@Peter Yeah there isn’t much advice out there for Switzerland, but in general people and the tax authorities seem to advise declaring any funds you have no matter which type of account or financial vehicle they’re sitting in. In other countries (e.g. France), the government is a bit clearer on the subject of Revolut and states you must declare such accounts.

As a Swiss resident, I’ve decided to declare Revolut and TransferWise funds to avoid any potential issues.

For Revolut I’ve proceeded as follows:

1 - Account description: “GB Revolut Ltd (eWallet XXXXXXXX, CHF)”

– eWallet number I use the “wallet reference number” found under Settings > documents > account information

– I add an entry for every currency used in the app, in this case CHF

– GB is in reference to the country in which the IBAN is located

2 - Country: “Royaume-Uni”

– As the IBAN is held in GB

3 - Account number: “XXXXXXXX”

– I used the “IBAN / Account number” found under Settings > documents > account information

– Note: It’s also the same last 8 digits as found in the eWallet number, and you’ll find the same IBAN is used for all Statements (including CHF holdings)

4 - Fortune Imposable: “XXXX”

– Grab your December Statement for the currency in scope

– Select the appropriate currency from the drop-down (CHF, EUR, etc)

5 - Rendement: “0.00”

6 - Impôt anticipé: “Non soumis à l’impôt anticipé”

For TransferWise, same process with only the following comments:

– eWallet number = “Membership Number”

– I believe every currency has its own IBAN, but I only have EUR activated so can’t say for sure.

For me this is a little bit overkill…

It clearly depends on the amount you hold on your revolut. For me is always <= 1’000 CHF, also I tend to consider it as cash…

Do you declare also the cash you held at 31/12 (e.g. what you had in your wallet ?)

As I said on this post (in French) ( Impôt sur la fortune ), I consider this a prepaid card and do not declare it. Not because I want to evade taxes, but because it’s not worth the hassle to me. There is no income tax to be paid, only wealth tax. So what, 10 CHF max of “evaded” taxes?

Yes, I declared the cash held in each currency (separately) as reported at 31/12 from Revolut’s statements. However it only took a few minutes with the different apps open.

I figured it was easier to add them than have to deal with more time and stress if the tax authorities decide to call back. The fact I had over 2k per currency (due to holidays) at 31/12 definitely helped me come to this decision

Various countries seem to want you to declare Revolut/TransferWise/N26 accounts (Paypal seems to be an exception, often treated more as a payment service). See below an example from France:

Hi @Ceitinn, in fact I was referring to physical cash (i.e. paper bills you hold at home) more than electronic wallet.

Of course it depends on the amount, but I’m not sure that if we have a few hundred CHF at home for regular cash expenses, we shall/will put those in our statements… as @Ed_Waadt said, it only impacts wealth tax. at 0.1 %, if you hold 1’000 CHF we are talking about 1 CHF potential tax…

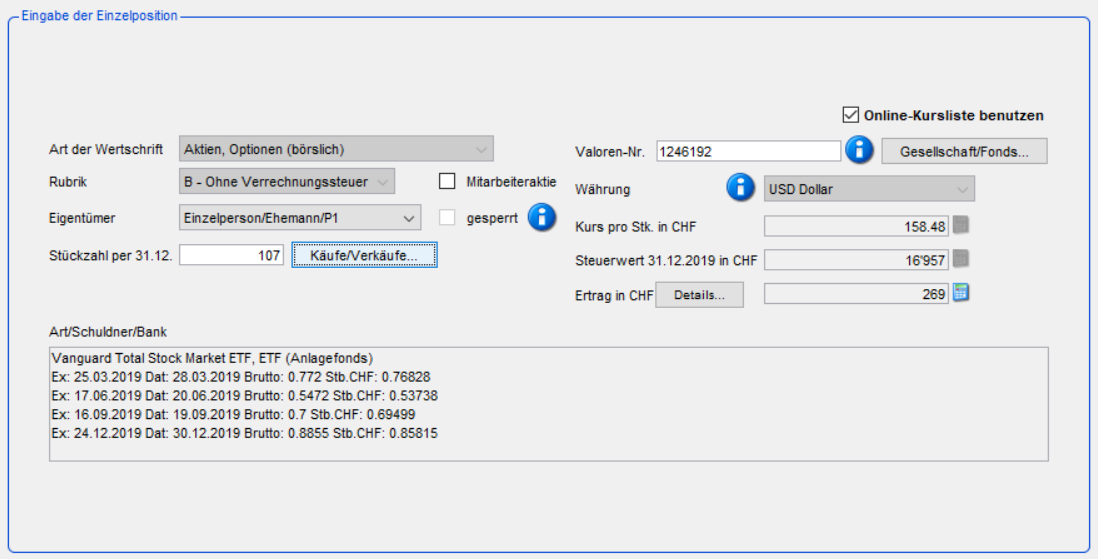

Question: For those investing in VTI - Do you get to classify it under the “DA-1” category in your tax tool?

For me (Basel BalTax) it is automatically selected as “B - Ohne Vst.”, and doesn’t let me modify it.

For others (VT, VEA, VWO) I can imagine they would have a harder time to split it, but VTI is all-US, so calculating WHT should be trouble-free for that.

Even if set under B - should I still be able to list it within DA-1 form?

VT, VEA and VWO are all domiciled in the US and are subject to the 15% withholding taxes that you can get back with DA-1 unless you pay lots of interest.

In Tax declaration, how do you report Dividends that were paid in the form of Capital Gain (example UBS)?

I know that Capital Gain is not taxable, but I believe it has to be still reported in the tax declaration as an income? And if yes, how?

Many thanks for your comments and feedbacks,

Peter

You don’t need to report them. It can be paid with reserve from capital increase, with a distribution of capital reduction, or from real estate funds who directly own the buildings, any tax-free dividend is not to be reported.

A question about putting in the “Vermögensverwaltungskosten”.

In BalTax (Basel) I got automatically calculated some silly number (38 CHF).

Based on what they get it, I cannot deduce (38/0.003 = 12667, which is no line item of mine in the Vermögen part…).

I understood one can write down max 0.3% of the “total managed assets”.

As you need to enter it “per account”, i.e. in a table, I was planning to add one line for IB, one for UBS, and put in the “monthly fees” (2x120).

This would still keep it all under the “0.3% rule”, so all good.

Do you also somehow add your VIAC/3rd pillar fees? (e.g. part of 0.5% total mgmt fees)

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.