Musk dreams up to do something. Musk puts his prodigious intellect, cash and focus on that something, achieves it, then gets bored and moves on. That’s about it in my opinion.

I’ve been following him for a few years, in particular the neuralink and starlink stories, I think this is what really floats his boat. Will certainly buy into either when they become public.

Valuation for TSLA has been a strech for a long time, especially comparing it with “legacy” automakers (which do in fact quite well in terms of cash flow generation). I believe TSLA will face headwinds as long as Musk is not fully and in his entirety focussing on TSLA (and not on X, Space X, external AI company, etc). am very pessimistic in the short term. Sell

I understand your comments. But I don’t think it’s fair to say that an almost 2 Trillion dollar company doesn’t know how to build business or doesn’t have business focus.

Heck, I think Steve Ballmer would do a better job - he wouldn’t necessarily be very creative, but he’d at least squeeze the juice out of the existing assets.

I’m not sure that you even need a leader that understands the technology - you just needs someone to push things along. Google should already have their self-driving technology in millions of cars - maybe not fully self-driving, but at least doing basic stuff and collecting data for them to develop AI and building out sales channels.

Google is too cautious and too theoretical/idealistic. OpenAI just took their lunch and ate it in front of them and Google are still floundering.

It’s lucky that they have their core advertising monopoly. Lucky for them that continues to bring in money. And lucky the regulators don’t understand the business either, else they wouldn’t have allowed them to acquire DoubleClick etc.

It amazes me that the FTC wasted time on nonsense like the MS acquisition of ATVI when they should be busy breaking up Google to separate the ad buy side, sell side.

Talking about google, I am very pessimistic about their outlook. They were leading the field a few years ago but I feel them falling back big time. Search will be disrupted in the next 5-10 years (AI enabled search & advisory). Advertising will get under even more pressure (data protection & Apple), their office suite sucks as they just don’t solve bugs in time… so what is left? Cloud but there we talk about a commodity business with low margin and fierce competition. So what is left for Google - youtube?

Over the next five years I’ll take Microsoft any time against TSLA.

I don’t expect an incredible performance from Microsoft (best case maybe 15% per year seems reasonable). But all it has to do is not to implode the way I expect TSLA to do.

As of this writing:

TSLA : $157.46/share

MSFT : $412.58/share

For those having difficulties making up their mind, I have a hammer called FASTgraphs and to me every problem looks like a nail.

Hence here’s some FASTgraphs taking into account analysts’ earnings estimates for the next couple of years for the magnificient 7 and the end of 2027 price target if each company stayed at the multiple of yesterday’s close:

Damn, I knew there was a catch, even if you take the analysts’ estimate for granted.

So, which horse should I bet on, based on the charts? Is the bet still open, at all?

Without the fee (ok, even with the fee) I’ll say this: this isn’t my terrain, as it seems pure speculation. I try to stay away from investments or even bets where I can’t build my own and enough conviction.

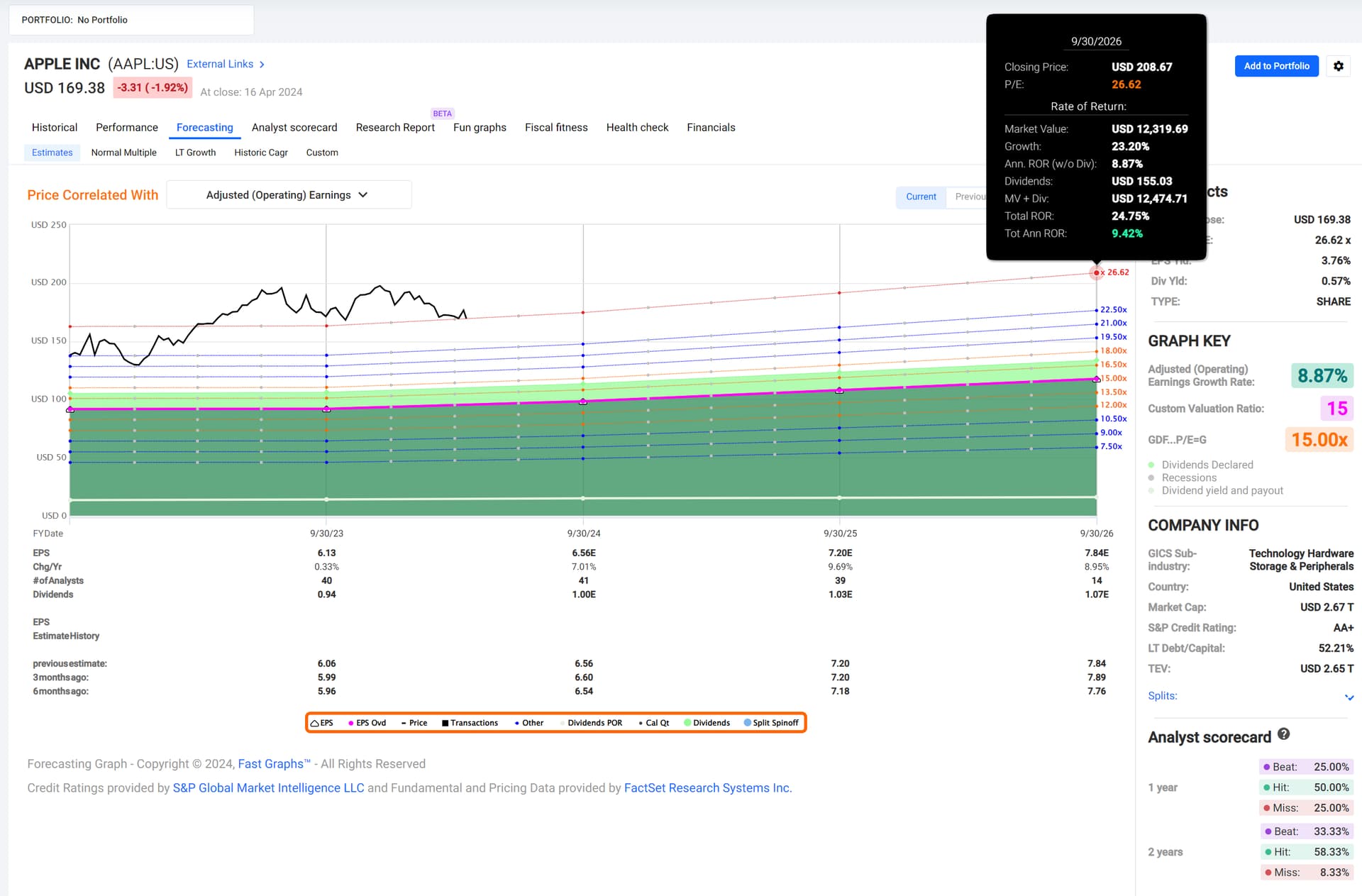

Apple’s too expensive for their expected growth. The appropriate (P/E) multiple for their growth is 15, and they’re at 26.

Pass.

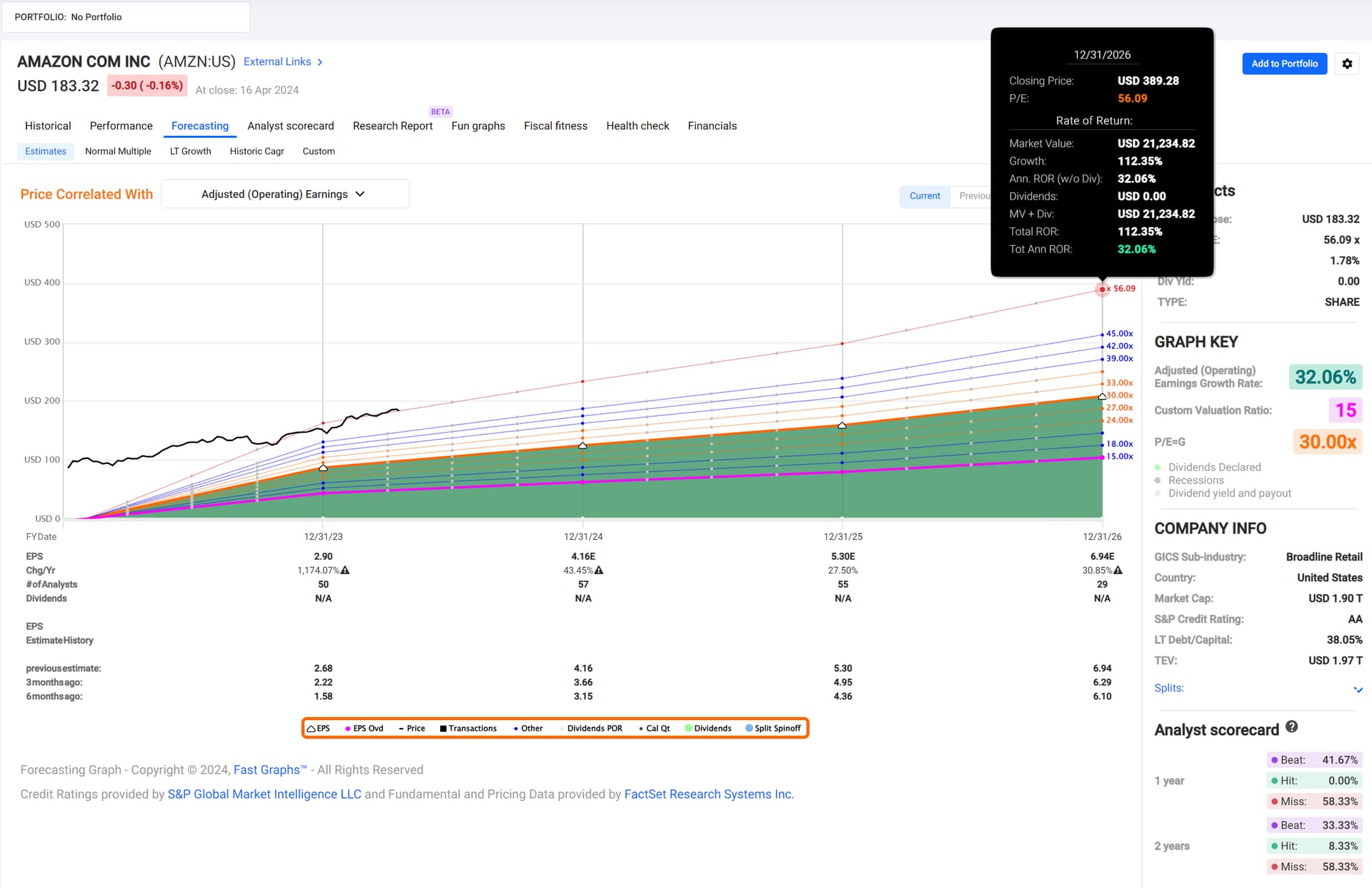

Amazon’s growth look spectacular, but even for their appropriate multiple (30), they’re overvalued.

Pass.

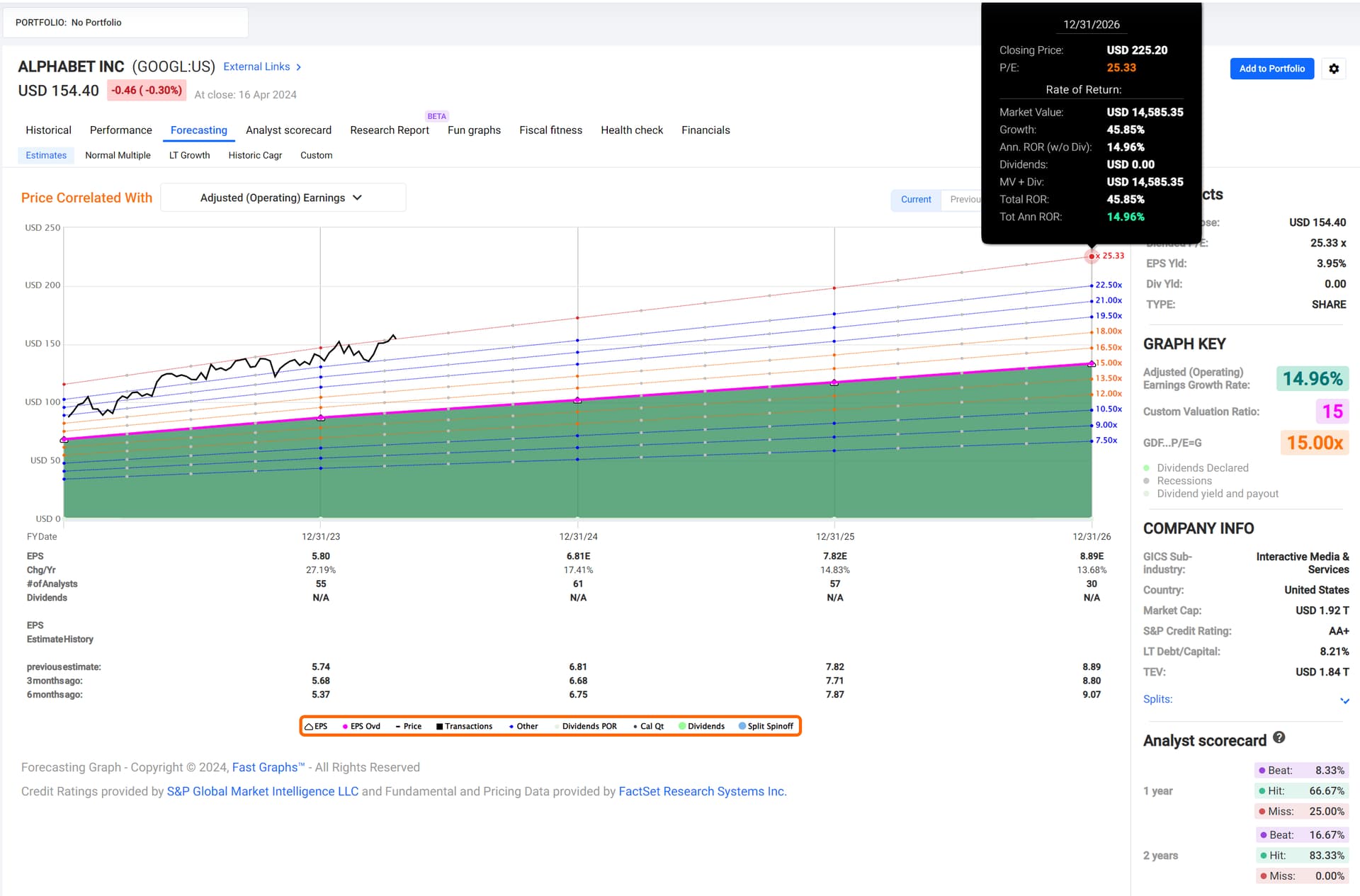

Alphabet’s case is the same as Apple’s (plus the concerns mentioned above).

Pass.

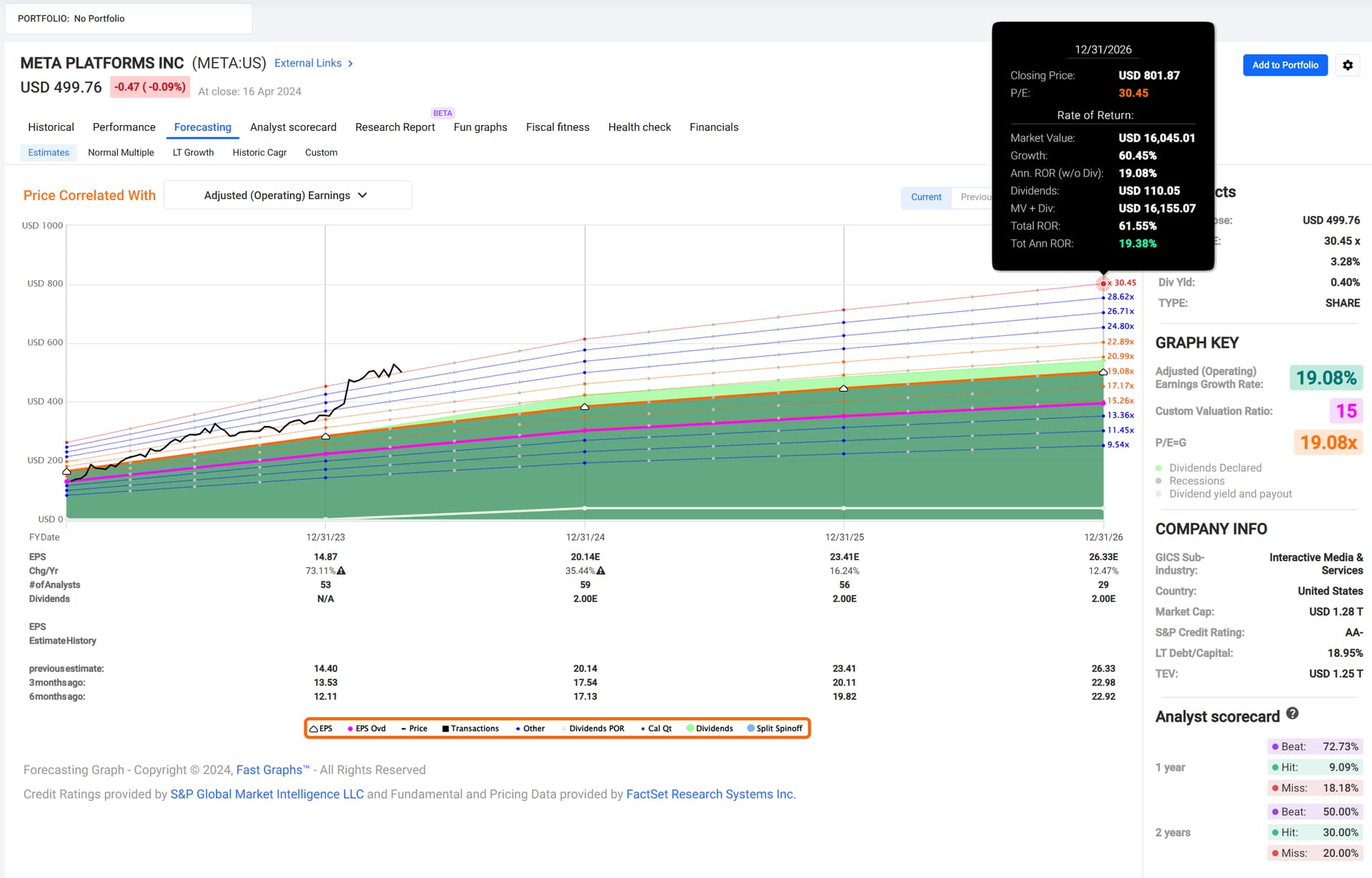

Meta’s growth justifies an about 20 multiple, they’re at 30. Overvalued.

Pass.

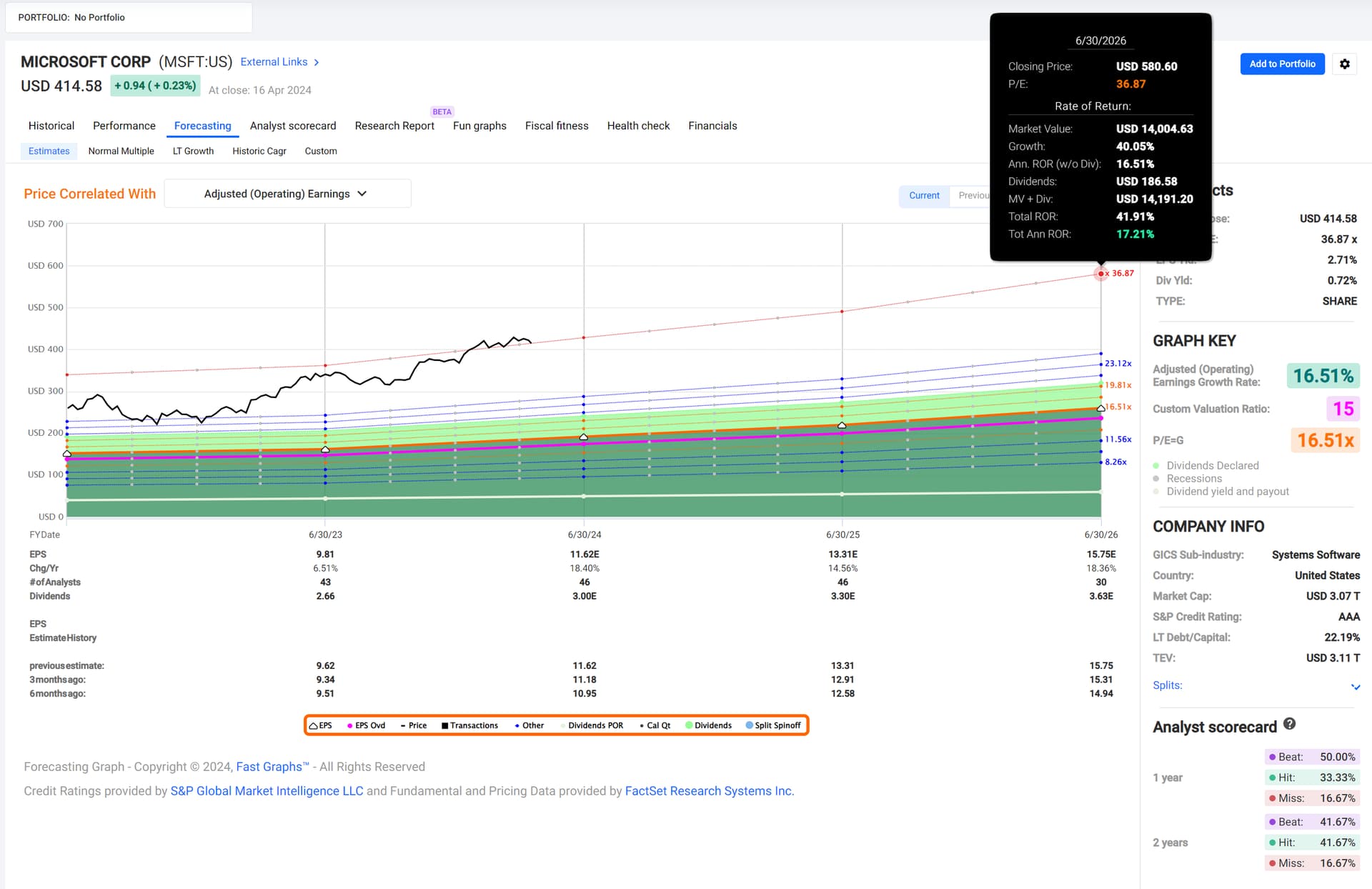

Microsoft’s growth justifies a 16.5 multiple. They’re at 37. Overvalued.

Pass.

Nvidia’s growth justifies a 30 multiple. They’re at 57 (!). Severly overvalued.

Pass.

Taking into account that Tesla’s almost as overvalued as Nvidia but has no real growth to show for, I’d probably tag along with @Julianek because of M$'s moat and even ignoring the AI hype intact growth opportunities with Cloud. They feel a little bit like they’re becoming a Coca-Cola, established brand, an even better moat (good luck moving corporate America and most of the rest of the world away from Windows and Office) and investors are willing to pay a premium for the company.

I’ll bet on Apple, then. If multiples don’t help, I apply an alternative method: From the products and services I use(d), the ones from Apple caused me the least frustration. Excluding Tesla, I don’t drive one, yet.

Given the timespan of the bet (5 years) and the average user turnover on this forum, there is too much risk that any of us won’t be there in 5 years to honor this bet.

What I suggest instead:

Let’s do a 5-year swap, settled monthly, on the relative performance of MSFT vs TSLA

notional of the swap is 100CHF

Leg 1 of the swap is Microsoft performance, dividends reinvested

Leg 2 of the swap is Tesla performance, dividends reinvested

initial fixings for both stocks is a written in my former message (TSLA: 157.46 USD, MSFT: 412.58USD)

Being long the swap means receiving MSFT performance and paying TSLA performance. Being short the swap is receiving TSLA performance and paying MSFT performance.

The swap is settled monthly and expires after 5 years. Both participant can choose to exit the swap during its lifetime after having settled the past month performance.

Example:

Bob is long the swap, Alice is short it.

on month 1, MSFT goes up to 433.21 USD and TSLA up to 163.76 USD. Compared to the initial fixings, that’s 5% for MSFT and 4% for TSLA. Netted, this is a 1% relative perf for Microsoft. Alice pays 1% of the notional, i.e 1% * 100CHF = 1 CHF to Bob.

On month 2, MSFT goes down to 420.83 USD and TSLA goes up to 165.33 USD. Compared to the initial fixings, that’s a total perf of 2% for MSFT and 5% for TSLA. So a net advantage of 3% for Alice. But because Alice had paid 1% in month 1 to Bob, Bob has to settle 4% of the notional to Alice.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.