(And while it’s good to keep those things in mind I’d argue that there are no imminent threat of that happening and insuring against low probability risk can be overkill, Argentine or Turkey economies didn’t turn this way overnight either, right?)

I’d put it under inflation risk. It is, afterall, a reduction in the buying power of my money for things like travel and buying things abroad. Instead of having products imported in my country and being more expensive (inflation), I am exporting myself in other countries and my money buys less there (whatever this is called). Conceptually, it’s the same thing to me.

My understanding is you should match the duration of your bond fund with your investing horizon, meaning that if, as time passes, your spending horizon for the money you keep in that fund goes below 1.7 years, then part of it should be in cash to bring the effective duration of your cash+fund mix in line with your planned expenses.

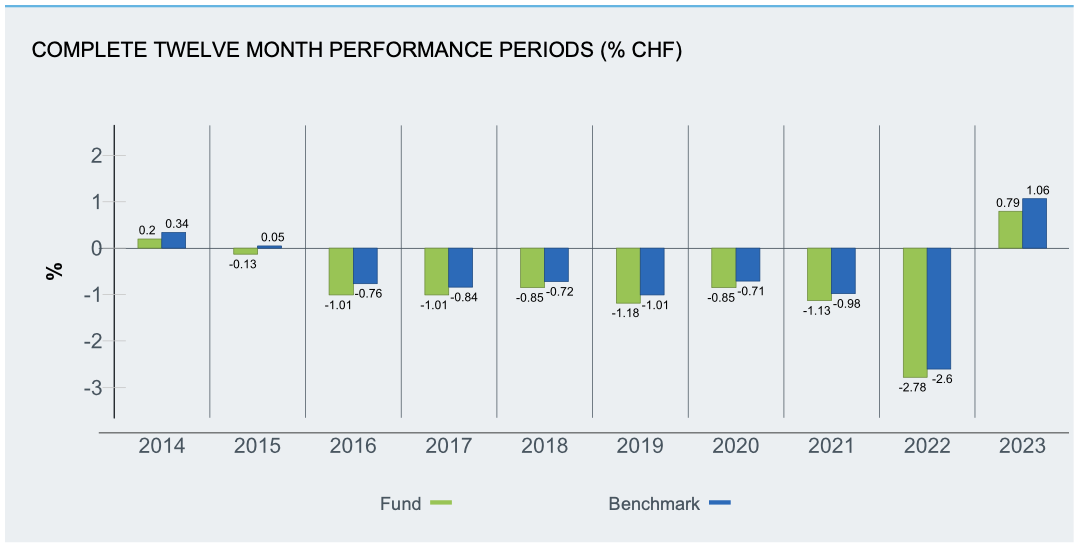

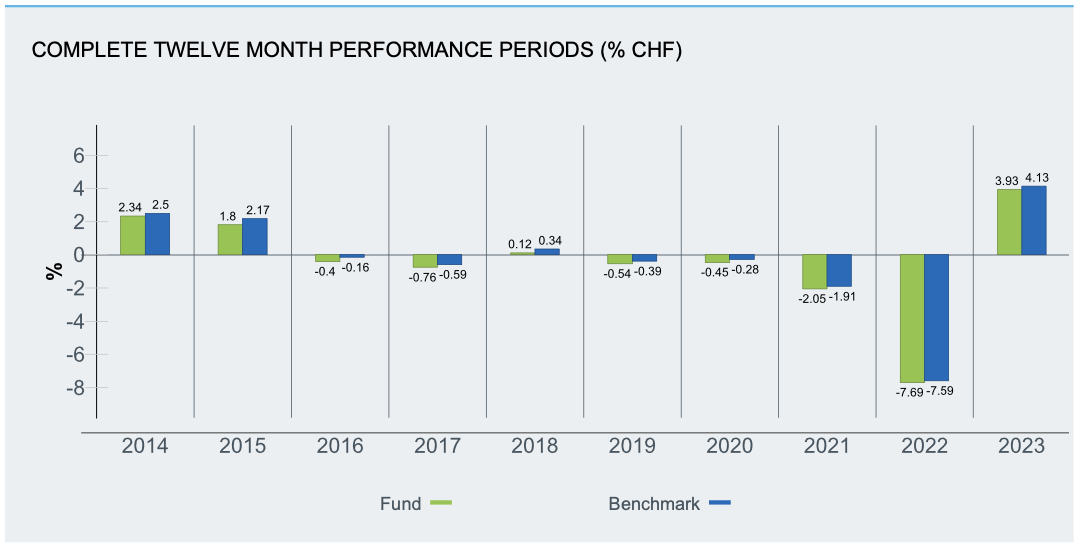

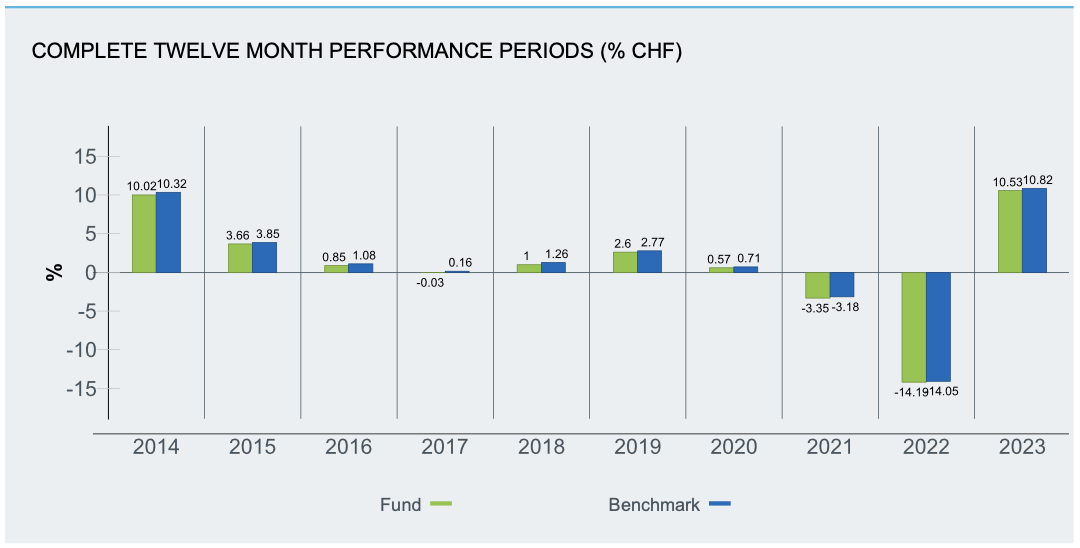

I was about to say it seems strange that there was such a large movement on short duration bonds and vice versa for long. It looks like 2022 was the time to buy CHF bonds!

2022? The year Russia attacked Ukraine and threatened nuclear war every three days, whilst stocks and bonds went down in lockstep. Just after all the COVID seemed to fizzle out.

We now know better, but if prices reflect information, there was a chance for worse.

My question at the bottom of the charts probably got lost:

But I answered it myself in the meantime: these values are including dividends. There’s even a fantastic little chart on justetf.com where you can see the part of the profit/loss that is dividends.

One question: are the Swiss government bonds generally considered better than opening a saving account with for example WillBe currently at 1.3%? If yes, why? Returns seem very low

I think you need to include more variables in addition to interest rate

Overall variables are

duration (how long you need to hold the investment)

credit risk (would you actually get money back)

interest rate

taxation

Let’s take an example

Swiss 5 year bond . Current yield 0.83%

WillBe interest -: 1.3%

Swiss bond comes with highest level of security, the yield is guranteed for 5 years and only coupon payments would be taxed. Capital appreciation would be tax free (depends on what bond you buy, this may differ) … keep in mind Swiss 5 year bond yield is low because market is pricing in rate cuts.

WillBE credit rating will be lower, but most likely money is secured under Esuisse guarantee. It is not guaranteed for 5 years. It’s not guranteed at all for any time period. Full 1.3% will be taxed as income

Corporate bonds will have lower credit risk, but higher yield than Swiss bonds.

Thanks a lot for your information, it is very helpful.

To be honest I was hoping that the returns of at least the corporate bonds were higher like 2% or so.

I have to think about it, maybe for not very big investments it’s not worth it.

Thank you!

Indeed. It’s around 1.5-1.6% (after fees) for the ETF.

Keep in mind, it’s an ETF which works different than individual bond. ETF never matures. so in order to ensure that you lock in your yield, safe rule of thumb will be to hold the ETF for 2X the duration. I read about this rule of thumb at link below , they also have a simulator to see impact of interest rates changes.

I think the risk premium for Corporates versus Swiss govt is less than 1% for same durations.

There are few companies which have higher yielding bonds but they also have higher risks. They can be found in Bond Explorer at Swissquote

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.