Really?

I believe I read about it on Saxo Switzerland.

Good to know it doesn’t apply in CH.

Really?

I believe I read about it on Saxo Switzerland.

Good to know it doesn’t apply in CH.

Saxo also applies eu law to swiss investors (kid requirement etc). You can freely disregard anything from there.

Also wash sales are only relevant when you incure a capital loss and then have that loss to potentially reduce taxes in the future.

That‘s why americans do tax loss harvesting (while avoiding wash sales).

Neither is applicable in Switzerland as there are no capital gains taxes.

said Index fund takes MSCI US NET Dividend as Benchmark (aka post FULL 30% Withholding Tax). Over the last 5 years it misses its Benchmark by about 0.24% p.a., which is 0.02% p.a.a worse than its TER. UBS is just terribly bad in managing Index Funds. The question is if anything will change there, as CS was terribly good in managing Index Funds.

The competitive CS fund takes the same benchmark, applies roughly the same TER but bets its TER by about 0.03% p.a. Still not a super good result actually; US shares should just be held through an ETF and this IE domiciled.

I added a paragraph about subscription tax in Luxemburg.

Just wanted to provide an update. It turns out the information provided to me was not completely accurate. So for US stocks, the order of domicile seems to be following

BEST - US

2nd BEST - Ireland

There is an article from Finpension which desrcibes their view on this topic.

https://finpension.ch/de/das-beste-fondsdomizil-fuer-schweizer-anleger/

Why does this finpension articles just completely omit that you can in fact buy US etfs at ibkr and swissquote and others? It‘s like lying in your face.

If you search this forum you can find posts/ thread about Swiss investors potentially losing access to US domiciled ETFs in 2021/22 if / when IBKR/Swissquote decide to follow other brokers to make their life simpler (aka blocking Swiss private investor access to US funds) just as they have done so for EU residents following MIFID.

I think they are just saying it is difficult to buy US ETfs. And in fact it is difficult for retail investors. Only IB and SQ support that and there are so many banks and brokers in Switzerland. Just because 2 brokers allow it, doesn’t make it easy.

I would say that the spirit of the document is to explain tax advantages and disadvantages. I think they did a good job. They don’t have to recommend brokers on their webpage.

Thanks to @nugget’s sheet I tried to compare the total costs of an IE vs US domiciled world portfolio. Even with the Bogleheads Wiki it seems some of these values for L1TW or L2TW are estimations and not that easy to obtain.

One thing I am still struggling with is understanding why reclaiming the 15% L2TW for US ETFs via DA-1 does not lead to 0%.

If I am correct it requires a tax rate >15% and no mortgage. However, somebody mentioned the practical difference is 0.3% * (1- marginal tax rate). I don’t really understand why. 0.3% are clear (15% WHT of 2% dividends) but the marginal tax rate would apply to IE dividends also. What am I missing?

If I assume 0% for L2WT and compare VXUS vs VFEM&VEVE the total costs seem very similar.

US etfs are still a bit better than IE etfs, mainly due to better treaties with Japan, Canada and Switzerland among others (while some european countries are a bit worse). Plus the other benefits such as size/liquidity/transaction costs/ter/more holdings.

Granted it‘s not a huge difference (for basic market cap weighted index etfs), but still worth it imo.

What you can do to estimate cost of specific etf is going through their yearly report and look how much dividends they had and how much was withheld.

And normally you should be able to fully claim DA-1.

If you care for those markets and withholding taxes, why not buy directly at the source in Tokyo or Toronto? ![]()

That statement doesn‘t make sense to me.

We buy total market index funds here mostly. They are practical, self rebalancing and efficient.

We are discussing VT/VXUS etc. vs other IE domiciled funds at the moment also. I contributed, that US etfs are still more beneficial, due to the aformentioned treaties giving an advantage. Your point has nothing to do with that.

It does, kind of. There’s some nuance to it, maybe think about it again.

The difference between a single fund in IE and US is relatively small, percentage wise.

If you are willing to go through the trouble of reading yearly reports to compare withheld taxes on dividends, you might as well buy several index funds that replicate the total market.

Even though it’s difficult to get to final number easily, I think the real difference between VWRL and VT will amount to 0.1 to 0.15% per annum after taxes in terms of their tax efficiency and tracking differences. I don’t worry too much about TERs because they can be misleading sometimes.

However since they anyways don’t track same indexes, the performance will be different anyways. I did some calculations few weeks back and found both ETFs actually returned the exact same total return over long period. I forgot how long I checked . Maybe it was 10 years. Lower tax efficiency of VWRL was compensated by lower exposure to small caps.

So I concluded below

I know you can try to do the math and 0.1% over 20 years might mean 2.2% of performance difference. But, let’s not forget 2% might be weekly fluctuations in price of these ETFs too.

I hold both. Simply because I don’t want to be stuck to one ETF or broker. Although majority is still in VT

You do that once and get a sense of the wht, that‘s all. It takes a couple minutes.

Your portfolio will get a big mess if your start with single country etfs, that may have high ters, less liquidity, higher trading costs, rebalancing effort to keep goal allocation, missing countries with no accessible index fund, or some with no/bad treaties etc.

It‘s wholly impractical.

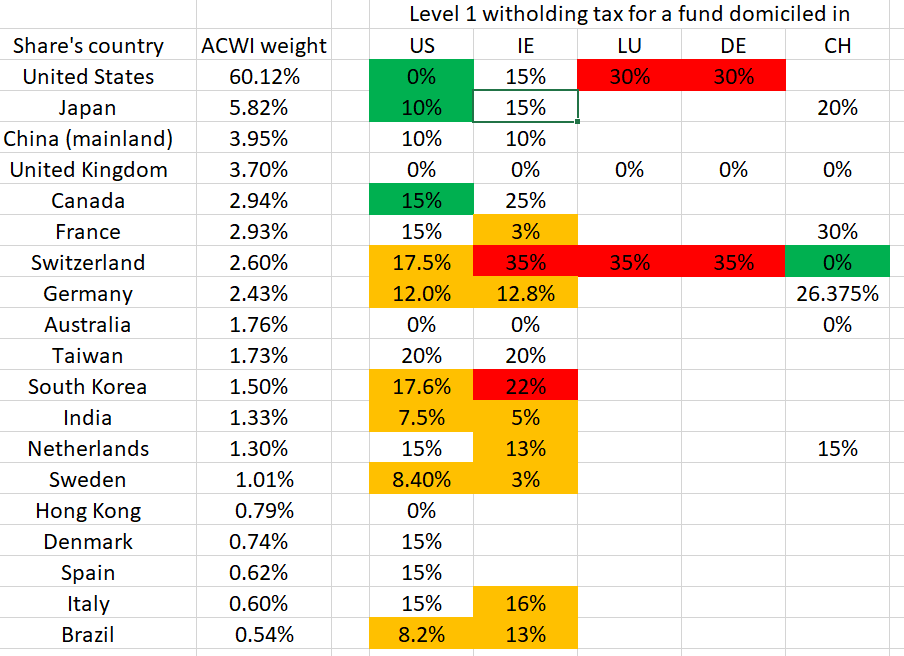

You can also take this list from @Dr.PI as a reference:

Look, that table and your comment support my point. I was referring specifically to Japan and Canada.

Anyway, my portfolio isn’t a mess, nor impractical. Don’t get me wrong, it can be done simpler, I get that. I just wanted to share the thought. In the end, it’ll be just a few hundred CHF difference, so you do you.

How do you single out Japan and Canada without having every other region as a single fund as well?

And I never said anywhere that the difference is big, I specifically said it‘s not a huge difference. So I don‘t get where I‘m supporting your points.

Your post was good to read for my confirmation bias, as I came to the same conclusion. I also hold both, despite there higher costs of VWRL, as I view VWRL as a form of insurance (and in my case I also have more in VT than VWRL).

That’s definitely a good point to hold in mind to gain perspective on the sums involved! (I would however argue that there is a difference between 2.2% in volatility vs 2.2% expected difference… but your general point stands IMO)

I agree. We should try to reduce the costs if we can. Always.

But we should also not forget what the amounts are. That’s all I wanted to say.

I believe the discussion about TER etc started getting lot of attention during the times when active management use to charge a huge (maybe 1.5-2%) amount of money. Then index investing came into play with costs like 0.25%. So that was interesting and significant.

But now I see people start changing their whole portfolio for 0.08% TER difference by selling their ETFs and buying new ones. This is alright. But we should not get too much obsessed with these things.

Also, TER needs to be considered combined with the tracking difference. If a very low TER ETF has a high tracking difference it may still perform worse than a higher TER ETF with an excellent tracking difference.