Whats the time frame of this calculation?

25 years

1 Like

What’s the growth assumption for the funds in this example?

All at 5%

Talking about complexity, most people forget „tax complexity“. This especially when you are in years 15+. Its a Problem when the Portfolio all off a sudden „causes“ people to pay huge taxes that they probabbly just can’t „afford“. Therefore, my set and forget solution for people that are too lazy and don‘t care is always using CH domiciled funds. Reason beeing is that even theasauring ones already and automatically deduct WHT. Meaning that people generally don‘t need to „pay additional taxes“.

Therefore, I only see Viac Invest for People can deal with apps and daily NAV, or Avadis for others that better don‘t even see the volatility.

All others, IE ETF based solutions cause issues that make people drop their investments. Its better when they invest with 0.2% more TER and 0.2% more tax drag from CH funds, than if they simply give up investing goven their tax declaration challenges…

1 Like

Are you talking about income tax on dividends?

Why would there be a “sudden” jump in taxes? It would build up continuously over the years.

2 Likes

That was worded poorly from my side - its not a Jump as such. The frog is grafually getting boiled until the point off realization and acute pain was ancountered

Still - take Hans Muster, earning 85k, thereof investing 20k p.a. in UCITS ETF. After 20 years, his „Tax Bill“ will be double the one of his Twin that doesnt invest. It may be so high that he can’t even safe much going forward. He eventually stops to invest, potentially pulls out money or even sells it all.

Now clone him and make him invest in Swiss Funds instead. His Tax Bill will be constant and it may even drop as the 35% WHT was too high. He will have a fundamentally different experience and investing will be much smoother for him.

Tax Complexity can become a material differentiator - but this only after a few years. This is why I, for Hans Musters that want set and forget, always recommend CH domiciled solutions. Viac Invest beats Avadis (at least on paper) so for people that manage to not open the App on a daily basis, I no longer recommend Avadis but Viac Invest. If they don‘t get taxes, they could simply put the year end wealth in the declaration, without looking up ISIN‘s and the like, and their tax declaration was fundamentally ok (unlike the UCITS Twin that when doing so grossly omitted income tax).

Yes, its performance is worse that YUH with VWRD, Neon, IBKR or potentiallly even Finpension Invest. But they rather keep beeing invested in an Ok solution, than starting in a great solution that confuses them and where the for sure drop out by year 15+.

1 Like

After 20 years Hans would have a 700k nest egg, so about 14k extra income.

At a marginal tax rate of 25% that’s about 3.5k more in taxes to pay.

Since he will still be able to save 20k per year, how won’t he be able to pay the surtax plus still save a good portion of the 20k?

Even if he stopps to invest (why would he?), he would still be off much better than his twin.

3 Likes

Sorry but I am not able to comprehend. In both cases the same tax liability occurs. Is it not?

35% or not, the tax return will need to be filed.

This reminds of people saying they’d rather not earn or own more as they’ll have to pay higher taxes.

8 Likes

Heard that statement a few times as well. ![]()

However @TeaGhost makes a good point that some people will not (want to) comprehend that the best solution is really best for them long-term. And isn’t it better to get them on @TeaGhost 's decent/easy, though tax-wise “not perfect” plan, rather than they fall into an “easy” investing trap with an insurance company and the like?

But yeah, one could also switch all of Hans Muster’s funds to Swiss Funds only once this perceived tax burden becomes an issue for him. The sell/buy fees won’t be crazy (if at IB), and capital gains tax isn’t hindering him to do this in CH either.

„Effective“ Tax is the same, with IR or CH Funds. „Felt“ Tax not. It makes a huge difference if the Swiss fund (when accumulating) distributes WHT that doesnt appear on your account but directly goes to the tax authorities - vs if you need to sell securities to pay taxes.

Hans Muster that was less informed, aware and willing to learn will not see the „Effective“ tax. He will only look at how much he needs to pay (without realizing his funds already payd a chunk beforehand) aka he only sees the „Felt“ tax.

Remember: CH Accumulating Finds will every year send 35% of the thesaured dividends directly to ESTV, and you won‘t even notice that.

1 Like

Tax Liability => yes

Tax Filing => not nescecarily, could be ommitted / simplified to only show / declare wealth

Actual Taxe Bill / Taxes Due => No

Every time the Portfolio causes pain and action was requires, comes with a risk of Hans Muster just giving up on investments or falling trap to anexpensive advisors. Set and forget is the best, even if not 100% tax efficient.

2 Likes

So is this just an assumption of yours, or is that something that’s actually happening?

Because I’m not so sure that people who are enough well off and intelligent to save up a substantial nest egg will go “this thing I’ve been doing made me rich but I also need to pay a few k in taxes, I’ll stop”

4 Likes

It’s the 1st time I heard about that theory.

In Switzerland, we pay our taxes by installment. It is straight forward to adapt them and cover the extra tax on financial income.

Let’s look at a portfolio of CHF 700’000, generating an annual gross distribution of 2.5%

Marginal tax rate: 30%

Wealth tax: 0.8%

| IE | CH | |

|---|---|---|

| Gross income | 17’500.00 | 17’500.00 |

| WHT | - | 6’125.00 |

| Net credited | 17’500.00 | 11’375.00 |

| Wealth tax | 5’600.00 | 5’600.00 |

| Income tax | 5’250.00 | 5’250.00 |

| Total tax | 10’850.00 | 10’850.00 |

| WHT | - | -6’125.00 |

| Final tax due | 10’850.00 | 4’725.00 |

In both scenarios (Irish or Swiss based instruments), the monthly installments shall cover the extra taxes due on the portfolio. I don’t see the tax burden issue for Hans Muster. Having to adjust his monthly tax installments annually ?

1 Like

What about Saxo & AutoInvest & “Wertpapierleihe” ?

You can buy

iShares MSCI ACWI USD Acc UCITS ETF (SSAC_CHF)

Custody Fees: 0%, Buy Fees 0%, Sell Fees 0.25%

Invesco FTSE (it’s not in the AutoInvest Programm, you have to buy normal prices:

Custody Fees: 0%, Buy Fees 0%, Sell Fees 0.25%

You’re right, I’ll need to update the first post and include Saxo.

But one can argue if a broker (applies to Swissquote as well), with all its complexities, is really the right thing if a non-expert (so not us) is looking for a hands-off solution. It’s just way too complicated compared to something like finpension.

Please let me elaborate. Zurich based, Single, Catholic Hans Muster that earns 85k pais about 9k in Taxes. When he thereof invested 20k per annum, he would after 20 years probably have investments worth 700k. A realistic (these times are extraordinary) dividend yield was 3.5%; so he would have an additional, taxable income of 25k.

If he invested in IE ETF, the tax Administrations. would send him an invoice of 15k, instead of 9k that he had to pay if he didn’t invest. If he invested in CH Fonds, the tax administration would send him an invoice of 7k. This as the WHT of 35% on the 25k Dividends was too high.

Trust me, the figure that the tax administrator puts in his annual love letter - that figure is known, understood and hated. It makes a huge difference if Hans Muster receives a bill worth 7k or 15k.

This is not about tax optimisation, this is simply about the story how taxes present themselves to Hans Muster.

Viac in my view is on the right track and Finpension, Findependent and Truewealth just don‘t fully comprehend their customers (financially illiterate investors). So even though there are things I don‘t like about Viac Invest, chances that they will succeed are signifficantly larger than any of the ETF based Robo Advisors.

1 Like

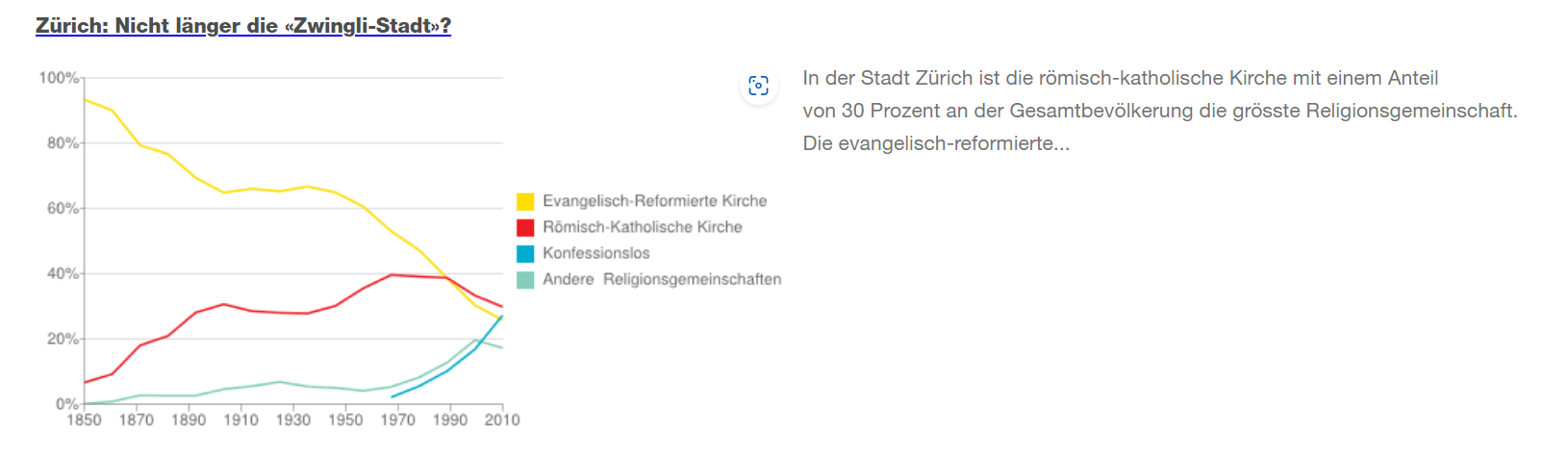

Sorry, not trying to derail, but I stumbled across John Doe in Zwingli-Stadt Zurich being a catholic… I think not. ![]()

Please carry on with your original converstation.

Edit: Actually, I stand corrected after satisfying my own curiosity:

(source)

Still finding it somewhat funny that John Doe in Zurich is now a Catholic. ![]()

3 Likes

Catholic pay the highest tax, that was just to boost the figures a bit upwards ![]()

But wow, didn’t anticipate that catholic actually was the right choice for Zurich lol

2 Likes