Sorry, I should have clarified. Yes, I meant including the TER. TWR alone I calculated 0.06% for VT and 0.13% for VWRL. Although based on what seems to be a bit outdated L1WT numbers from the wiki post.

Thanks for the clarification that sounds reasonable. Interestingly, the TD for VT was reported at -0.91% for last year. Anyways, by the looks of it, it seems I am splitting hairs. I was just generally curious about the differences and wanted to understand withholding taxes of dividends.

Well, it’s more complicated than this. I will refer specifically to MSCI indices, FTSE is probably similar, and give 1 example. Most ETF’s performance is reported on a “total return”, with dividends reinvested, basis, even if they are distributing. They track an index, usually a net total return version. To calculate it, it is assumed that dividend distributed by each stock is reinvested after deducting a tax of 30%.

Now, an Irish ETF on US stocks pays 15% withholding tax on dividends distributed to it, and there are no taxes for payouts from the fund. Assuming as an example 2% dividend yield, 0% TER and ignoring compounding in 1 year time frame, this ETF’s performance will be 0.3% better than that of it’s index, i.e. TD of -0.3%, although the fund didn’t do anything but receiving and distributing or accumulating dividends.

ETFs also earn money by lending stocks. iShare is rather transparent about it. A fund can earn more than 0.1% p.a. with this. These earnings also decrease TD.

2 Likes

Thanks for more clarity.

Just a question.

Let’s say there are two ETFs -: ETFA and ETFB. Both track MSCI USA. ETFA is domiciled in US and ETFB is domiciled in IE.

Would both of these ETFs track exactly the same Total Return Indexes as benchmark? Or they track two different Indexes because the underlying WHT assumptions need to be different ?

It’s up to the management company to choose which index their ETF track. Most US ETFs on US stocks would track a US-based index, which would count no withholding tax, I guess. PBUS is vanilla MSCI USA.

1 Like

By the way, I checked the fact sheet of VT and VWRL, it seems their benchmarks are assuming pre-tax dividend reinvestment for VT.

But I could not understand clearly for VWRL because I can find different comparisons. I saw one where only index price is compared so I think it excludes dividends anyways. Then I saw one where all gross income is reinvested but it’s not clear what happened to WHT.

I think VWRL performance vs benchmark might not have this WHT effect (at least based on link below) and can be purely attributed to its lending or simply its effective operations. But I am not 100% sure.

I think you might be looking into this comparison because you might want to buy VWRL but worried about money you might lose by not buying VT instead.

If that’s the case , then please consider following

- These two ETFs are not exactly the same. VWRL doesn’t invest in small caps while VT does. So it’s not just choice of ETF but also about exposure to small caps.

- VT is more tax efficient for CH residents, it is not insignificant, but it is also not so huge difference.

I think in long run, you will be fine with either one.

#1 VT , #2 VWRL for global investing with one ETF

3 Likes

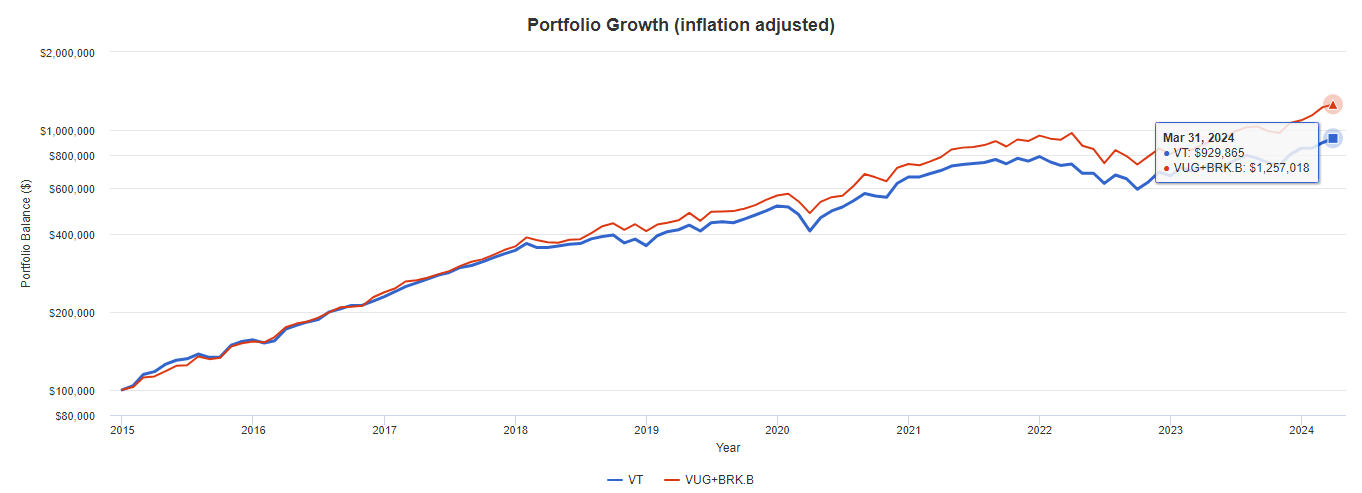

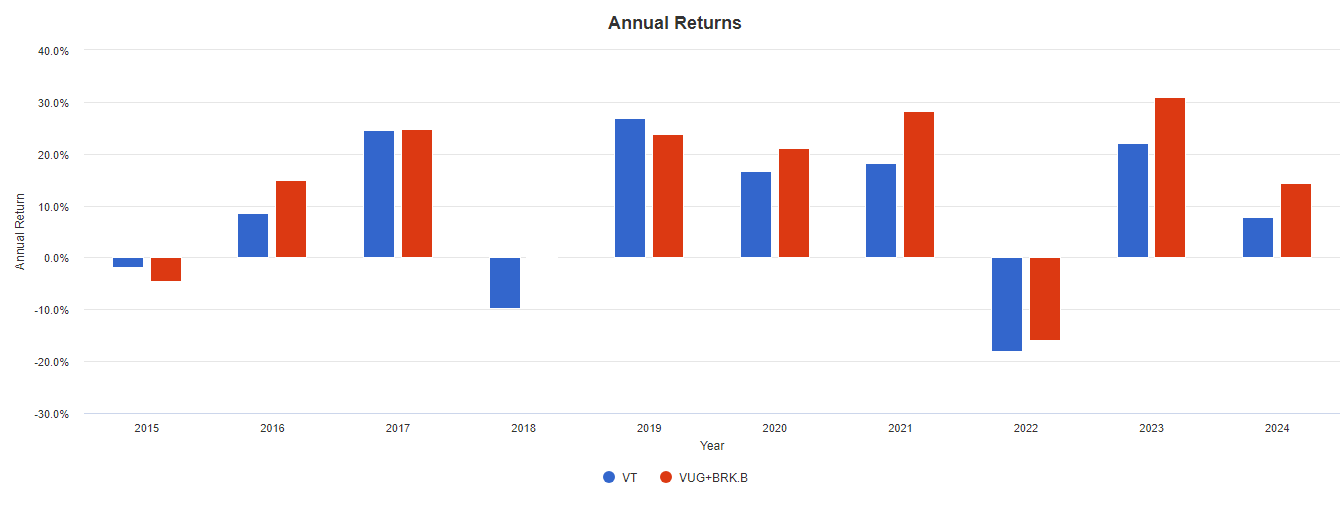

I moved all my equity allocation from VT to VUG+BRK.B shares last year.

Why? Main reason was marginal tax drag on dividends is huge in Suisse Romande.

Being single, a high earner, having military tax, and living in Geneva my marginal tax rate is 50%. Since VT pays ~2% in dividends per year my marginal tax rate gives a 1% tax drag on holding VT.

Compare that to VUG with ~0.5% dividends and BRK.B with 0%. Holding them in equal weight gives ~0.25% dividends or 0.125% tax drag. Expense ratios are also slightly lower but this is less relevant.

Essentially, as long as VUG+BRK.B does not underperform VT by >0.9% over the long run then I am still better off.

Summary of differences between VT and 50% VUG + 50% BRK.B:

- Tax drag: VT has 1% while VUG/BRK.B has 0.13%

- Market correlation: VT has 98% correlation and VUG/BRK.B has 94%

- Growth/Value: Holding a growth fund like VUG and value focused holding company like Berkshire gives rough diversification here

- Geographies: VT is a global fund but as all market cap weighted funds are, is dominated by the US with 65% of its holdings there. VUG+BRK.B is 100% US.

I appreciate that this approach has more US exposure, more tech exposure, and is quite concentrated in specific stocks like AAPL. However, I don’t necessarily see those as bad things going forwards and so for the sake of almost 1% lower tax drag I am content to hold this for the long run.

Performance since 2015. This is starting with $100k and investing $5k inflation adjusted per month since. It is not adjusted for the tax savings (so for VT subtract 1% per year and VUG+BRK.B subtract 0.13% per year).

Note that only 2 years since 2015 (2015 and 2019) did VT outperform. During periods of international stock outperformance VT should do better. Or if there is a big US tech crash and Berkshire doesn’t offset substantially. Otherwise VUG+BRK.B has had pretty incredible returns over the last decade+.

4 Likes

I’m not sure growth is the way to go here. It had some good years recently, true. But isn’t it an anti-factor (of the value factor)?

Since you state that you earn a lot (and therefore have or will have a lot of money), did you consider warpping your investments into a company to shield it from tax? (And leaving Geneva, because 50% wtf)

2 Likes

Well I’m not actively seeking out growth here, its just a byproduct of me seeking lower tax drag. Hopefully in the long run the value from Berkshire and growth from VUG act as good diversifiers.

Not sure how wrapping investments into a company would be more tax efficient. I assume its quite a lot of hassle and with a structure like this there isn’t much tax drag already.

As far as leaving Geneva, I’m sure I will at some point. I have a great job here for now but if an opportunity in a Zug/Dubai/Singapore came about then the tax savings would likely more than justify it.

I believe it’s common that EU domiciled funds track a benchmark “net of worst-case WHT”, ie not considering potential tax treaties. For US exposures, the BM provider would hence assume a WHT of 30%. That’s my understanding when I checked a few ETF a while back on Bloomberg. Not sure on the US ones. I had a look at the VT factsheet and it seems it tracks a benchmark that considers only WHT at the fund but not investor level. Eg the US part would be assumed to be subject to 0% WHT.

This seems also consistent with fund performance. IE domiciled ETF tracking US heavy benchmarks (such as “All World”) often beat their BM as the index assumes 30% WHT for US while the fund only pays 15%. VT in comparison is almost precisely 7bp below the benchmark, reflecting that it very closely tracks the BM, except for fees…

1 Like

If you might leave at the drop of a hat, a company is not so useful, I agree. A company needs a local representative. Moving a company cross-border probably means lawyers.

It’s not thaaat complicated. Hairdressers and carpenters manage. For a small company, you only need to do accounting and pay taxes on it. For very simple buy and hold, some Excel table will do. Filing taxes doesn’t differ much from doing your own taxes. Founding costs start at 400 CHF at startups.ch.

Fringe benefits: It can domicile where you live and help pay rent. You can sell some of your work through your company (less protections, less taxes, duties, and contributions). No fear of professional trader status. Buy and sell all the options, get tax credit on losses. Have some insulation between you and your leveraged investments.

Looking at taxes: Even Geneva taxes below 15%. A company also pays capital gains tax. And you additionally pay tax on dividends you take out (which are reduced for major shareholders).

But yes, for low dividend stocks portfolios that is not that attractive, since you pay nearly no taxes to begin with.

Looking at MSCI ACWI gross returns (should likely be net) since 1988:

| In company | Directly | |

|---|---|---|

| Taxed | Total Gross | Dividends Gross |

| Since 1988 p.a. | 8.21% | 1.96% |

| Tax | 15.00% | 50.00% |

| Drag | 1.23% | 0.98% |

And you would still have to pay additional taxes to take the money out of the company. Ahh… Geneva and their 50% tax wins. ![]()

3 Likes

Thanks for crunching the numbers.

In the end in Suisse Romande I think you just have to go for as much capital gains as possible. Any dividends or bonus taxed at marginal rate is just a big cost of working here.

Does exist an etf replicating S&P or VT but without any taxable income ( last column of Ictax ) ?

Like boxx for the us bill

Not really, and if there was a popular one, ictax would probably eventually invent a virtual dividend, like they do for accumulating etfs.

There are some Canadian Horizon “total return” etfs. But you‘ll likely have unrecoverable withholding tax layers with that (or maybe not, as they are synthetic, haven‘t looked that deep into them), so probably not worth it and might be eventually taxed, who knows.

E:

There is one in ictax for example

https://www.ictax.admin.ch/extern/de.html#/security/51302635/20231231

Should be this one https://horizonsetfs.com/ETF/hxs/

There is however a swap fee integrated of “no more than 0.3%”

Which can be quite a bit.

But actually on second thought might be interesting. I‘ve looked those up in the past, but did not dig deeper. I‘ll need to have a closer look on those.

They do have various other total return etfs also: Global X

But those are not in ictax.

EE:

On another glance, it says this in ictax " * (I) The taxable earnings could not yet be identified andbe determined later."

But it says that even for 2022, cant imagine they 2 years to determine that. I wonder what you do in such a situation for your tax declaration?

But I think you see the potential problem.

EEE: for 2021 it was 0 taxable income: ICTax - Income & Capital Taxes

There may be some IE or LU domiciled swaps based UCITS that might have zero income. Not sure about their cost structure though. And also is they track gross or return returns of jndex.

1 Like

My limited research so far seems to conclude that there is always some significant cost involved.

For example apparently for the Horizons etfs the swap fee of up to 0.3% is to reimburse the swap counterparty for the withholding taxes.

In the end depending on your marginal tax rate, there might still be a tax benefit.

ICtax always takes into account dividends of the accumulating ETFs using swap on the european market (UCITS ETFs).

Not sure why it is not the case for these canadian ETFs.

No one in Switzerland holds these Canadian ETFs.

1 Like

Hi, I have 2 beginner questions about this topic:

- L1TW = 0% for US stocks paying dividend to US ETF

- L2TW = Originally 30%. Thanks to double taxation agreements, a “qualified intermediary” can reduce taxes to 15% thanks to the W8-BEN document. The remaining 15% taxes can be refunded through the DA-1 document in the tax return.

1.) Is L1TW still 0% for ETFs like VEA (developed markets) or VWO (emerging markets)? I saw this question in the thread and the answer was that you have to calculate it specifically for each case.

US ETFs are more tax efficient because the withholding tax will only be repaid by the authorities one year later on your next tax return or deducted from your tax bill. However, this money cannot “work” for you during this year. For example, it could have grown thanks to a good financial year. However, you will get exactly this amount back from the authorities. That’s why the 15% US taxes are preferable to the 35% Swiss taxes because you have 15% more of your dividends and therefore more money in your bank account that can “work” for you this year. After a year, thanks to economic growth, this money could be higher than the fixed and equal amount that the authorities deduct from your tax bill. That’s why the following applies: the less withholding tax you pay, the better.

2.) Is this explanation true as to why US ETFs are more tax efficient than i.e. Swiss ETFs?

Thanks in advance!

Nope undortunately not. It‘s around 10%. Non-recoverable.

US citizens would get some tax credits for that, for us that‘s not possible.

But it‘s still a little (like not meaningfully)better than Ireland, as US has better tax treaties (example L1 wht for Japan in Ireland is 15% in US 10%, Switzerland 17.5% Ireland 35%, but Europe ob average has better treaties with Ireland than the US)

I think this difference is so little that it‘s basically meaningless. It‘s only 20% of your small 2.X% of the dividend. Also swiss funds only distribute once a year. That also has an effect.

No.

Actually swiss funds, with swiss securities, are the most tax efficient (in regards to dividend taxation) for the swiss investor, as there is 0% withholding after tax declaration on any level (sometimes you dont get everything back with DA-1 due to various reasons, e.g. mortgage deductions).

Plus about ~10% of the dividends of swiss funds get distributed as capital gains, so are tax free!

Granted it‘s not a huge difference.

3 Likes