Kindly asking for an opinion on the following. Is there a way to get a Value Factor portfolio on Finpension, considering the only fund available is CSIF (CH) III Equity World ex CH Value Weighted - Pension Fund (CHF hedged and non-hedged), where the allocations are different compared to a standard value factor ETF?

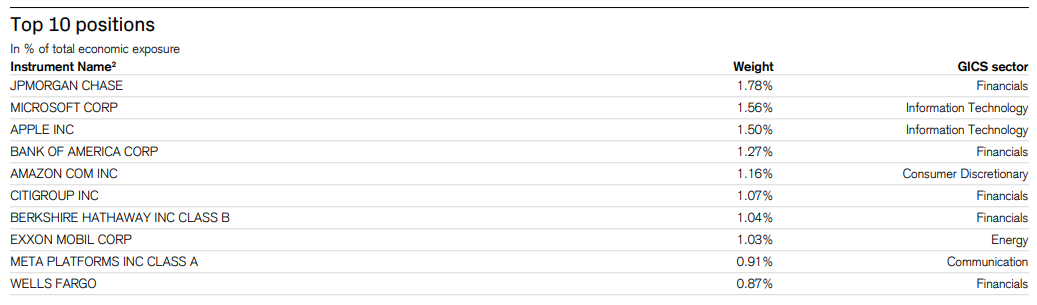

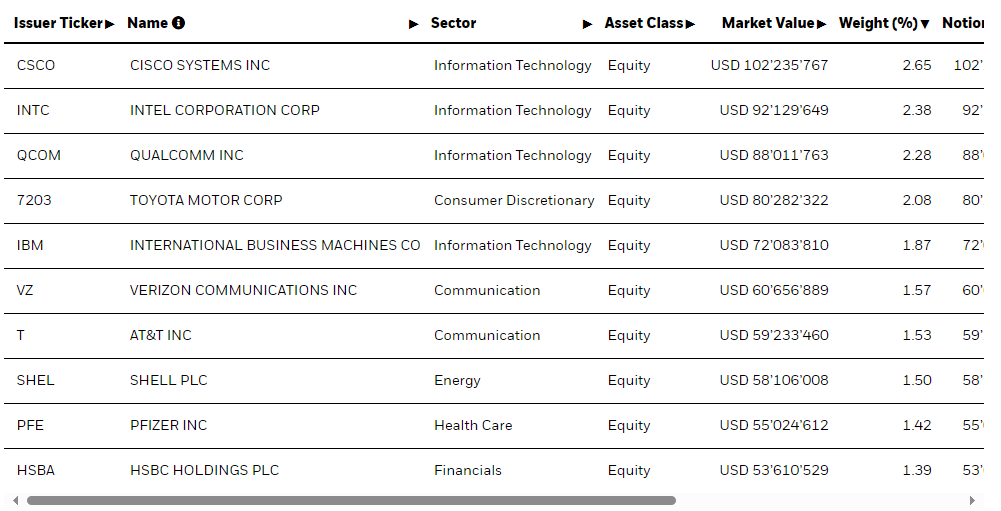

Please find below a comparison of top 10 positions.

MSCI value weighted (VW) index is different from value / enhanced value factor indices. VW contains all the companies in is benchmark (just with different weights than market cap) unlike value or quality or min vol that have fewer components.

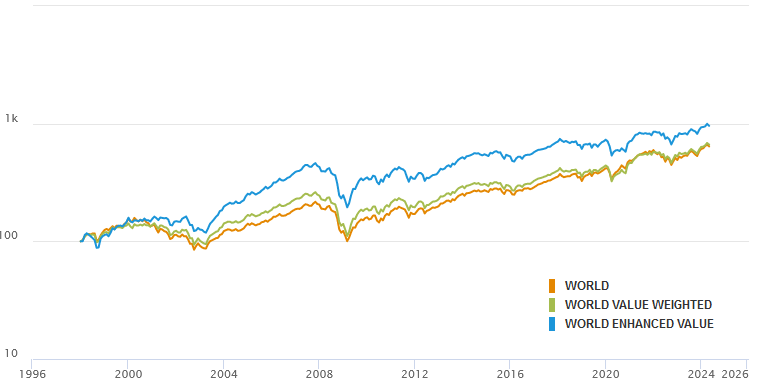

EDIT: “WORLD ENHANCED VALUE” is a much stronger tilt. It had nearly 50% more total return over this almost two decades. Though, careful with indices. Their inception date is much later than the backtested data suggests.

I think it‘s a nice option for someone not deep into factor tilting and as a majority holding in the portfolio. Most people can‘t handle much tracking error.

A nice lightly tilted 3a portfolio could also be 50/50 value weighted and quality. Value is premium is relatively anti-correlated to profitability (pretty much quality) premium

3a will shield your income tax from dividends for time being but eventually you will need to pay withdrawal tax. Assumption here is that value stocks will outperform standard allocation. Hence the net return for value stocks should be more than rest of the investments.

So what would be better depends on following

withdrawal tax rate

dividend rate + capital gains return

overall return

marginal tax rate

wealth tax rate

You might be right but I think one should do the math.

Yeah, I agree. Like the counterintuitive result of 0% US withholding tax for pension funds. You can already get full tax credit for the normal 15%. So better prevent additional taxes where you can’t. The dynamic might change if non-3a Finpension manages to get tax credit on IE ETFs (and this will start to apply to dividends from all countries).

I do own these factor ETFs with my broker, yes. Factor tilting is just a part of my overall target portfolio allocation and with Finpension anyway just a small yearly amount that gets in here.

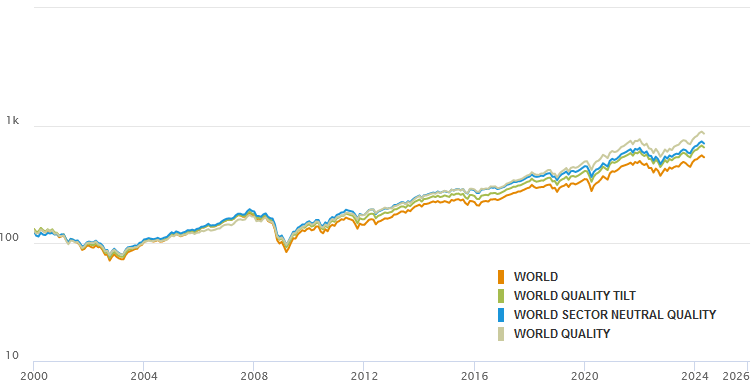

Qualitatively, nothing much for Quality & World. Value loses a bit. Additionally Net is missleading where you have DTAs and tax credit (at the very least with high US concentrations).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.