I just got an email from them stating that they changed a couple of rules. The “meanest” one is that if you don’t pay in time, the interest charged start from the day of the invoicing instead of the day when you receive their bill. In the worst case it might be a month I suppose.

Also the 30CHF they ask you if you don’t pay the bill are the same and shouldn’t be forgotten.

I personally dislike SwissCard alot, they were too incompetent to cancel my Miles&More Duo cards, despite sending me a written confirmation that my account was cancelled last year. 2 months after the cancellation confirmation I got a invoice for the yearly fee and some transactions of servcies which I forgot to move to another card. Told them to go f* themselves.

There are two methods which are widely used. One is the billing date and the other is the posting date. In the billing date method, interest is charged from the end of the billing cycle (for balances carried past the due date). In the posting date method, interest is charged from the dates on which purchases are made. Obviously the billing date method is more favorable because you pay less interest.

I find the income tax progression goes up in relatively small steps. Do you have an example of when paying this massive interest, one comes out ahead after having paid ones taxes?

Does anyone make this kind of calculations? I wonder if I should do that myself in december and just withdraw a lot of money through the CC. I’m not even sure where to write CC debit on the tax declaration…

Daniel was talking about the interests (not the debt itself). I don’t think there’s any case where you’ll get more money yourself because you decided to give money to someone else instead. Since taxes are progressive, every extra money you earn increases your overall wealth minus marginal tax rate, interests paid should follow the same logic (assuming those interests are avoidable, and there’s no opportunity cost).

If you’re thinking about doing that, donate to charity instead. At least you can decide how the money is used instead of just increasing bankers wealth.

There is no such case where doing what you propose would result in saving you any mone (besides some rounding errors). Tax is progressive but also monotonous, more income always means more tax - follows directly from definitions of tax progression in swiss laws (typically worded as a set of clauses like ‘every X franks after Y shall be taxed at Z%’).

The right way to think about tax deductions in progressive tax regime is not in terms of which tax bracket you end up in, but in terms of marginal tax rate (first derivative of tax wrt income). If your marginal tax rate is 40%, that means your after-tax interest is 40% cheaper than before-tax, e.g. 0.6% instead of 1%. Marginal tax is always positive and so you can directly see why NOT spending the money is always better than spending & deducting it.

In terms of plain tax, you are right. However, your taxable income bracket also impacts many other financial aspects i.e. health insurance premium reductions, eligibility for scholarships or children’s educational or daycare subsidies, etc. So the tax saving in itself may be minimal or non-existent, but the full value of having a lower taxable income can be substantial - depending on your situation.

For example, reducing your taxable income by just a couple of francs can make you eligible for 1000-2000 francs more health insurance premium subsidies per year. That would be one example, but there are many more which could apply. But obviously these things are more important if you don’t earn a very high income or if you have a lot of kids (like I do).

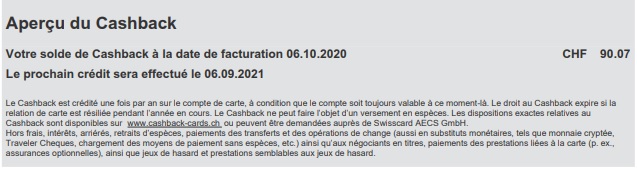

Subscribed to cashback cards one month ago and their promess was 5% cashback for the use of the card in the first three months (limited to max CHF 100 cashback) but still a good deal. But with the first bill they say that they will credit the account in… september 2021 (if I don’t resign in the mean time of course)

What a joke!

You should read the Terms and Conditions of whatever you subscribe as it is clearly mentionned in article 3.3 :

In french : “Le Cashback est crédité une fois par an sur le compte de carte du titulaire de carte participant, initialement le même mois de l’année suivant l’ouverture du compte de carte. Le Cashback cumulé est indiqué sur chaque facture mensuelle accompagné de la date du prochain crédit («jour de référence»).”

In english : “The Cashback is credited to the Participating Cardholder’s card account once a year, and for the first time in the same month the card account was opened in the following year. The accumulated Cashback is always displayed on the monthly statement together with the date of the next credit (“Reference Date“)”

It’s just an advice to not be surprised in the future

Yes thanks for the reminder. I usually do for more important things.

But still, after 3 other cashback cards, its the first that makes you wait one year to have your cashback. And specialy for a thing they big advertize on (Get 100 francs welcome) I find it kind of petty.

Just my consumer point of view

Don’t mind I don’t like either their marketing program about their welcome CHF 100 cashback and the fact that you have to wait 1 year to take advantage of the cashback.

In the other hand it’s also a security for them to protect their business and hoping that not everyone will be able to access to the cashback (for example people who don’t pay their bills at the end of the month).

I’m looking to try their program on December or next year.

It’s basically a 100chf goodbye… I think I will stop using it after a year. I feel a bit uneasy with their helpdesk and the fact that they sent me one bill twice… I didn’t call them yet, maybe I should. (the bill is exactly the same, same id etc… just sent twice)

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.