I can’t find the link anymore. But everywhere they make examples of the 90/10 portions. 90% is the collateral. If the counteparty fails, the ETF remains with 90% of the value. What happens then?

People might want to sell the etf and the provider has to sell part of that 90% to cover the costs? Maybe that 90% is losing value because the counterparty failing is probably generated by a bigger crisis?

The rule seems fine if the counterparty might fail on its own but if there something happening then the ETF value might go to 0.

The article is very much obsolete, and with a Canadian focus. EU regulations changed a lot over the past 15 years. Therefore, little of it is still relevant today for UCITS funds.

I would not focus too much on the 90% because in practice, the synthetic funds tend to be overcollateralized.

What do you mean by “better”, Saxo has worse performance? The difference is because of higher TER, higher buying fees, stamp tax, loss in withholding tax, and lower income tax. XALL on IBKR is ~0.2 percentage points better than on Saxo for the 20y performance difference values above.

Yes that’s the idea. They go ask a bank or similar “hey I have all of those can we make a deal where you give me the returns of this index, I give you the economic exposure of the collateral”.

The bank will typically hedge it so it’s risk neutral for them.

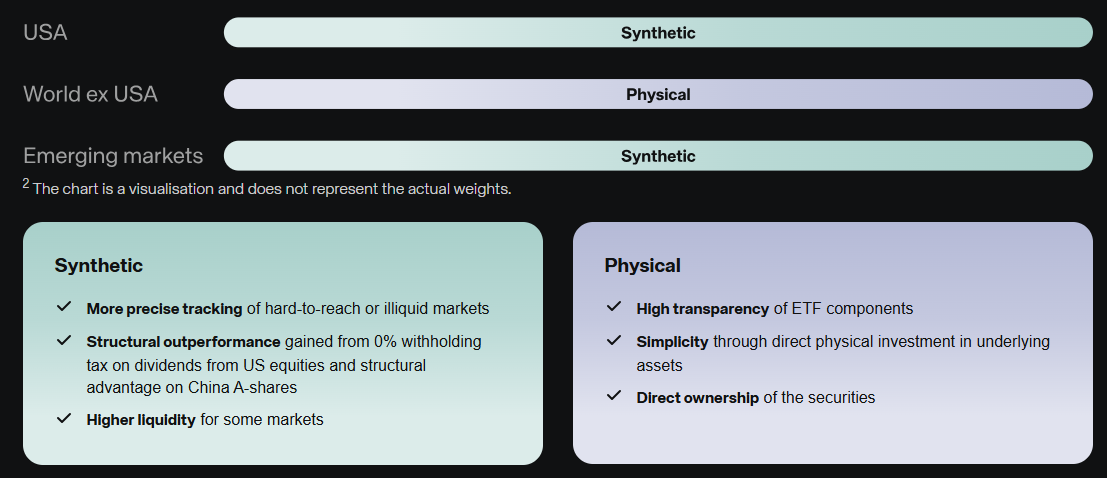

There is no bet. The fund retains legal ownership of the collateral. The unfunded structure means that:

Collateral is held in the ETF’s own custody account

Investors have a direct claim on those assets

Counterparty exposure is the difference between collateral value and index value

UCITS rules cap swap counterparty exposure at 10% of NAV but in practice most providers “reset the swap” daily, and as I said, synthetic funds tend to be overcollateralized. So real-world exposure is usually negligible.

Reading thought this discussion make me realized why I was so attracted by Bitcoin in the first place. Extremely simple, transparent rules, very low (almost no) risk of rules change, no geographical impact, no direct political impact, more importantly non dependency on anyone else.

I opened a IBKR for diversification, but I’m anyway forced to have exposure to stock market with 2nd (not controlled) and 3rd pillar (controlled), now I’m wondering which additional exposure I want to add on top and which part should be risk free from all these political decisions and geopolitical wars.

Bonus, with the current low price of Bitcoin, it’s the perfect entry point to rebalance toward it. And when these new rules will be applied, I will have to decide what I do with the rest invested in US.

I was under the impression that Swap costs were typically very low for major developed market indices. Tracker X500 has a TER of 4 bps, therefore Swap costs should be around 1 bps maximum, no?

I imagine they could be bigger for the emerging markets sleeve, but that’s roughly a tenth of ACWI.

Afaik similar to hedging “costs”, swap “costs” (if you don’t include the transaction fees on the provider side, but were thinking of things like spread etc) are not included in the TER, it’s part of the overhead of the swap itself.

That said https://etf.dws.com/download/asset/6ee6a5b2-d799-4f7d-afa0-568c770bd08c only has example of positive spread (in favor of the fund). Either due to outperformance on withholding tax or due to the equivalent of security lending (eg it allows people on the other side of the swap to short hard to short shares).

You are right. I just compared two funds tracking S&P 500 Scored & Screened Index and the synthetic one outperforms a tiny bit more.

By the way, I am pretty amazed by the profusion of funds available in Europe today. We have access to UCITS funds, including ESG-screened funds, for as low as 3 bps!

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.