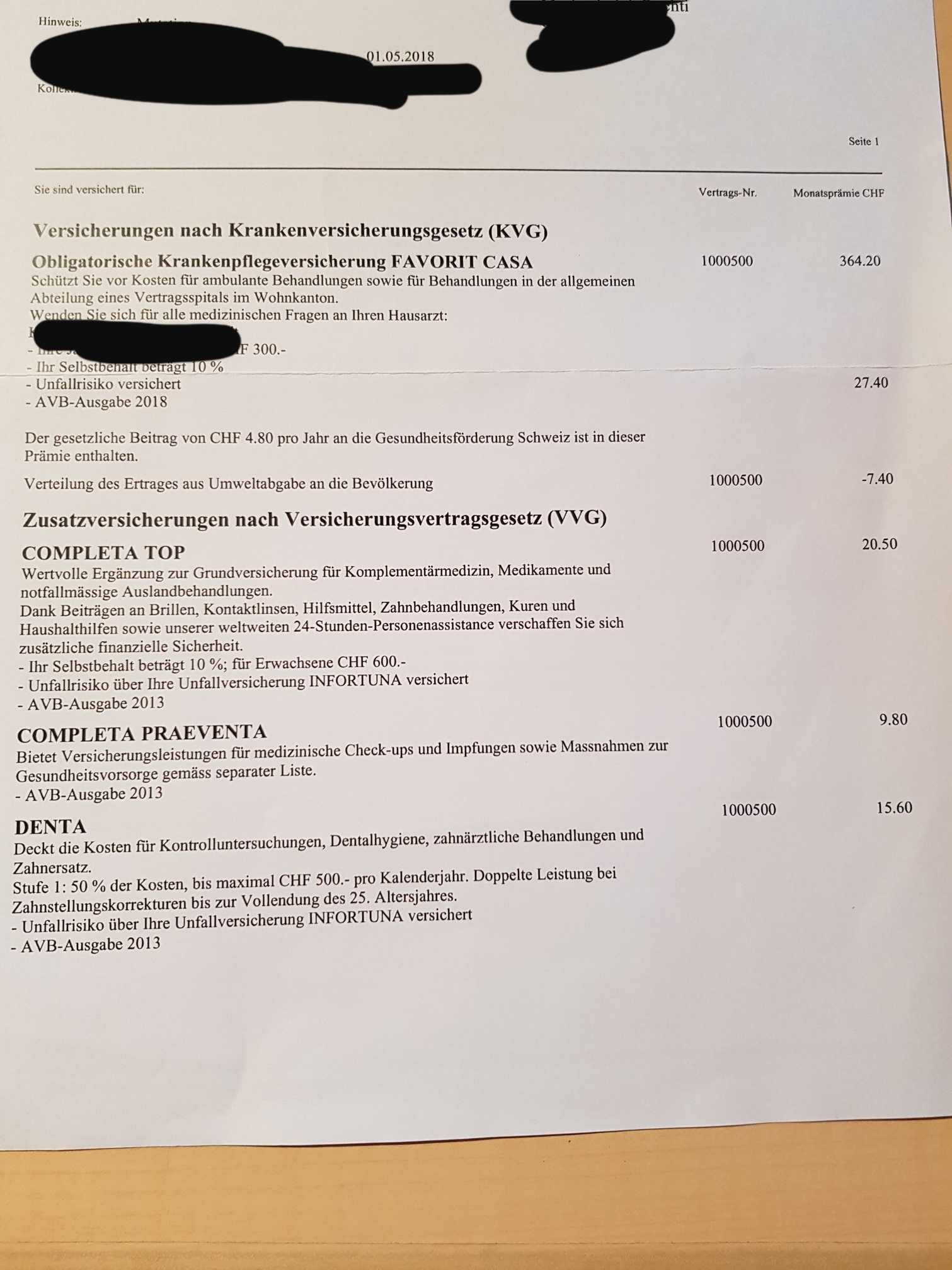

I moved out from home and still have a very expensive insurance policy which my family paid until now. My insurance company is SWICA, they’re awesome and I’d like to stay with them.

My franchise is at 300.- which doesn’t make much sense because I’m very young and healthy. I visit the dentist once a year for a checkup (+ occasional repairment.) I hardly ever go to the doctor, only when I have a small sports injury or vaccination treatment. Last time I went to the doc was more than a year ago…

!

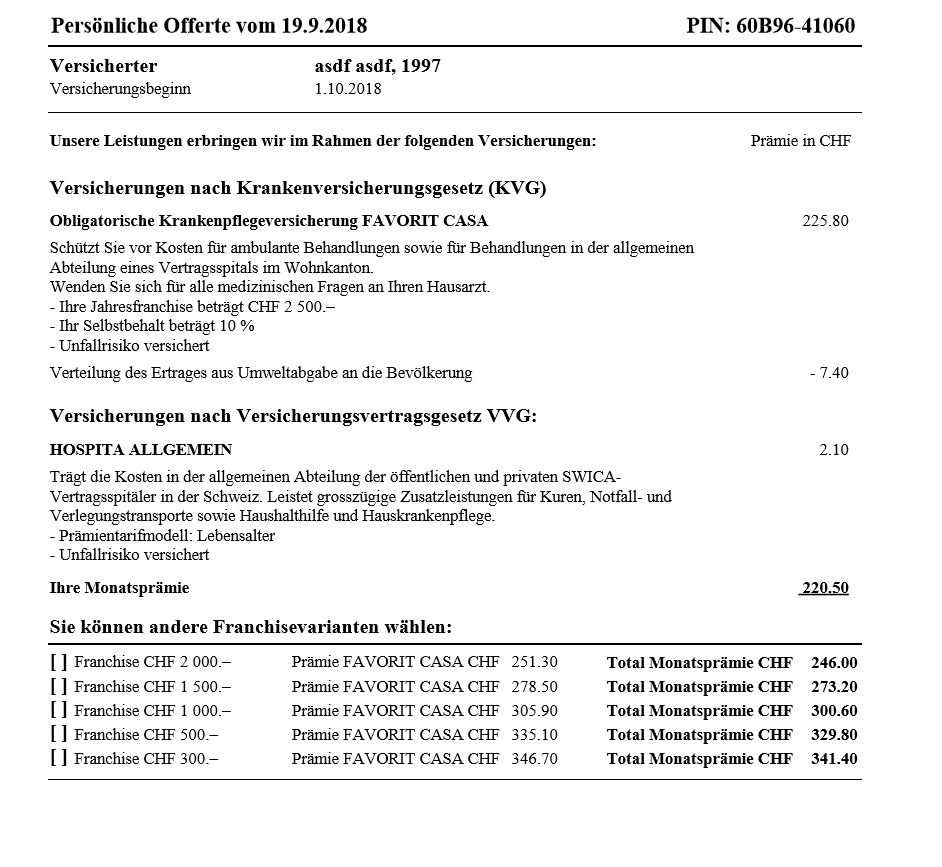

I could lover my general coverage from CHF 364.- to CHF 218.- a month by choosing a CHF 2’500.- franchise instead of CHF 300.-. I heard that the saving amount on high franchises will be cut back significantly in 2019, do you know more about this?

I’m using the “Family Doctor” model and liked it a lot so far. Which one are you using?

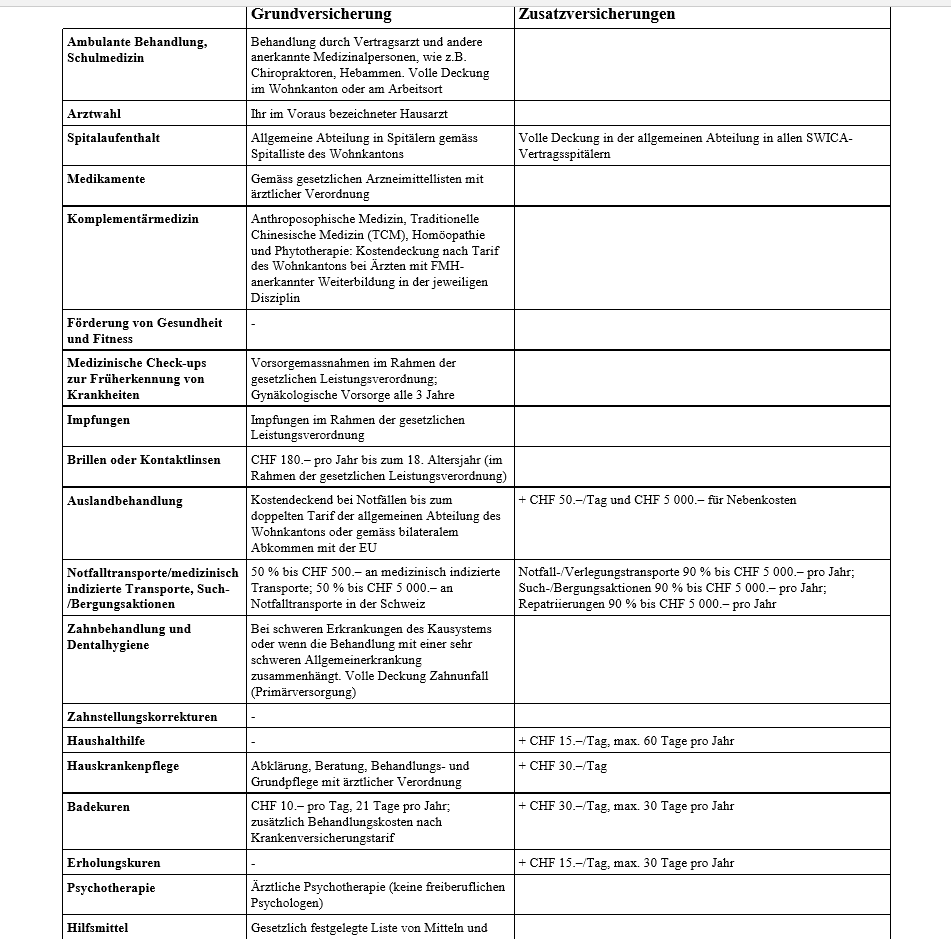

I currently have the following supplementary insurances selected, they cost around CHF 60.- per month. Link with information: Supplementary insurance plan – SWICA

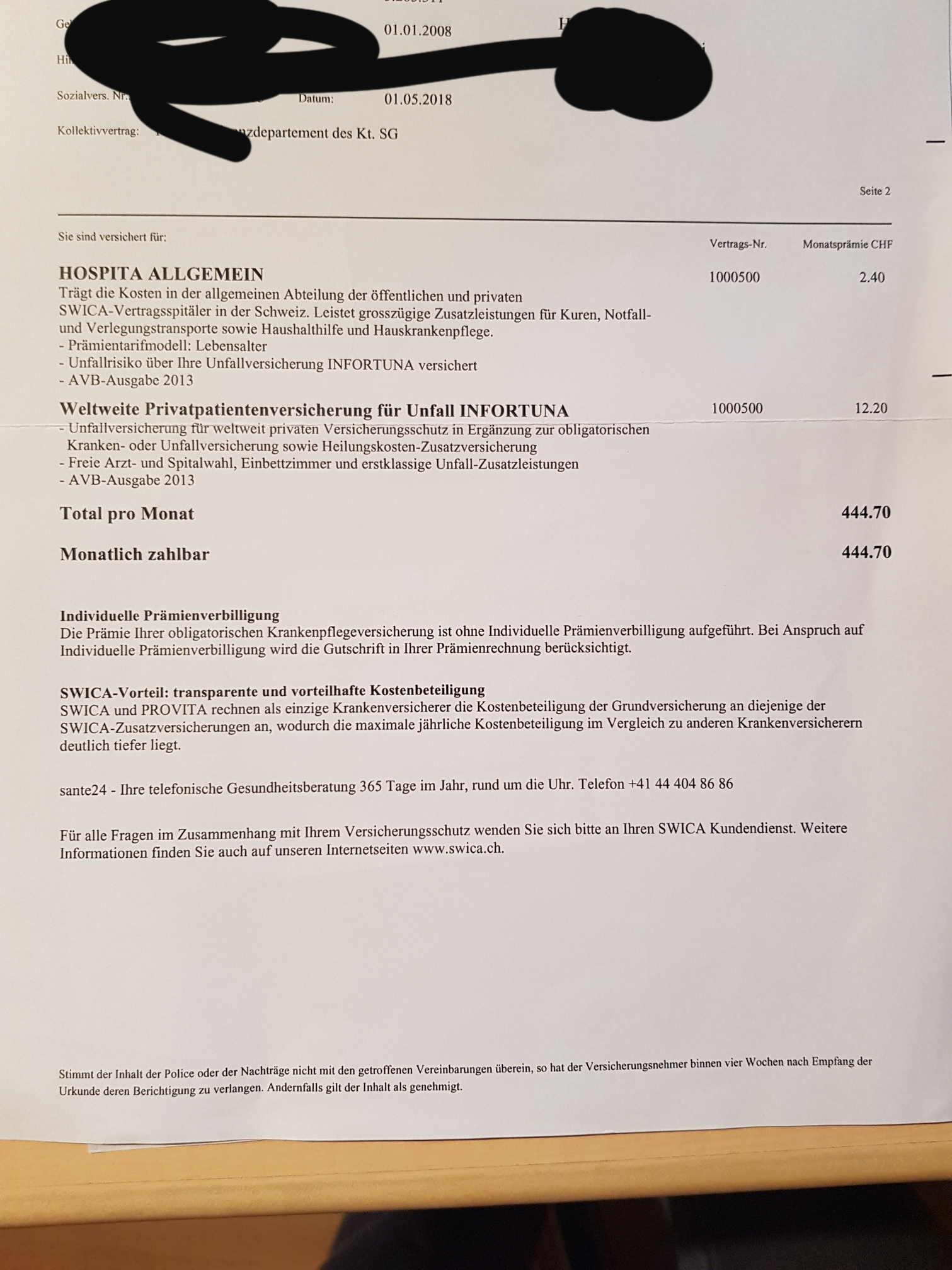

Hospita Allgemein → 2.-

Covers costs in SWICA approved hospitals

Accident Cover as a Private Patient - Worldwide → 12.-

Full cover of all costs when I have an accident worldwide.

Single bedroom and emergency transport coverage worldwide.

Full cover for the cost of glasses, medically prescribed aids and dental treatment Does this mean I can send every dentist bill and they pay it or is it just accident related?

Completa Top → 20.-

Emergency transport (already covered above!)

Homeopatic Medicine

CHF 200 for glasses every 3 years (don’t have glasses yet)

50% of Orthodontic Costs up to age 25

Benefits for prescribed spa treatments

Benevita Bonus Programm

Completa Preventa → 10.-

CHF 500 participation for fitness, nutrition & relaxation

CHF 200 for vaccinations per year

CHF 500 for preventive medical check ups every three years

Denta → 15.-

CHF 500 for dentist checkups and fixes

Which ones would you cut? I’m <25 and a student, can I get additional savings / benefits by saying this and that I want to pay yearly? The new policy amounts to CHF 280.- instead of CHF 445.- by increasing the franchise from CHF 300.- to CHF 2’500.-.

I’m currently still insured for accident with my employer but never took it out from my policy. Can this be done in hindsight?

Thank you very much for your thoughts! Apologies for asking so many questions but all of this is new for me.

I think I can relate to you. I had all the things you have listed above when living with my parents.

Here are my thoughts:

Accidents:

Each Health insurance iteam you list can either be had with accident coverage or without. Always go without! Accidents are covered by your employer like you said. Call your agent they should be able to adjust this.

Moving on:

Do it, take the 2500.- franchise. I am at Helsana and my Prämien actually went down this year. I was told this was because of my age and franchise (2500.-).

I dont know anything about saving on high franchises in 2019, its first I am hearing about this…

I have this also seems to help if you ever have an accident out of the canton you live. It might even be international too.

Accidents are always covered by your employer. Check with them. The only reason for having this is if your employer insurance is worse than what SWICA offers. Do you really need private eg. single room?

Take a look at what they offer and see if its worth it. Do you need glasses each year? Do you go to the gym? Do you go for massages? etc.

If not cut it.

Same as above, consider this: a medical Checkup will cost you maybe 150-200CHF. Is it worth it to pay 120.- year in prämien for a checkup every 3 years?

Not worth it if you ask me. I go to a dentist for a checkup and cleaning. Costs me less than the 180.- you are paying here.

Like I said these are my opinions. I am interested what other think.

This is a very good advice only for people employed somewhere and working more than 8 hours per week. Otherwise you must take the accident option in your health insurance. This applies especially to children and housewives.

As far as I know (or more precise, have been told by SWICA), they do not offer any discounts when you pay for the full year at once instead of monthly.

If you get new information, feel free to share.

The Completa Praeventa is worth it to me, as one gets 50% off the gym (you need to calculate whether it makes sense for your subscription, if you use one).

The downside is that Praeventa is only available on top of Completa Top, which seems pretty worthless for most of the points above.

Insurance companies are here to make money so chances that you will pay more than you will get out of the additional insurance are very high. Also those “ambulant” additional insurances only pay very limited, so usually really not worth it unless you can get more out of them than you pay in on a regular basis. (e.g. I pay 250 for my ambulant insurance but take out 300-450 each year, BUT this will change in a few year when I get older, so I will get rid of this insurance at that time)

Basic insurance is very good in Switzerland and pays everything that’s really essential everything on top is just comfort or it’s usually better to pay out of pocket. Also the way you are insured right now doesn’t really make sense to me. Why do you have Private Insurance for accidents worldwide, but if you get sick in Switzerland you will only get “Allgemein”

Also base insurance pays for hospital worldwide, but only up to 100% on top of what it would cost in CH. I would only take up a short travel insurance for the probably few times you travel to a country where this is of use, e.g. USA.

Saving for higher franchises will NOT be cut back in 2019 anymore, they reverted it.

What I would do:

Exclude Accident from Base insurance as soon as possible, afaik can be done each month, but cannot be done in hindsight

You are likely not going to the doctor so just use the cheapest available model (HMO or whatever) and highest franchise, you can change this each year if you don’t like it.

Get rid of all supplementary insurance, this includes Completa Top, Completa Praeventa, Denta, Infortuna. Only keep them if you are already getting more out of them than you pay in or will very likely do so in the near future.

Depending on the Canton you are in and available hospitals i might consider keeping Hospita Allgemein (So you can go to hospitals anyhwere in CH without paying on top)

If you want Private Insurance than consider taking up a “flex” model where you choose if you want to go in as a Private or Allgemein patient at the time you enter the hospital. They are reasonable priced and it might be difficult to get Hospital insurance later, when you become older. You can also include private accident there.

Rant mode: Also don’t just stay with an insurance company because you believe they are “awesome”, other companies are just as awesome. That’s the same sentence I have to hear over and over when people are overpaying for their banking packages at UBS or CS without getting anything out of it. /Rant mode off So my advise: Compare premiums with other companies once the premiums for next year are out.

Just be aware that this is my personal opinion and I only take up insurance that I really deem worth it.

Thank you very much for the fabulous replies! I learned a lot about health insurance thanks to you guys and realized that I (and my family) can optimize many things. I can cut down my costs from CHF 445.- to CHF 230.- so thank you very much. I should invite you for a drink

The only supplementary insurance I want to keep is the Hospita Allgemein for Switzerland. I have a few more qustions about the others:

Halbprivat Flex --> Do you guys have this? I don’t mind being in a room with several people but in case that I have to go to the hospital (which would e.g. be a car accident, knee injury, sports crash) it would be important to me that a well-trained specialist performs the surgery. For example my girlfriend had her miniscus torn and went to a special clinic in Zurich for surgery. Would this only be possible with Halbprivat?

Which base model are you using? (house doctor, Telmed, pharmacy, health center) I could save CHF 180.- a year by choosing a pharmacy instead of a house doctor but I’m not sure if that’s worth it.

When I go to e.g. Germany or France for a day and have a car accident there, would I be at a disadvantage without international coverage? Because a travel insurance wouldn’t make sense for these short trips.

Do you have the “Gesundheitsrechtsschutz” (Health law protection) for CHF 30.- a year?

Your main quoted potential hospital visits are due to accidents, which is outside health insurance! That is covered by your SUVA plan (via employer). I know mine pays for full private, check what your employer pays for.

I use Telmed, where I have to phone to get “permission/ok” before going to Doc. Never been refused. I guess they try convince u otherwise if u wanna see the third specialist in one month or sumtin.

International not required. U covered to Swiss prices, which as we know are the highest (except maybe USA).

Law protection - no, I have no need for this, nor plan to. Taking doc to court doesn’t happen here. And if it’s about a very high bill, the health insurance will fight it “for you”.

As for me we use the “family doctor” model. It means you have to go to your usual doctor before going to any specialist doctor (except eye doctor or gynecologist). I’m not going to any specialist by myself anyway, so I don’t see the point in not choosing “family doctor”.

For example, I had a pain in my hand and went to him. After checking things he took an appointment for me at hand surgery specialist. How could I have find out this specialist by myself? Eventually the surgeon found a very small glass shard in my hand…

Last New Year (so no way to go to the family doctor) my wife fell suddenly ill and I went with her to an emergency hospital. After waiting three hours it appeared she had a pneumonia. The total bill: hospital, chest X-ray, antibiotics, anti-antibiotics side effects (don’t laugh… she has a weak stomach) was about 1’000.- There was no problem with the insurance since it was during a holiday. I don’t know what would happen if you go to an emergency hospital for a simple cold.

And last medical story, several years ago I had an accident and was brought to a big hospital. After some time they put me in a big room with three (? with morphin I don’t remember well) other people. It was horrible: an old woman who didn’t understand why she was there (obviously she had a strong dementia problem) and kept urinating in her bed… another one calling the nurse all the time and insulting her… long story short I took a private insurance for us. If I have to stay several days in hospital I don’t want this again.

You can always upgrade to private room by paying directly to the hospital. In the long term it’ll likely be cheaper than paying for it through a supplementary insurance.

Thank you for your answers I asked my employer what kind of coverage he has but he didn’t know, LOL. His company is insured with AXA.

Since I’m starting university now I’ll work less than 8 hours per week and have to take care of accident insurance myself. I’m going to the US for two weeks in January. SWICA covers costs of international treatmens up to twice the sum of what it would cost in the respective Swiss canton hospital plus CHF 50.- per day / CHF 5000.- through “Hospita Allgemein.”

Now, if I have to take a surgery in the US, will it be hundreds of thousands of $ or is it going to be within twice the costs + CHF 5000.- of Swiss hospitals?

This would be my ideal Swica (I’ll look for other companies too) variant so far:

With this variant, I’d be at CHF 220.- compared to CHF 445.- (!) what I’m paying now. Is there anything missing? I could change house doctor to medpharm (pharmacy) to save another CHF 17.- per month.

It’s not just SWICA, by the way, it’s guaranteed by the law, I guess. Even my cheapest Assura insurance has the same coverage for international treatments and if I want to have no limits then I need to upgrade to MONDIA for sth like 5-8 CHF per month.

Alright, good to know that US Healthcare really is expensive. It’s time for me to send in the documents to SWICA (I’ll stay with them as of now.)

Swisscare doesn’t list anything for the USA unfortunately. I’m going to take the Swica worldwide private hospital coverage “Infortuna” for 12.- a month:

Here is the full rapport:

You can use this PIN to access the offer: 6A-DS-C9

Partner Pharmacy instead of House Doctor (is this fine?)

In my opinion yes, you will just have to go to a pharmacy first, if there is something wrong with you were you should see a doctor they will send you to a doctor. This is just to avoid doctor consultations for simple stuff where a doctor visit is not even appropriate. If you don’t mind this - go for it.

Infortuna

Personally I would not take this on. CHF 12.20 per month is way too expensive and this will only be needed in countries such as the USA. Also if you travel to the USA and suddenly get sick very badly and need emergency treatment this will not cover the cost, as this only covers Unfall and not Krankheit.

In most countries where health cost are just a little bit higher or even lower than in Switzerland you don’t need this as basic insurance already covers up to 2x the swiss cost. This is not sufficient in only a few countries. (mainly USA, Canada) If you only travel to the USA lets say once per year for a few weeks or even less it’s cheaper to just take up a one time Travel Insurance every time you travel there. For example this one here from Atupri: (you don’t need to be with Atupri to take this on) https://www.atupri.ch/de/private/versicherungen/reiseversicherung

Will cost you e.g. CHF 22 for 15 days, this covers Unfall and Krankheit and it will take less than 3 minutes to get. (completly online)

Thanks a lot! This would be perfect as I’m going to the US for exactly 15 days. Is it necessary in the US to be a private patient? Atupri would probably only cover basic.

You are not guaranteed the highest possible available comfort. But they will cover whatever is common in the country. So Private supplement is not necessary.

Thank you Thaek! I am sending in everything tomorrow

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.