending on your age, duration of insurance, risk group etc. I also went for decreasing sum, as I accumulate wealth independently anyway. My policy is 500k for 30y. Decreasing ~16k/year which suits me perfectly.

Hello @belouga13

I have exactly the same contract that I concluded in 2018 in Geneva, but in 3b because it is tax deductible up to CHF 2’200. I have been living in the Canton of Vaud since 2019, so I changed this insurance to 3a in April 2020.

It is by falling on this forum and various other blogs on the FIRE movement that I noticed the strangeness of this type of insurance. After calling my advisor at Swiss Life Select last week, he recommended that I keep this insurance and mix it with a bank 3a (I told him about VIAC, and he told me it was a good product, but nothing more).

As of today, I have only paid 2x 2’200 CHF (4’400 CHF) and I have to pay my contribution for this year, which I haven’t done yet, because I decided to cancel everything and transfer it to VIAC with a long term (35 years); cash surrender value at CHF 1’298.- (so I will lose CHF 3’000.- with the transfer, but I prefer that than to lose more next year).

Moreover, this is a shit product, I earned CHF 14 last year with the excess part, wow!

@Julianek: I thank you for this complete post which only confirmed what I thought for a few weeks about this type of insurance. My adviser even suggested me to keep this insurance to become a homeowner. I don’t know if I’m going to become one one day, so I prefer not to keep it and have to re-contract it, but surely with a 3a bank if necessary than a 3a life insurance… Thanks again!

Swiss Life Select are among the worst. They sold me a Life Insurance 3a in 2016 and fortunately i realized that it was a money-losing machine early enough so i did not lose more than 4’000 CHF.

First advice: Those 4’400 CHF you paid are sunk costs, don’t expect to recover them and exit as soon as possible.

Second advice: I will assume Swiss Life Select used the same sales techniques with you as they did with me. If you want to understand how badly you were manipulated, I advise you to read Influence, by Robert Cialdini. In particular, you will learn about the following principles:

Social Proof Principle : Swiss Life Select usually contacts you because they asked one of your acquaintance who could benefit from their services and you were mentioned at some point. They make sure you are aware of this. When people have no clue about one product, the fact that their friends and acquaintances use it can only be a good sign, right?

Commitment/Consistency principle: Swiss Life Select will ask to send their advisor directly at your home to have a first session with you. There is a bias in all of our brains that makes us want to look consistent in our actions: surely if I have let those people come into my house, i am interested in their products, right? You will find it very difficult to reject them afterward.

Authority Principle : this one is more classic, but the “advisor” was likely to wear a suit, look like he knows what he is talking about, and maybe using quite a lot of jargon, so a hierarchy of knowledge is created between you two: he is the one knowing what you should do, and you should listen to it. (At least, that’s how your brain works).

Liking principle: like any good sales person, your advisor was likely to be friendly, even complimented you at some point by a) trying to find a common point between you two (in my case, it was musical taste) or b) praising how good of a decision maker you are and how other people are idiots. We are easy preys for flattery.

Scarcity: i don’t remember but it is likely that his guy made you a time-limited offer, triggering a fear of missing out.

Reciprocation: if this guy made you any insignificant favor, it is likely you want to reciprocate.

And other techniques i may have forgotten.

Any single one of these factors are powerful in themselves, but combined together they are really deadly. No wonder so many people fall in this trap!

That’s exactly what happened. My little brother was contacted by my current “financial advisor” through a friend of his, and then my brother recommended me and I went to the appointment, but at Swiss Life Select. I was surprised when he’s suggested me a Zurich product and not a Swiss Life one, but I trusted my little brother and the advisor… My fault.

Nevermind, I’m ok to lose my CHF 4,400 rather than CHF 6,600 next year. Better now than after.

I strongly dislike these kinds of business practices and also feel pity for people with such a job.

If I read your description and this article about their job training, I can’t help but feel this is one of the worst jobs I could imagine. [Obviously other people feel different, but I’m not sure if I would choose this job over being a sewer worker.]

They are not financial advisors, but salesmen. They can only recommend their products and are paid with a commission.

Yes, cancel ASAP. Maybe the loss is lower if you take into account the saved taxes.

Swiss life select hires a lot of young folks without solid finance backgrounds (check their job ads). The turnover is really high and obviously they keep only people doing the most sales.

In general, for big purchase commitment: compare, read all the contracts, take some time to think about it, always sign when you are alone to avoid "pressure, ask a second opinion.

.

I figure it out now that I’ve got more information about them…

I’ve already create a VIAC account and send an e-mail to my salesman with the transfer document. I’ll see what he will said to me, and if he doesn’t want to do the intermediate with the Zurich, I’ll send it either to Zurich.

I’ve already said to my little borther to do the same by the end of this year. Unfortunately, he already pay the premium and will lose CHF 6’600…

I’m glad to discover this forum and that @belouga13 made a post like this to share his interrogation.

For anyone still following my post, and to inform anyone in a similar situation as me, here is a brief update:

I asked both companies for the repurchase value of my contracts, dont have the exact numbers with me right now, will post them in a few days, but nothign out of the ordinary to the others who posted similar cases in this forum.

However I do want to point out my experience with VIAC so far. I setup the account easily, and selected their “transfer from another 3rd pillar” option, filled out the form, sent it to them by post, and 3 days later received a confirmation from them stating that all had been done on their side, and that I only have to wait for a reaction from the other 3rd pillar providers (22nd of may). I received a letter from Retraites Populaires last week, which I simply had to sign and send back to, confirming that they should transfer the remaining value to VIAC, while cancelling the current contract with them.

I am still waiting for a reaction/ reply from Zurich Insurance, but as I am not home at the moment, I might have a letter from them in my mailbox.

For the Zurich, I guess they will not answer quickly for the transfert. I sent them a registered mail with acknowledgment of receipt (for legal proof) where I terminated my 3a life-insurance in addition of the « transfert for another 3a Pillar » from VIAC on the 11th of May.

Since then, I didn’t have any answer to the transfert neither to my termination letter. I’ll take you in touch if they answer me before you ![]() (I don’t have a large amount invested so I hope it will not take to much time…).

(I don’t have a large amount invested so I hope it will not take to much time…).

Updates !

I’ve received two letter, one from Zurich Insurance and the other from Swiss Life Select.

Zurich confirms that they’ve received my termination letter and transferred request. They need more days in order to give me an answer.

Swiss Life Select informed me that “normally” the first 36 months of cotisation of my 3a life insurance are used to cover the insures risk, so that 0 CHF is invested and therefore the entire amount of my investment (4’400 CHF) will be lost ![]() They are looking to contact me in order to stay with them (haha).

They are looking to contact me in order to stay with them (haha).

We will see what’s will happening in the next days (months?).

Hi at all,

I have started Swiss Life FlexSave Duo almost 3 years ago. Reading this post and others in the MP forum I’m realizing that I did a big mistake.

When I met our swisslife select person, I was just arrived in Switzerland and I didn’t know anything about 3rd pillar/2nd pillar and other swiss financial mechanisms.

In the last year I have started to read blogs and other resources in order to learn how to better manage my wealth. In the last weeks I was reading the forum and I found this topic that makes me curious.

If I well understand I have to find a way to stop my life insurance as soon as possible and move my 3rd pillar to a bank account (e.g. VIAC).

Could you provide me some suggestion in order to do it properly? Yanikuza are you based in Geneva?

thanks,

Matteo

Hello @Mat_ley,

I’m not anymore based in Geneva. What kind of suggestion do you want ? I can tell you how I did my termination. But you also have to be sure that you are ok to lose what you invest in your 3a life insurance. Is it a 3a or a 3b, as you seems to live in Geneva, the 3b is deductible from tax and can be an alternative to stay with it.

As of today, I just received the confirmation from Zurich and SwissLife Select that my request is being processed. I have been informed that the transfer of my 3a life insurance account will probably be CHF 0.- as the first 36 months of premiums are only used to cover the insured risk. Therefore, I can confirm that the first 3 years of premiums are not invested at all for your 3a.

I would ask Zurich and Swisslife what is the amount on the 4 and 5 years. Maybe you can get back some money, another solution would be to reduce amount on the contract. Maybe you can still get back some money

I have just concluded the cancellation process for my PAX 3a insurance. I lost CHF 11’756.05 in the process (almost 2 years) + the opportunity cost of investing that money somewhere else. And in junt one month I already have a positive PnL of CHF 923.88. Not looking back.

You really think that’s a big mistake ?

Have you the detailed interest rate from the 3 past years please ?

And amount put each year ?

I think that’s a good security because first pay mortgage if something happen.

Second you not lose money during bad market year but yes you win probably almost nothing.

And you have tax deduction.

This year on VIAC you can may be lose a high percentage of all money put on the market and can take a lot of time for retrieved lost money. FlexSave Duo can keep your money.

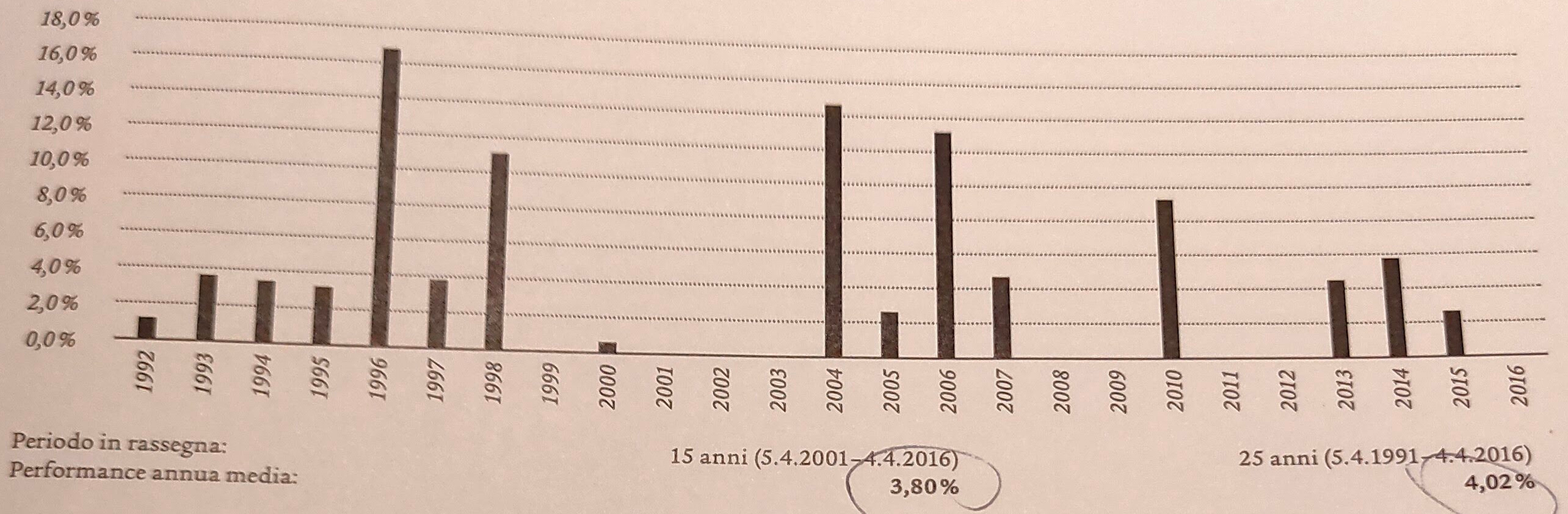

This is from the document I have received when I started. According with it, They have a basket composed by:

34% SMI

33% S&P 500

33% EuroStoxx 50

The maximum theoretical performance is 2.3%/months. They will apply only positive performances, negative ones won’t be taken in account.

Ok thank you 0% for 2016 can be ok not a really good year.

2017/2018/2019 should be positive on interest rate.

One thing, you should be able to put your life insurance on hold instead of break contract.

Ask may be about that like that you can hold contract during bad years and found another way or just wait retreat for retrieve your invest if work really like that not 100% sure.

Thanks for your suggestions.

I’m trying to be polite with our swiss life agent because I was very upset after the information I have read on this forum about swiss life and their commercial behavior. During the last days I got more information about the evolution of our insurance. After 3.5 years we already lost 30% of our 3a pillar deposits because fees and other expenses. Of course the swiss life agent didn’t mention these fees when we signed the contract and they didn’t provide me any documents about it.

I could understand elevate fees for this product and the insurance could be interesting, in any case, for a swiss person that grown up here and will spend the entire life in Switzerland. For me, It doesn’t make any sense to offer this product to a 37y old expat (like me) that probably will not spend the entire life in this country. This is only a commercial practice and I I have taken the bait…

I’m waiting for the reply of my agent and I would like to book an appointment in order to re-discuss it. I hope I could save something…