If you believe the market will go up in the next 4 years, don’t buy it because you will make less money.

If you believe the market will be down in 4 years, then keep your cash, because it will be the same at the end, except if a big crash occurs in less than 4 years, then you can use your cash to buy shares at a lower price.

And of course, why these companies (same question with every structured product)

This product looks extra stupid compared to barriere reverse convertibles which I wouldn’t buy anyway, but makes sense in a way

This kind of product might be an option for someone who has cash but doesn’t want to take risk in the stock market. For example because the cash is for a future house purchase.

If I understand the term sheet the return is capped at 18% after 4 years before tax (max 4.2% p.a. ). Most of the upside potential of stocks is sacrificed in return for keeping your starting capital but if your next best alternative is keeping cash at the bank at <1% interest it does not look awful

Important to know you are exposed to credit risk of the issuer (if Swissquote bank SA goes bust you likely lose your money without any protection from the government)

As I understand it, selling before the final fixing/redemption date would be selling on the secondary market. I.e. you get whatever someone else is willing to pay for it, no guarantees. They do mention “Daily price indications will be available” but I don’t know how they will calculate the indicated price.

Just received a similar email from SQ promoting this kind of products as “more interesting than sitting in cash”.

Swiss leaders, with 100% downside protection and potential for coupons

—

Get the capital protection with the potential for annual coupons. By subscribing to our “Swiss Capital Protection with coupons”, if the stocks go up, you make profit, but if markets collapse, you are protected. A more controlled strategy than just “buy-and-hold” or interesting than sitting in cash.

If all stocks are above the Initial Fixing Level on 27 of February in:

Year 1: Autocall at principle 100% + 3.50% memory coupon, otherwise product continues;

Year 2: Autocall at principle 100% + 7.00% memory coupon, otherwise product continues;

Year 3: Autocall at principle 100% + 10.50% memory coupon, otherwise product continues;

Otherwise: redemption at 100%.

So simple, it almost feels like cheating

All you have to do is subscribe to our “Swiss Capital Protection with coupons”, which gathers 4 of the Swiss stock leaders: ABB, Novartis, Swisscom and Swiss Life. Your funds will simply be blocked while they potentially generate revenue for you. However, you will be able to close the position at any time.

Risk-wise, could we call those products as “corporate bonds” of Swissquote Bank? Basically you are guaranteed with a yearly coupon (+ potential capped gains for the underlying stock), and in worse case scenario you get back 100% of the capital.

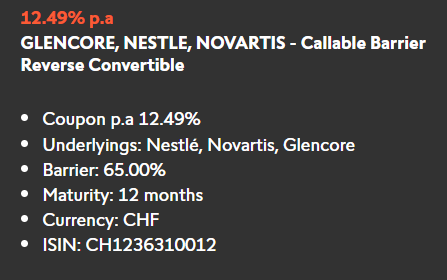

Two big advantages of these barrier reverse convertible are:

downside protection, reimbursed at 100% if all stocks remain above the barrier level during the whole duration

revenue generally not taxed, because the coupon is considered as option premium, not as interest.

The biggest risk is to receive the worst performing stock, in case one falls below the barrier.

The basket of stocks often contains at least one volatile stock. That helps to increase the coupon, but also increases the risk of stock delivery instead of reimbursement. In this example it is Glencore, the coupon % would be quite different it was replaced by Roche…

Note also that there is a secondary market after the product has been emitted. There, it is possible to buy products with shorter remaining time, and some are below their nominal value (if stocks have already gone down since emission). This allows to fine-tune the risk-reward ratio.

All these products should be delta neutral for the issuer, so I would not read too much into it. A barrier reverse convertible is relatively easy to replicate. You can buy a zero coupon bond and sell a down-and-in put option on the security. So if for instance the implied volatility increases, the issuer will be able to offer more attractive products.

I don’t really like these products because the fees can be hidden very well. You need to calculate the value of a replicating product to figure out if you are getting a fair deal (and these products are targeted heavily at retail investors, which usually do not have the necessary background). Furthermore, the value of the products during their lifetime (if you plan to trade them on the secondary market) is not immediately clear because it depends on Delta, Vega, Theta, and Rho of the underlying option.

Ignore it. There are financial products to be bought and to be sold (quoted from white coat investor).

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.