Diversification basically.

Also Credit premium from less safe bonds (swiss bonds are basically the safest bonds in the world)

For example there also have been times when governments default on their debt and your bonds become worthless. Super unlikely for swiss bonds in particular of course, but if you exclusively hold those, you put all eggs in one basket.

It’s however relatively fine to only hold domestic bonds. I woudln’t though, and do something like 50/50 domestic/international hedged

No, I get buying a bond and holding it to maturity, collecting the coupon and getting the principal back upon maturity. That’s simple enough to understand and also as a hedge to equity. It’s bond funds that I am not understanding and not finding in any way attractive.

Buy bond ETF today at YTM x% and duration y

If you hold this fund for 2y period then you would get original principal plus x% per annum for the period. This equation could hold true also for less than 2Y duration but some research say 2Y period increasing probability

An important point that took me time to realize is that most of “personal finance” materials that you can find are written either by US Americans or financial professionals, or both . It’s not that they are wrong, they might just not apply to you and me: a small scale private investor in the accumulation stage residing (and having tax liability!) in Switzerland.

I would say there are 4 reasons to hold bonds:

reduce portfolio volatility,

for yield,

as a diversifier,

for safety.

When it comes to assets allocation, I mentally replace “bonds” with “cash” and I am fine with the discussion.

When it comes to yield, you know: bonds in CHF have very low yield, so you have to either increase risk or duration. Besides, I think that because of a strong demand, the yields of Swiss bonds are lower than they should be.

So, I prefer to “Take risk on the equity side” and ride on with volatile equity and supersafe cash.

Bank’s mid term are not exactly an equivalent to bonds, as they are not liquid, but it is also an option for us.

But this is an important point for people with more depreciating currency. If you count in USD or EUR, you must have some kind of yield on your fixed income, otherwise you are losing too much.

When it comes to diversification benefits, well, diversifiers themselves should have non-negative return, otherwise cash is better. Yes, when the interest rate is falling, the value of bonds goes up, even if their yield was already negative. But it sounds like speculation on interest rate movements,not an investment to me.

Most importantly, I am accumulating and I don’t need to spend my portfolio. I can wait for the portfolio to recover.

If you are spending your portfolio, you are in a different situation. If you are an institutional investor, same thing. I would say financial professionals think in terms of institutional investment practice, even when they think that they write for retail investors.

My cash in a bank account or medium term bank notes are safe thanks to the obligatory insurance of deposits. If I need more guarantee coverage, I open another “normal” bank account or an account at a cantonal bank with unlimited state guarantee.

Businesses can’t do this, they are not covered by the depositor’s protection. Pension funds can’t leave couple of billions on their UBS bank accounts. They have to do some kind of investment, which can be a money market fund or bonds. We don’t have to.

I wonder why so many privates in Japan hold governmental bonds. Is it because there are not many safe options for cash or they are rendering service to their country?

I understand that’s the theory, but then why does the value of the bond fund drop over these long periods of time? Maybe my fault is that I look at the chart and not try to backtest it?

@dr.pi you articulated my (far less elaborate) thought process completely, I’ll save it…somewhere…so I remember!

Edit: as I said I do not understand bond funds, or bond trading.

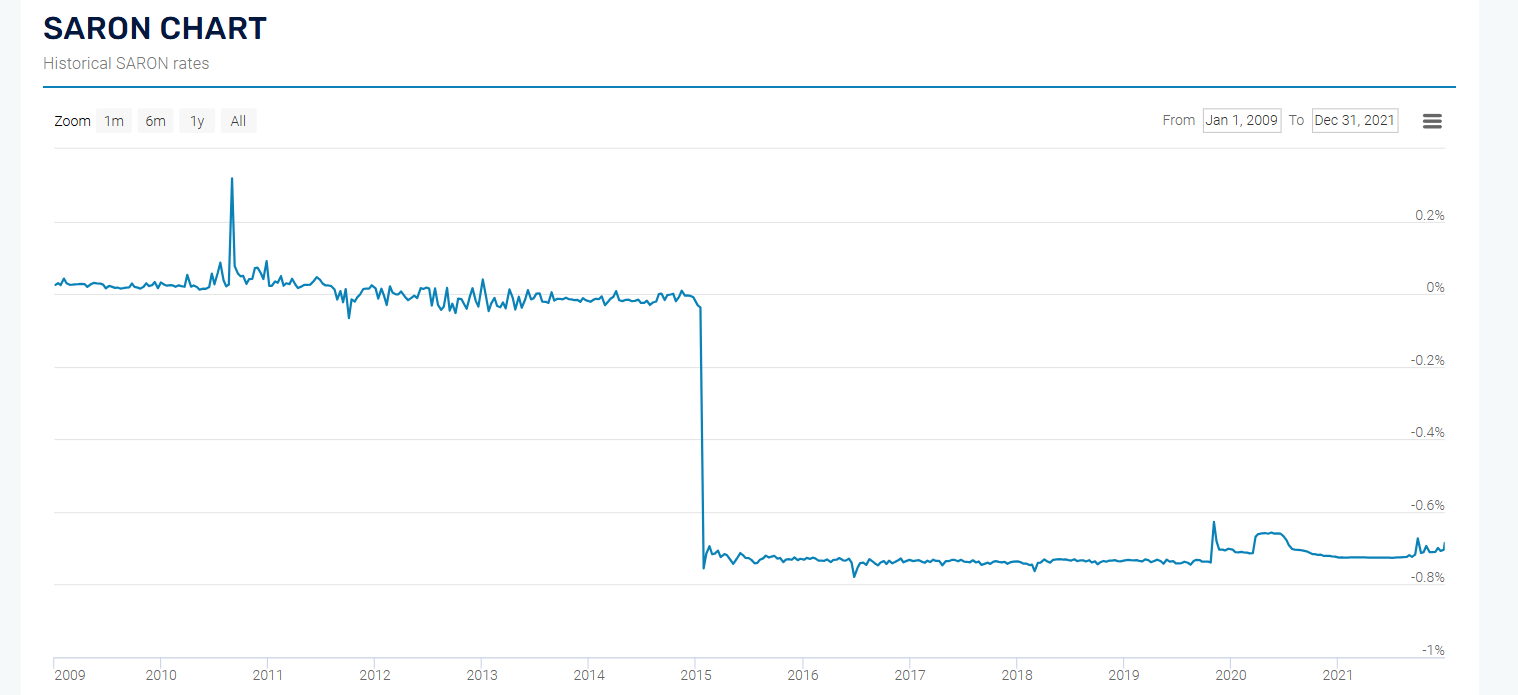

The gross yield-to-maturity for 2Y CH gov bonds was zero or negative from April 2012 until April 2022. (And it’s again zero or below for a month now).

I’m wondering in what capacity banks will apply negative interest rates to bank accounts if/when the SNB policy rate again enters negative territory. They might be less reluctant compared to the first time, in which case, you might need to open a lot of different bank accounts if you want a significant cash allocation to avoid both negative yields of safe bonds and negative interest rates of bank accounts.

Why would someone pay for the privilege of lending someone money? I mean, if they aren’t getting protection from Don Vito?

I get it, to me a bond fund for someone earning CHF makes little sense. Single bonds, maybe.

I guess a use case could be someone having cash in a weak and weakening and manipulated currency which they want to protect by buying a bond in a stronger currency?

They don’t. However, the base fee is 0.52% p.a. on the invested amount, capped at 0.40% p.a. for the whole portfolio. Global 60 without bonds invests 74% of the portfolio (incl. real estate and gold), so there is virtually no benefit at that level. Global 40 without bonds would be quite cheap with portfolio fees of 0.28% p.a., though. You can easily compare the variants on VIAC Pillar 3a Investment Strategies - Cost-Effective and Broadly Diversified

VIAC still offers a 0.3% interest rate on cash holdings in 3a but I guess that will essentially vanish with the next lowering of the SNB policy rate.

I was curious about this. So i tried to check some data. read on Pictet paper, that expected real return on 10Y Swiss bonds is 2%, so ideally it should be better than cash. I wanted to simulate what would people do when SNB rates are low , so i looked into period of 2009 onwards when interest rates were similar to what they are right now. I

SNB interest rates have been <=0.25% for the period of Jan 2009 to Dec 2021. So we can assume cash yield for this period was close to ZERO.

But Swiss Govt Bonds 7-15 years (first chart) returned 38% and Swiss Govt Bonds 3-7 years (second chart) returned 11.4%

For taxable accounts, lot of these yields might be taken away in taxes, but for pension accounts like 3a, this is much better than keeping cash. What might not make much sense is short term bonds 0-3 YR as they tend to have very low yield

Negative yield bond investments were a topic of big debate in past. There is a lot of literature on this.

It was mainly used by funds and institutions.

For retail investors it wouldn’t work. But again it depends on what duration are we talking about and what bond ETF

Corporate bond ETF (CHCORP) in Switzerland is yielding 0.9% at this moment. So it’s not zero or negative yet.

People or organizations with a big amount of money, and where that money value needs to be stable and/or with predictable cashflows, are forced to buy bonds at any yield basically.

You as an individual might still get 0% at a bank when the yields are very negative. But someone with a million+ will get a negative yield at a bank.

So if a bond has less negative yield than the cash at a bank, it‘s still a better deal.

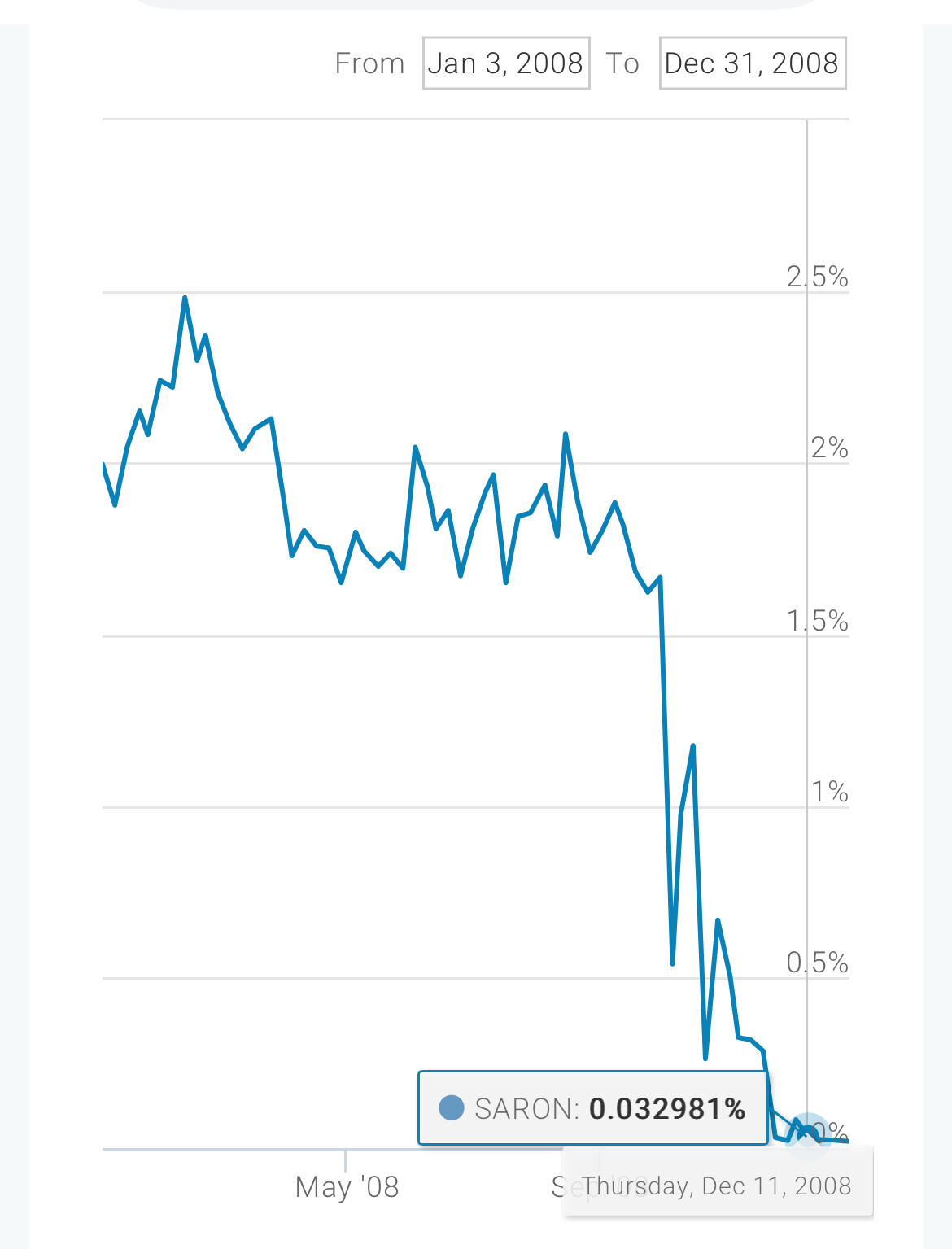

Returned if you bought them before the rate dropped, or if you bought after that?

Well, anyway, there is a huge mismatch in duration of these fixed income instruments, so it’s not really comparable. 10Y were getting more expensive while the current rates were stable because future interest rates were going down. You can compare with historical 10Y swap rates.

Yes that’s true that cash has no duration risk and hence no reward too.

However the discussion was about if bonds make sense for Swiss investors. And medium to long term bonds can still make sense. Short term bonds , maybe not

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.